An infrastructure project or power plant can take a decade to build, stabilize operations and generate cash for debt service. Yet much of a bank's funding comes from short-term deposits that mature, and can be withdrawn, far sooner. That is why financing major projects is not simply a question of whether banks can lend more. It is a question of whether the money stays available for as long as the project needs it.

At the July 18 Standing Government Conference with the business community, Nguyễn Thanh Tùng, Chairman of the Board of Directors of Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank), said banks would not have abundant funding to meet credit demand from many upcoming large projects. Phạm Đức Ấn, Governor of the State Bank of Vietnam, also pointed to the system's substantial maturity mismatch.Báo Chính phủ

This is not an argument for diminishing banks' role. It helps new investors read the relationship between credit, interest rates and the bond market more accurately. When the term of funding does not match the term of a loan, the strain usually first appears in funding costs before it reaches companies seeking capital.

The real constraint is the time horizon of capital

Think of a bank as taking deposits from many people with different maturity dates, then using the aggregate balance sheet to fund longer-lived assets. It does not move one savings account directly into one project. Its balance sheet also includes equity, liquid assets, borrowed funding and many other loans. Still, time remains the core constraint.

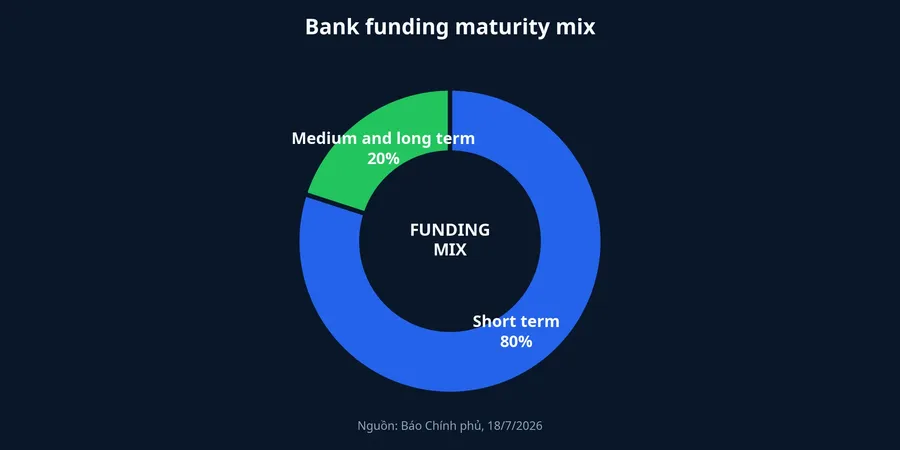

In his conference remarks, Governor Phạm Đức Ấn said short-term funding accounts for 80% of the total, while medium- and long-term funding represents just 20%.Báo Chính phủ Short-term money suits revolving needs such as inventory purchases, payroll and a production cycle. A highway, industrial park or power plant, by contrast, may not generate cash until well after construction and commissioning.

When a bank uses too much short-term funding for long-term loans, it must keep replacing that funding while the loan has not yet returned cash. The risk need not show up on the day a loan is disbursed. It becomes clearer when deposit rates rise, customers shift between tenors or capital markets tighten while a half-built project still needs funding.

That is why liquidity limits and rules governing the use of short-term funds for medium- and long-term lending are more than technical details. They help a bank meet current obligations while longer-lived assets have not begun to pay back. Remaining room for credit growth therefore does not mean that cheap, suitably long-term funding is unlimited.

A low LDR does not settle the funding question

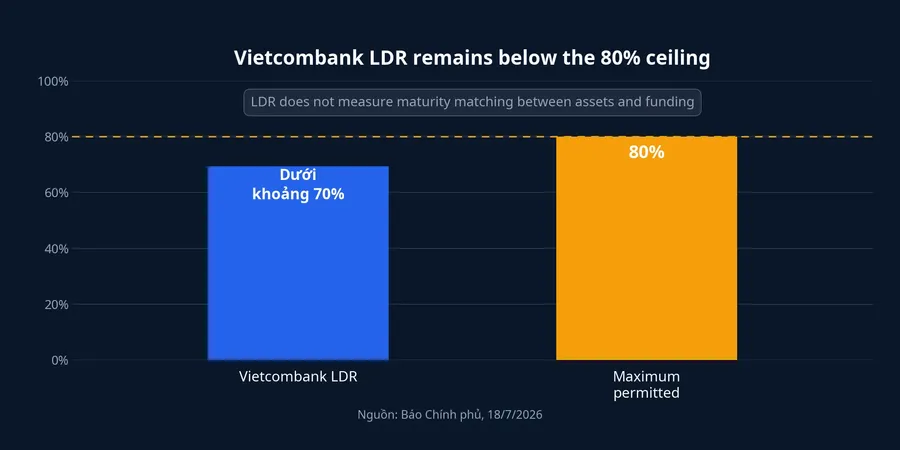

The loan-to-deposit ratio, or LDR, compares outstanding loans with mobilized funding. It is useful for judging the scale of lending against deposits, but it does not directly measure whether asset and funding maturities match. That distinction matters when an investor sees a ratio below its limit and assumes the bank has spare money for every long-term loan.

Nguyễn Thanh Tùng said Vietcombank is permitted to maintain an LDR of 80%, while its own ratio is below approximately 70%.Báo Chính phủ That buffer indicates room when measured against total deposits and loans. It does not reveal the tenors of those deposits, nor does it turn short-term savings into ten-year funding.

Extending the tenor of deposits or adding outside funding normally costs more. Governor Phạm Đức Ấn described the transmission plainly: funding scarcity raises deposit rates, and higher input costs then feed into lending rates.Báo Chính phủ For companies, that can mean higher borrowing costs or tighter control over disbursement. For depositors, it does not automatically mean a risk of losing money, because banks also have equity, liquid assets and other prudential requirements.

Bonds match maturities, but they do not erase risk

Bonds serve a different function from bank loans. They can connect a company that needs capital for years with an investor willing to hold for a matching term. The company knows its interest and principal schedule; the investor can examine the maturity, coupon, terms and priority of claims. When it works well, this market keeps part of long-term financing from being concentrated on bank balance sheets.

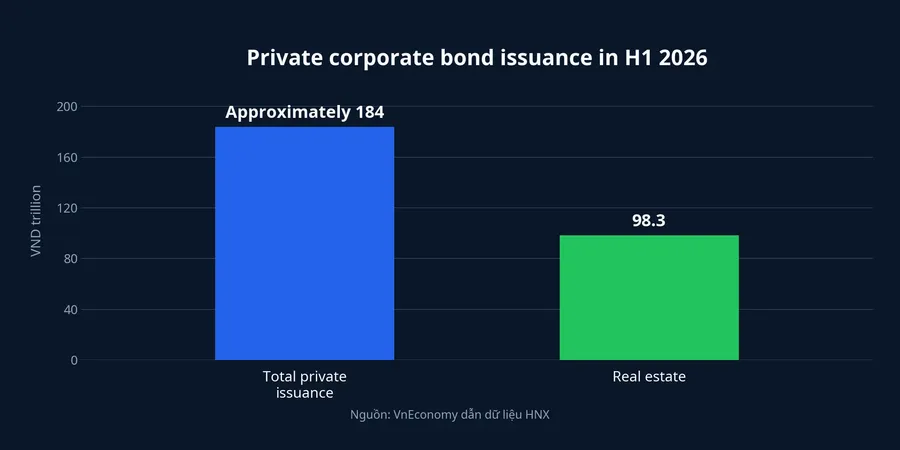

HNX data cited by VnEconomy show that private corporate bond issuance in the first half of 2026 totaled approximately VND 184,000 billion. Real-estate issuers accounted for VND 98,300 billion, or roughly 53.4% of issuance.VnEconomy The scale shows that bonds are already a meaningful funding channel. The composition is also a reminder that total issuance alone cannot prove that the market is diversified or safe.

A bond does not create repayment cash flow in place of the company. It changes who provides capital and how credit risk is allocated. When a bank lends, it underwrites and retains that risk on its balance sheet. When a company issues bonds, part of that risk passes directly to bondholders. A higher yield is usually compensation for weaker repayment capacity, harder-to-realize collateral or a longer tenor. It is not a free reward.

Investors need to look beyond the collateral label

Put simply, the phrase “secured by collateral” answers only a small part of the question. A buyer needs to know who owns the asset, how it was valued, whether it secures other obligations, who holds the records and who has the right to enforce the security if the company misses payments. The value written in a file can be very different from the cash recovered in a forced sale.

At the conference, Governor Phạm Đức Ấn said that a provision allowing commercial banks to choose to provide asset-management services for bond issuance had been reported to the Government and is expected to be included in a bill amending the Law on Credit Institutions.Báo Chính phủ This is not an issued or effective rule. If enacted, the mechanism could clarify custody and management responsibilities, but it cannot replace the key task of assessing the cash flow a company will use to repay interest and principal.

Private placements should not be treated as identical to public bond offerings. Issuance conditions, eligible buyers and disclosure standards differ. In particular, Vietnamese private corporate bonds are for professional securities investors; an attractive coupon does not remove the need to understand the issuance documents and the underlying credit risk.

Conclusion: capital must be shared with the right risk holders

The central point is unchanged. Banks remain essential, especially for working capital and the early stages of a project. But a multi-year project is more durable when it is supported by funding with a matching tenor, including equity and bonds, rather than relying too heavily on rolling over short-term deposits.

For the bond market to share that funding burden safely, financial information must be reliable, use of proceeds must be transparent, collateral management responsibilities must be clear and buyers must be able to assess risk. The next signals worth watching are the progress of the legislative amendment, the quality of disclosure in each issuance and each issuer's actual capacity to service debt. Those are the tests of a healthier long-term capital market, not merely the total value of bonds issued.