A bond fund can generate a gain for investors who stay while paying out cash to investors who leave. There is no contradiction in that. In the first half of 2026, 20 of the 28 tracked bond funds saw net withdrawals, totalling about VND 7,300 billion.Tin Nhanh Chứng Khoán

That figure is not a verdict that every bond fund has invested badly. It is a practical reminder that a positive return alone may not keep investors in a product when another option better matches their needs. In plain terms, investors are answering two different questions: how much has my fund certificate gained, and do I still want my money here?

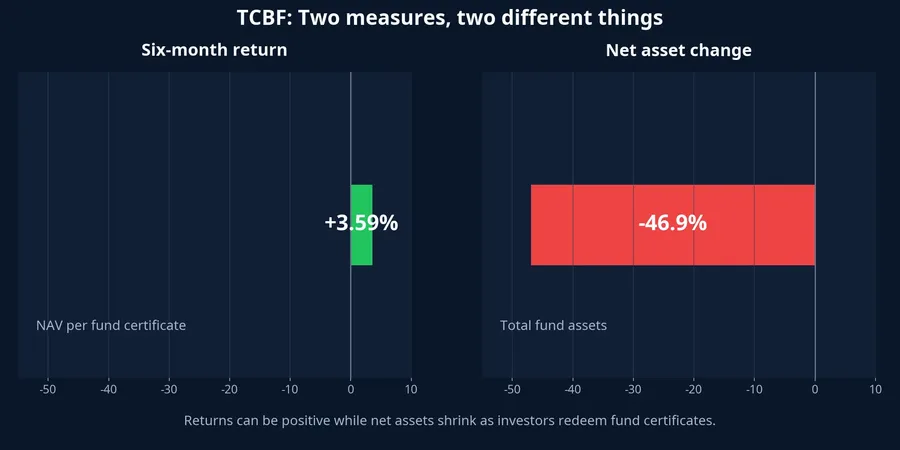

NAV and fund size are not the same measure

NAV is the net asset value per fund certificate. When it rises, an investor who bought at the start of the period has a positive return on that holding, before taxes and charges triggered by a sale. This is the figure that describes the investment performance of each certificate.

The fund's total net assets tell a broader story. They move with the portfolio, but they also change as investors subscribe for or redeem certificates. When many investors sell, the fund pays redemptions and total assets can shrink even while NAV per certificate continues to rise.

TCBF makes the distinction especially clear. In the first-half data, the fund saw more than VND 4,800 billion in withdrawals, nearly 65% of net withdrawals from the bond-fund group, while its return remained positive at 3.59%.Tin Nhanh Chứng Khoán Reading the contraction in size alone as an investment loss would confuse money leaving the fund with the portfolio's return.

TCBF's June report recorded VND 5,230 billion in assets under management, NAV of VND 20,759 per certificate and 251.9 million certificates outstanding.Techcom Capital NAV describes the value of one unit. Certificates outstanding and total assets add the dimension of how much capital remains in the fund. Together, the three figures give a more complete picture.

Withdrawals do not have one explanation

The available figures do not show where each withdrawing investor moved their money. It would therefore be too quick to claim that every redemption was profit-taking, a move to equities or a return to bank deposits. Some investors may need cash. Others may be rebalancing, while some may prefer a more predictable return during a period when they expect to use the money.

What the data supports more clearly is that the product's competitiveness is being tested. Withdrawals were concentrated in large funds, while some smaller funds still received modest inflows. This does not yet look like a wholesale exit from the asset class. It looks more like investors are distinguishing between funds, fee structures and their own liquidity needs. That distinction matters because a fund's headline return is only one input into a household decision. The certainty of a planned expense, the time required to receive redemption cash and the ability to tolerate a lower NAV can matter just as much.

The comparison with deposits also needs to be made on equal terms. A July 15 survey put six-month online deposit rates at the sampled banks between 3.5% and 6.8% per year.VietnamPlus Those are annual quoted rates, whereas TCBF's 3.59% is a six-month return. Placing the two figures side by side without matching the holding period creates a misleading comparison.

The published return is not the cash you receive

Think of a fund return as the NAV result shown on the screen. The cash actually received after selling also depends on purchase date, sale date, tax and fees. TCBF publishes an annual management fee of 1.2% of NAV and a redemption fee that ranges from 1% to 0%, depending on the holding period.Techcom Capital An investor who sells early because cash is needed may realise less than the performance number previously seen.

That is also why a bond fund should not be treated as a savings account with a different label. NAV can fluctuate with markets and investors can lose capital. In its June report, TCBF allocated 85.7% of assets to bonds and 14.4% to cash and short-term liquid assets.Techcom Capital The name “bond fund” does not by itself reveal issuer quality, portfolio concentration or how long the underlying assets take to mature.

Bank deposits have a different protection mechanism. From July 13, 2026, Vietnam's deposit-insurance payout limit is VND 350 million, including principal and interest, for one person at one participating institution.DIV That does not make deposits the better choice in every situation. In exchange, an early withdrawal will generally receive a lower rate under the product's terms.

A practical comparison for new investors

Before choosing a bond fund or a deposit, bring both options back to the same date on which you need the money and the same expected cash amount. Do not begin and end with “what percentage return does it offer?” The checks below make the comparison more useful and less emotional.

| What to check | Question to answer |

|---|---|

| Net return | After management fees, redemption fees and tax, how much cash remains? Has the deposit rate been converted to the same holding period? |

| Fluctuation | If the money is needed on a fixed date, could NAV be below the purchase level? |

| Access to cash | On which days does the fund trade, and when does cash reach the account? What happens to deposit interest after an early withdrawal? |

| Asset quality | Whose bonds does the fund own? Is it concentrated in a few issuers, and does the maturity profile fit the goal? |

| Protection | Is the deposit within the insurance limit? Which fluctuations does the fund-certificate holder bear directly? |

The conclusion is not that bond funds are always better, or that deposits are always safer. A positive return is necessary, but it is not sufficient to make a fund compelling. For money needed on a fixed date, where certainty within the insured limit matters most, deposits have a structural advantage. Bond funds still have a place for investors who can accept NAV movements, understand the portfolio and do not need immediate access to the money. Neither choice should be reduced to a league table of quoted rates. The right comparison is the return that remains after costs, the uncertainty accepted and the timing of the financial goal.

The signals worth watching are therefore not limited to whether next month's NAV rises or falls. Watch net flows, the fees that apply to your intended holding period, portfolio quality and the return gap after both choices are converted to the same time horizon. Only when those four pieces fit together does a published return become meaningful for your own money.