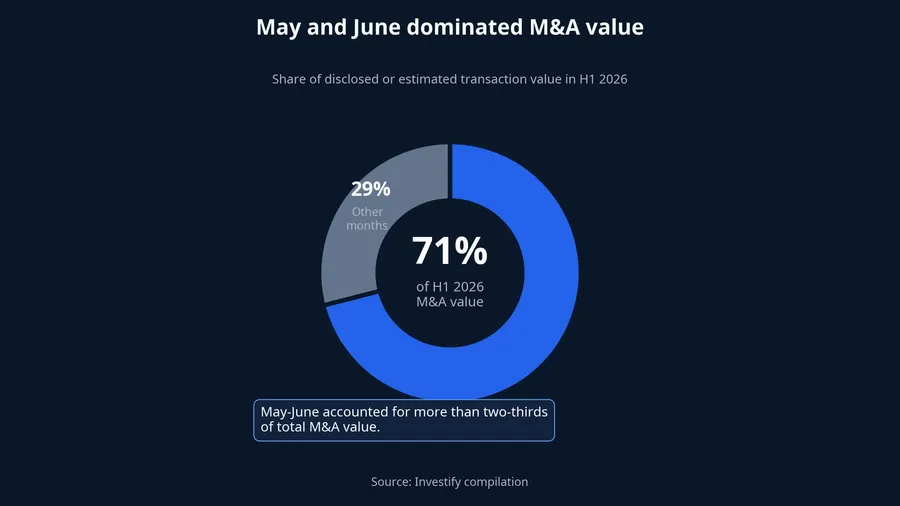

Roughly 71% of disclosed or estimated M&A value in Vietnam's first half of 2026 was concentrated in May and June. That is a clear sign that deal activity accelerated into the end of the period. For a new investor, though, the more useful question is concrete: does the transaction put cash into the company, pay an exiting shareholder, or require a listed company to fund an acquisition? The answer changes how the stock-market implication should be read.Grant Thornton

M&A is not one uniform type of cash flow. Two transactions can appear in the same report while producing opposite balance-sheet effects: one strengthens the target company's resources, while the other creates a large funding requirement for the buyer. The central point here is straightforward. The pickup in M&A deserves attention, but shareholder value can only be assessed after separating the cash structure, control rights and financing behind each deal.

Deal value clustered at the end of the first half

Grant Thornton Vietnam recorded 126 announced transactions in the first six months of the year. Only 89 had a disclosed or estimable value, totaling approximately USD 2.43 billion. The figure therefore describes the observable part of the market, rather than a precise total for every deal completed or announced during the period.Grant Thornton

The useful signal is concentration, not a blanket claim that the entire market is booming. May and June contributed about 71% of first-half value, meaning a handful of large transactions could move the aggregate quickly. Deal count and deal value measure different things: many small deals may add little value, while several large ones can reshape the headline number.Grant Thornton

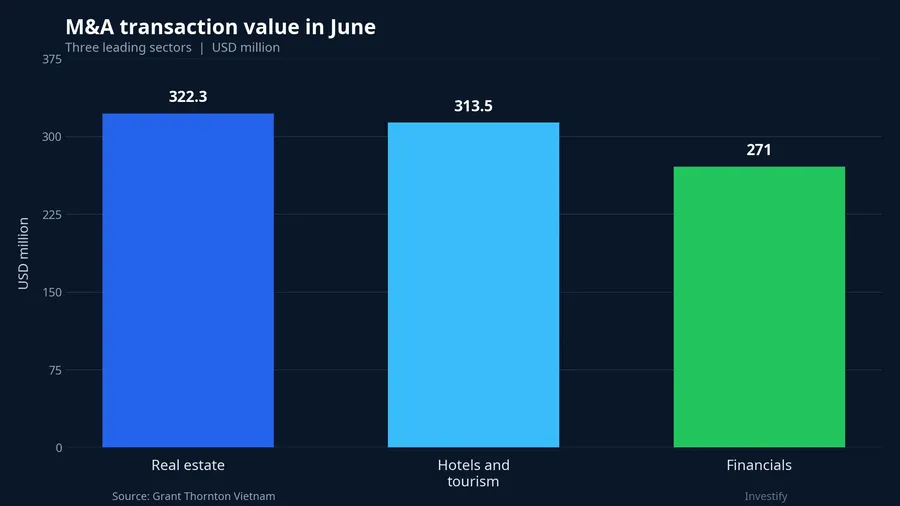

June alone saw 33 announced transactions, with 29 carrying an identifiable value of approximately USD 1 billion. Real estate led at about USD 322.3 million, followed by hotels and tourism at about USD 313.5 million and financials at about USD 271 million. This composition points to concentration in a few sectors, not yet to a broad-based expansion across Vietnamese businesses.Grant Thornton

The same M&A headline can send cash in different directions

Vinpearl is an example of new capital entering the company. It raised USD 255 million through convertible dividend-preference shares; Grant Thornton says the funds are intended to reinforce financial capacity and support the development of its tourism and resort ecosystem. For VPL shareholders, USD 255 million is only the first layer of the analysis. Conversion terms, new investors' rights and the potential future share count matter just as much.Grant Thornton

Phat Dat presents the reverse structure. PDR approved a plan to acquire 35% of Lotte Properties HCMC for approximately VND 7,666 billion, and expects to contribute about VND 2,727 billion more to retain its stake in subsequent capital increases. That is not cash automatically flowing into PDR. It is funding PDR needs to arrange, so shareholder impact depends on completion, funding source, cost of capital and the cash flow generated by the acquired asset.Grant Thornton

It would therefore be premature to place the two companies side by side and decide which is “better off” from their appearance in the report. Vinpearl receives fresh capital but may alter the economic rights of existing holders. PDR may gain an interest in a project, but it also needs to show that both the purchase price and financing are sensible. They are both M&A stories, yet they pose different shareholder questions.

There is also a useful counterfactual to keep in view. A capital raise can be constructive when the new funds earn more than the economic cost of the securities issued, but the same structure can weigh on existing holders if conversion terms are too generous. An acquisition can broaden a company's asset base, yet it can also impair returns if the buyer overpays or relies on expensive borrowing. The M&A label does not resolve these possibilities; the transaction documents and subsequent disclosures do.

An ownership percentage does not settle the control question

VietinBank Capital's acquisition of 9.35 million PET shares, estimated at around VND 495.55 billion, offers another useful distinction. Its holding rose to 13.45% after the transaction. That is a significant shareholder position, but the percentage alone does not establish control of Petrosetco's operations.Grant Thornton

Think of it as owning an apartment in a building. You own part of the property, but you do not automatically make every management decision. In a company, nomination rights, veto rights, shareholder agreements and voting structure show the actual degree of influence. Without that information, interpreting a minority investment as a change of control would go beyond the available evidence.

Viwaseen demonstrates how buyers and sellers can face opposite outcomes in the same transfer sequence. BNE and Xuan Cau Holdings respectively held 24.47% and 14.79% of VIW after the transaction, while Vinaconex reduced its holding from 86.01% to 25%. Buyers gain assets and the seller may receive cash while relinquishing control. VCG shareholders still need information on cost basis, proceeds, disposal gain and subsequent accounting before they can judge the financial result.Grant Thornton

A practical reading framework before looking at the share price

The first question in an M&A announcement is who receives the cash. Issuing new shares typically puts funds into the company, although existing holders may be diluted. When an existing shareholder sells a stake, the seller receives the proceeds and the target company may receive nothing. A listed buyer can add assets, but it may also use cash or take on more debt.

Next, distinguish the transaction stage. An approved plan, a signed agreement and a completed transaction are not interchangeable. PDR's plan indicates intended scale and funding direction; financial effects can only be assessed when conditions have been met, the deal is completed and the investment is recognized. Treating a plan as already-earned profit gets the timing wrong.

Finally, test the consideration and its funding. Cash on hand, borrowing, share issuance and convertible instruments create different trade-offs. A promising asset can still become an expensive deal when funding costs are high. Conversely, a large disposal may not improve long-term value if a company sells an important earnings source without a credible replacement.

That discipline is especially helpful when market attention shifts quickly from a transaction headline to a price move. A share-price reaction can reflect expectations, broader market conditions or investors' different views of the same deal. The public data in this report does not establish which of those forces dominates for any individual ticker. Keeping the deal mechanics separate from the market reaction prevents an appealing narrative from becoming an unsupported causal claim.

The late-first-half acceleration shows that larger M&A transactions are emerging for investors to monitor. It is not a blanket buy signal for every stock mentioned in the data. The next disclosures on completion conditions, financing, governance rights and accounting will be more revealing. That chain of evidence, rather than the market's USD 2.43 billion headline, will show whether a transaction adds operating value, produces a one-off gain or simply moves assets from one owner to another.