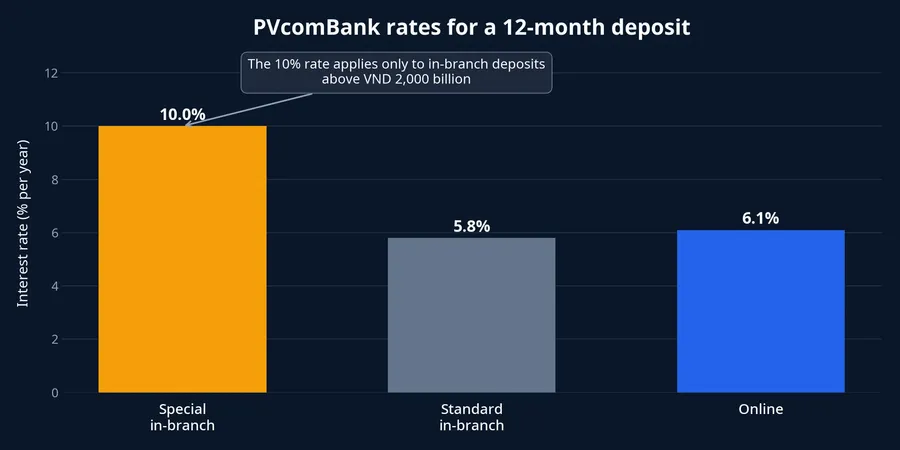

A 10% annual rate is enough to make anyone stop at a rate table. At PVcomBank, however, that rate is reserved for in-branch deposits with a 12- or 13-month term and a balance above VND 2,000 billion. For almost every individual saver, it is not a rate that can be used to calculate the return on their own deposit.Timo

Put simply, a rate table is a price list with conditions. Its biggest number may be compelling, but it matters only if the customer fits the stated segment and deposit method. The useful question is not which bank displays the highest number. It is how much money will actually arrive in your account at maturity, given your balance and your plans for the cash.

The VND 2,000 billion condition behind 10%

A rate roundup updated on July 17 listed PVcomBank at 5.8% per year in branch and 6.1% online for a 12-month term, while the 10.0% special rate carried the very large-balance condition above.Timo

The 3.9-percentage-point gap between 10.0% and 6.1% is not a reward for finding a savings trick. It describes products with very different balance requirements and transaction channels. Including 10.0% in a comparison for a VND 100 million or VND 500 million deposit therefore distorts the exercise before it begins.

The online rate in this example is 0.3 percentage points above the in-branch rate. That gap is far smaller than the special-versus-standard difference, but it is a gap an ordinary saver may actually access by choosing the appropriate channel. This is why the detail lines matter more than the headline.

Put four variables on the same line

To compare two deposits fairly, start with the amount you can genuinely set aside. Then hold the term constant, for example at 12 months, before comparing rates. A longer term should not be put beside a shorter one and used to declare one bank “better”, because the customer is also exchanging access to cash for a different rate.

The third variable is the channel: in branch or online. The July 17 rate roundup shows that PVcomBank can carry different rates across the two channels even for the same 12-month term.Timo The fourth is how interest is paid. Monthly payments put cash in the saver’s hands earlier than an end-of-term payment, so the rate needs to be read alongside the payment method selected.

That difference is not an error in the rate table. Monthly payments give the depositor access to cash earlier, so the bank offers a lower rate than for an end-of-term payment. If one rate is paid at maturity and another monthly, they represent different cash-flow choices, not simply a contest between percentages.

The same logic applies to promotional labels and balance tiers. A rate can be valid, clearly published and still be irrelevant to a particular depositor. That is why a comparison should record the rule beside the number, not in a separate mental footnote. It is much easier to notice that an offer requires an extraordinary balance, or a different payment method, before funds are locked into a term than after the deposit has been opened.

For a first-time saver, a short note can prevent confusion: deposit amount, term, opening channel, interest-payment method and minimum conditions. Only when these five fields match can two rates be placed side by side. It is a modest discipline, but it removes headline figures that you are not eligible to receive.

How to calculate interest actually received

For an end-of-term deposit held for a full year, the illustration is straightforward: principal multiplied by the annual rate. Circular 14/2017/TT-NHNN states rates as a percentage per year and uses 365 days as the standard year; actual interest is calculated from the balance, rate and number of days the balance is maintained.Government of Vietnam

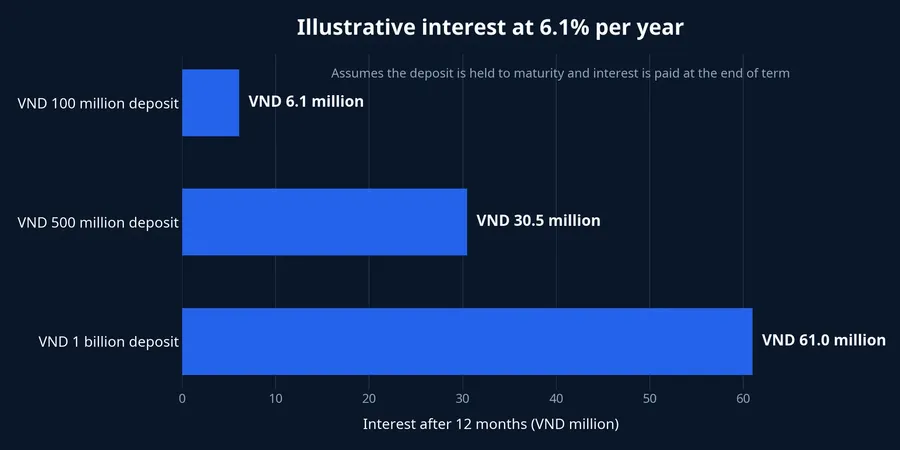

Using PVcomBank’s 6.1% online rate as an illustration, a VND 100 million deposit held for 12 months generates VND 6.1 million of interest, for a total of VND 106.1 million. At the same rate and assumptions, VND 500 million generates VND 30.5 million and VND 1 billion generates VND 61 million.Timo

What matters is not to expect the 10.0% rate on a VND 100 million deposit. That calculation would produce VND 10 million of interest, VND 3.9 million more than the 6.1% illustration. The arithmetic is fine, but its input is wrong because 10.0% belongs to an entirely different balance condition.

The illustration is not a promise for every product. A deposit whose dates do not cover exactly 365 days is calculated using the actual number of days, and a different payment method also changes the result. Checking the projected interest in the app or contract before confirmation remains important.

It also helps to separate a calculation from a decision. The calculation answers what a stated rate would produce under stated assumptions. The decision still depends on whether the money is genuinely available for that term, whether monthly income is needed, and whether the product’s withdrawal rules suit the household’s cash reserve.

Early withdrawal can reverse the result

A term rate delivers its full value only if the deposit reaches maturity. Under Article 5 of Circular 04/2022/TT-NHNN, when a customer withdraws the entire balance early, the credit institution applies no more than the lowest applicable demand-deposit rate for that customer and currency at the time of withdrawal. PVcomBank states the same condition for its Đại Chúng Savings product.Government of Vietnam PVcomBank

This is often overlooked when attention is fixed on a difference of a few tenths of a percentage point. A VND 200 million deposit at 6.1%, if held to maturity, corresponds to VND 12.2 million of interest in this illustration. If the entire balance is withdrawn midway through the term, 6.1% is no longer the basis for calculating the return over the period already elapsed.

The current rules treat partial withdrawal separately. The withdrawn portion receives the applicable demand-deposit rate, while the balance left in place continues to earn the originally agreed rate. Even so, savers should check the contract or ask the bank whether the particular product permits partial withdrawal and what procedure applies.Government of Vietnam

How to read a rate table before depositing

The most useful habit is to cross out special rates if you do not meet their conditions. Then compare each available option using the same amount, term, channel and interest-payment method. Finally, read the early-withdrawal, automatic-renewal and minimum-balance terms. This is not paperwork for its own sake; it turns an advertised percentage into a number you can verify.

In the PVcomBank example, an ordinary saver should compare the 5.8% in-branch rate or 6.1% online rate for a 12-month deposit, rather than use 10.0% as the benchmark.Timo The thesis remains the same: the highest stated rate is useful only when it applies to your own deposit. Before committing money, watch the balance condition, payment method and likelihood that you will need the cash before maturity.