Nearly VND 18.9 trillion in consolidated pre-tax profit is a number designed to command attention. VPBank reported 68% year-on-year growth for the first half of 2026 and completion of nearly 46% of its annual profit plan; the second quarter alone produced almost VND 11 trillion. Yet for a financial group, the consolidated number cannot be read as though it belonged to a single legal entity.VPBank

The central takeaway is straightforward. The parent bank remains the principal income engine, while VPBankS, OPES and GPBank broaden the group’s sources of profit. That does not, by itself, prove that profit quality has improved at the same pace. The detailed second-quarter accounts still need to show the net interest margin, provisioning expense, income mix and movement in loan-quality buckets.

Start with the right reporting perimeter

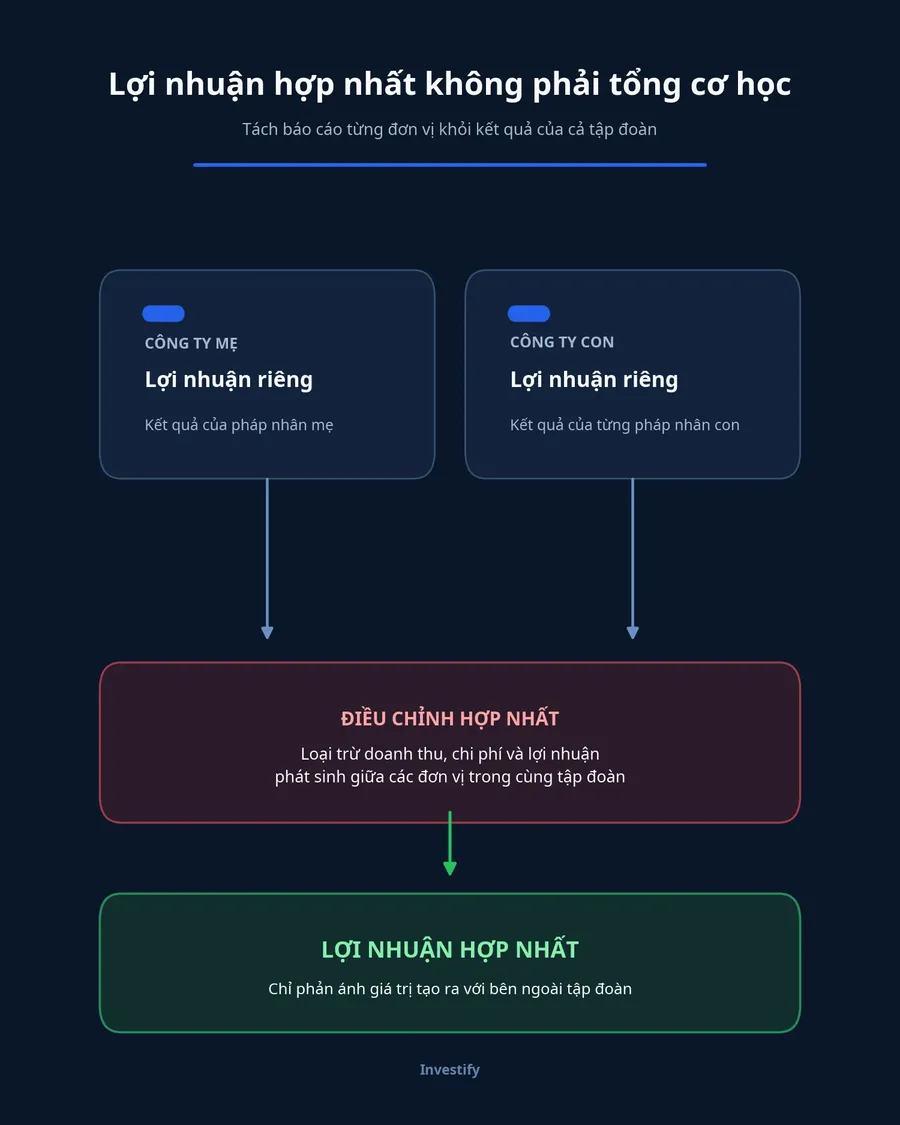

Consolidated profit is the group result after intra-group transactions and other consolidation adjustments. It is therefore different from the standalone profit of the parent bank or a figure released by an individual subsidiary. This distinction is the first safeguard for new investors confronted with several profit figures in the same release.

VPBank described consolidated pre-tax profit as nearly VND 18.9 trillion. It separately said the parent bank had earned VND 15.6 trillion in “profit” after two quarters, without specifying in that passage whether the measure was pre- or post-tax. Numbers placed close together are not automatically comparable or additive. The prudent approach is to retain the source’s label and wait for the detailed statements to clarify the accounting basis.VPBank

Put simply, consolidated accounts treat the ecosystem as one economic entity. Revenue at one group company may be an expense at another. Keeping both when adding the pieces would double-count value. Ownership stakes, non-controlling interests and other consolidation adjustments can also make the total differ from a simple sum.

This is more than a technical accounting point. A reader who treats every subsidiary disclosure as an extra block of group profit may overstate what the group actually earned. Conversely, a lower consolidated result does not tell us that a subsidiary performed poorly. It may simply reflect eliminations or a reporting basis that is not identical to the group headline. The notes to the accounts are where these differences become traceable rather than assumed.

The parent bank still sets the income pace

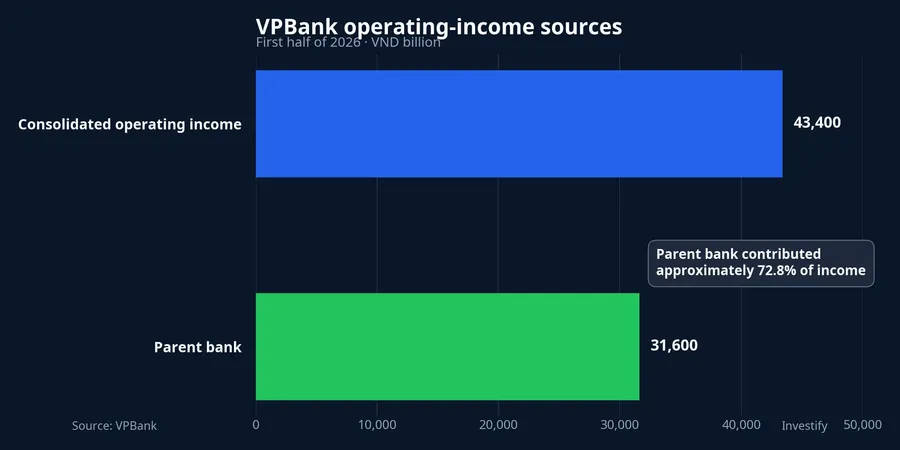

VPBank’s consolidated operating income reached VND 43,400 billion in the first half, up 35.2% year on year. The parent bank accounted for more than VND 31,600 billion, also up 35%. Dividing the two disclosed figures gives the parent bank an estimated 72.8% share of consolidated operating income.VPBank

That share identifies where the closest reading should begin. Interest income, funding costs, lending growth, provisioning and credit quality at the parent bank will carry the greatest weight for the group. Subsidiaries can diversify the income base, but they have not displaced the core role of banking.

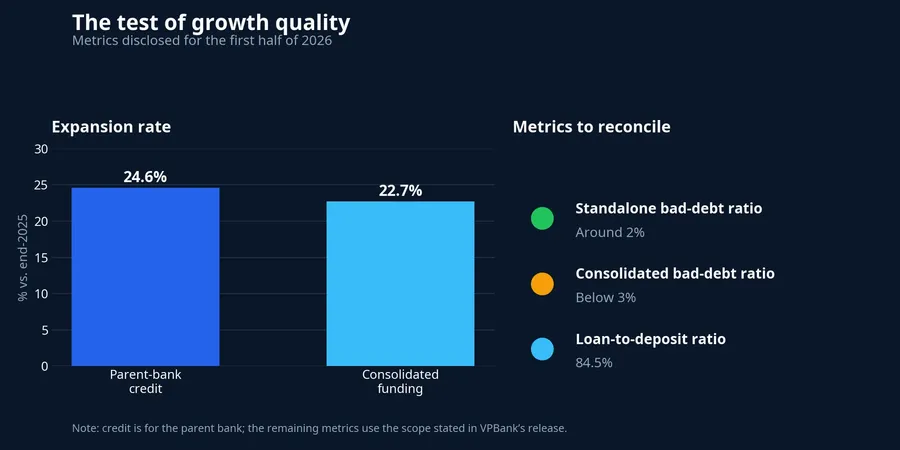

Balance-sheet growth accompanies that expansion. Consolidated assets exceeded VND 1.5 quadrillion, up 19.2% from end-2025. Parent-bank credit was nearly VND 1.06 quadrillion, up 24.6%, while consolidated customer deposits and valuable papers were nearly VND 902,000 billion, up 22.7%.VPBank

Those growth rates merit attention, but they do not establish a liquidity conclusion because the scopes are not identical: credit is a parent-bank figure, while funding is consolidated. VPBank reported a loan-to-deposit ratio of 84.5% that remained compliant with regulations. A fuller assessment requires a detailed balance sheet, maturity structure and funding costs on a comparable perimeter.VPBank

The distinction matters because a faster credit-growth number is not a diagnosis on its own. It can reflect lending demand, a change in the mix of funding, or a different reporting boundary. A sound reading compares like with like before drawing conclusions about funding pressure. The 84.5% ratio is therefore a useful disclosed reference point, while the maturity and cost detail remains the necessary follow-through.

Non-bank businesses now carry more weight

The subsidiaries’ progress is a constructive signal, provided it is read carefully. VPBankS recorded VND 2,673 billion in pre-tax profit for the first half, three times the prior-year level. VPBank also said the securities firm entered the top eight by brokerage market share on HOSE. The result makes the brokerage business a material earnings source worth following in its own right.VPBank

OPES earned VND 613 billion in profit, nearly three times the year-earlier result; VPBank linked the increase to growth in original insurance premiums. GPBank generated more than VND 730 billion in profit in six months, nearly 1.5 times its full-year 2025 result. These disclosures show a broader set of earnings sources, but they do not directly reveal each entity’s net contribution to consolidated profit.VPBank

FE Credit had no separately disclosed profit figure in the July 17 release. Without that figure, consumer finance cannot be assigned a share of the consolidated profit increase simply because it belongs to the ecosystem. Investors should not fill in an omitted disclosure with an assumption.VPBank

Why simple addition fails

Adding the published numbers for the parent bank, VPBankS, OPES and GPBank already produces more than the nearly VND 18.9 trillion consolidated profit. That is not evidence of an error. It is a reminder that the figures may differ in pre- versus post-tax basis, reporting scope and consolidation treatment.VPBank

For investors, standalone subsidiary figures are directional. VPBankS shows a growing securities contribution; OPES and GPBank show expansion into other lines of business. Only the financial-statement notes can quantify intercompany eliminations, non-controlling interests and each piece’s net contribution to profit attributable to the bank’s shareholders.

That distinction also shapes how to read diversification. More profit engines can reduce reliance on a single business line, but they do not automatically make earnings more predictable. Each business has its own income drivers and reporting base. The evidence currently supports the narrower claim that VPBank’s earnings base has broadened; it does not yet support a precise ranking of which subsidiary created the incremental consolidated profit.

The next test is still ahead

VPBank reported a consolidated Basel II capital adequacy ratio of 13%, a standalone bad-debt ratio of around 2% under Circular 31 and below its 2.5% target, and a consolidated bad-debt ratio below 3%. Its ratio of short-term funds used for medium- and long-term lending was 22.4%. These are useful initial buffers, but each is a point-in-time snapshot.VPBank

The detailed accounts should show whether NIM held up, how provisioning changed as lending accelerated, and whether special-mention loans moved. The non-interest-income mix also needs separating so recurring income is not confused with one-off items. These questions do not negate the reported result; they determine how durable it is.

For a first read of the next filing, the order of operations is practical. Start with the parent bank’s income and funding trends because they account for most operating income. Then check how much of the group’s result came from recurring interest and fee income, rather than a temporary item. Finally, compare the provisioning charge and the loan-quality disclosures with the pace of credit growth. This sequence does not produce a buy-or-sell conclusion; it makes the reported 68% growth easier to place in context.

The appropriate conclusion for now is that VPBank has expanded its scale and built additional profit legs beyond the parent bank. Evidence is not yet sufficient to say profit quality has improved in lockstep. The second-quarter accounts and accompanying notes are the next checkpoint, especially for NIM, provisioning, income mix and bad debt.