A week full of bad headlines would normally lead investors to expect oil and gold to rise together. The final session of July 17 showed why that shortcut can fail. Brent was volatile as risks to energy shipments around Hormuz and the Red Sea came into focus. Gold, meanwhile, weakened as higher energy prices revived inflation concerns and the prospect of US interest rates staying high.VOV

The central point is straightforward: one shock can send oil and gold in opposite directions because each market is processing a different problem. Oil first prices the risk that physical barrels will not reach buyers. Gold must weigh safe-haven demand against the opportunity cost of holding an asset with no yield. When the rates channel dominates, geopolitical stress does not automatically lift gold.

Oil is pricing delivery risk

On July 17, Brent rose by nearly USD 1 during the session before easing slightly. The market remained focused on risks to oil flows through Hormuz and the prospect of stress extending to the Red Sea.VOV That is the key distinction between oil and many financial assets: crude must be carried, delivered and refined on time.

Hormuz and Bab el-Mandeb are different choke points in the energy shipping chain. Trouble at one can make the workaround through the other less reliable. Insurance costs, tanker schedules, rerouting time and inventories at delivery points are the indicators that distinguish anxiety-driven pricing from a prolonged physical squeeze.

Military headlines and oil prices also do not move in lockstep during every session. The market can assess supply risk and take profits after volatile sessions at the same time. A quieter session does not invalidate the shipping story.

The Red Sea raises the cost of the detour

When Hormuz is disrupted, Red Sea ports and alternative routes become a buffer for supply chains. That buffer only works while it remains open. A July 17 VOV report described the risk that Houthi forces could be ready to block Red Sea export routes if the conflict escalates.VOV

For a new investor, the simple version is this: oil prices do not only reflect how many barrels sit underground. They also reflect how many barrels can pass through the right gateway at the right time. When a gateway is impaired, the cost of keeping that flow moving rises even if production at the field has not changed.

Still, the potential for a Red Sea disruption should not be treated as a completed event. VOV described it as a risk traders were weighing; Brent eased slightly on July 17 after rising earlier in the session.VOV The disciplined reading is to watch actual vessel traffic and freight costs, rather than turn a threat into a certain long-term shortage.

Gold reacts to the price of money

Gold does not generate periodic cash flow. When Treasury yields or USD deposit rates become more attractive, holding gold carries a higher opportunity cost. That channel dominated this week. Global gold prices fell 2% on July 16 as oil and US Treasury yields rose, fuelling concern that inflation would remain high enough to keep interest rates elevated for longer.CafeF

In plain terms, expensive oil can travel through several links. It raises energy costs, which can make inflation harder to cool. If that reinforces expectations for higher US rates, bonds and USD deposits become relatively more attractive. Gold then has to compete with yield, rather than simply benefit from demand for protection.

CME FedWatch showed traders assigning roughly a 53% probability to a Fed rate increase at the September meeting at that time. That was a market expectation, not a Fed commitment.CafeF It shows why the label “safe haven” is insufficient for forecasting: a shock can increase the demand for protection while also raising real yields and the cost of owning gold.

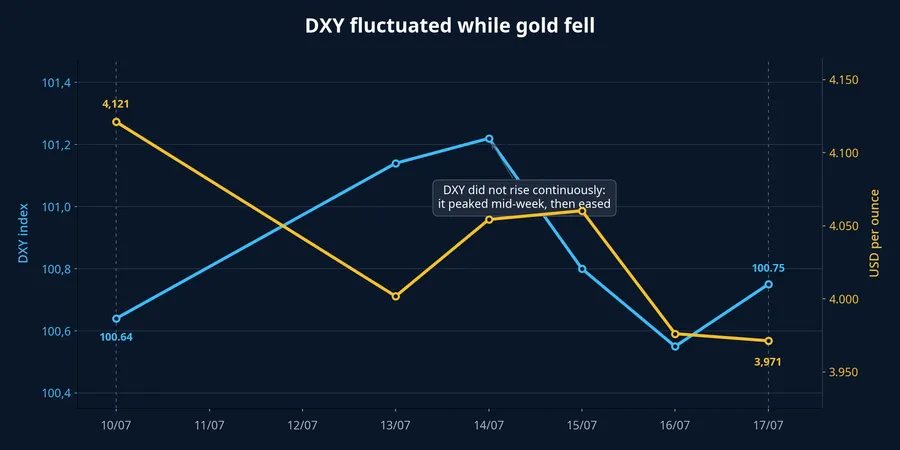

The US dollar is worth tracking, but it should not become the single explanation. The US Dollar Index was around 100.76 on July 17, while the dollar had fallen nearly 0.25% from the start of the week after June inflation data cooled.CafeF Because the dollar did not rise consistently through the week, the evidence leans more toward a yields-and-rate-expectations explanation than a mechanical “strong dollar, weak gold” rule.

There are plausible offsetting explanations. Softer US inflation data and profit-taking after a sharp down day can support gold. This is not a claim that rising oil always pushes gold lower. It describes this particular week, when the inflation-and-rates channel outweighed the safe-haven channel. If concern about the financial system rose quickly or yields turned decisively lower, oil and gold could still advance together.

Vietnam adds another layer to gold prices

Vietnamese investors also need to separate international gold from domestic bullion. On July 17, SJC gold bar selling prices fell VND 1.6 million per tael to VND 146.6 million, while the bid-ask spread for gold bars ranged from VND 3 million to VND 4.2 million per tael.CafeF That spread means being right about the global direction may still not offset trading costs over a short period.

So a Vietnamese gold investor should separate at least three layers: international bullion prices, US yields and the USD exchange rate, and the actual bid and offer prices at home. Ignoring the third layer can turn a correct global view into an incorrect assumption about domestic returns, because the quoted spread can determine much of the short-term outcome.

Conclusion: Follow the transmission path, not the label

This week's thesis is that oil was led primarily by delivery risk, while gold was pressured primarily by the outlook for inflation and interest rates. Those conclusions are not contradictory; they are two transmission paths from the same shock. The thesis would change if vessel traffic and freight costs normalised quickly, or if US yields fell materially as Fed expectations shifted.

For oil, watch flows through Hormuz and Bab el-Mandeb, delivery delays and freight costs. For gold, US Treasury yields, rate expectations and the direction of the dollar matter more than any single geopolitical headline. The broader lesson is that the same shock does not produce the same response across every asset class.