Since July 13, 2026, Vietnam's standard deposit-insurance payout limit has been VND 350 million for a depositor at a participating institution. The limit covers all insured deposits, including both principal and accrued interest.DIV That matters for new savers who split money into several accounts to manage different maturities. Splitting accounts can improve cash-flow planning, but it does not create extra insurance limits.

The simplest way to think about the rule is that it does not count passbooks or app accounts. It looks at the depositor and the institution that takes the deposit. If the accounts are in your name at the same bank, their insured balances are aggregated when your insurance entitlement is calculated. That distinction prevents a common misunderstanding: opening another savings account in the same bank's app does not add another layer of protection.

The calculation is per depositor, per institution

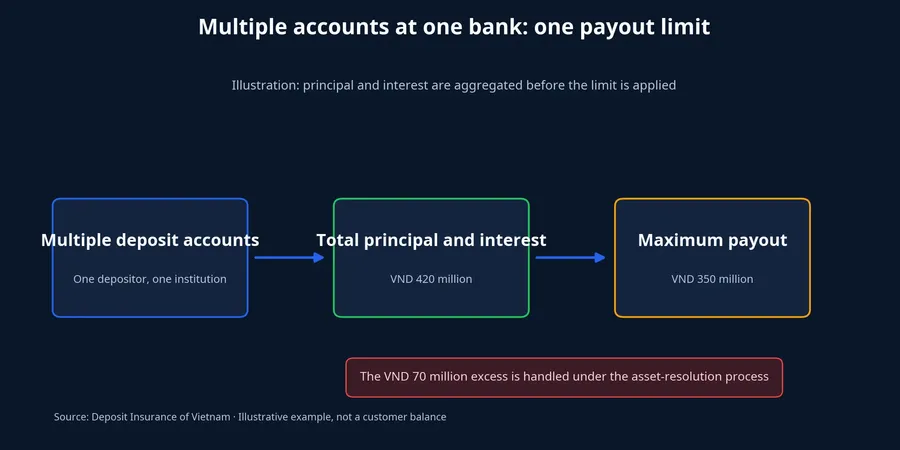

Suppose the total of your principal and interest at one bank is VND 420 million. It makes no difference whether that money sits in one 12-month account, two short-term accounts, or a demand deposit. The calculation begins with the VND 420 million total, and the standard insurance payout is capped at VND 350 million.DIV

The VND 70 million excess in that example is not automatically lost. Under the Deposit Insurance Law, principal and interest above the payout limit are addressed through the process for resolving the participating institution's assets.Chính phủ These are different mechanisms: deposit insurance is the amount paid within the limit once the payout obligation arises, while the excess depends on the legal asset-resolution process.

Digital banking can make the distinction harder to see. You may have opened one account at a branch, renewed another in the app, and bought a certificate of deposit under the same bank's brand. If the same legal entity issued those products, they are still treated as one institution for the insurance calculation. Check the legal name on the contract or certificate, not simply the product label or where the account was opened.

That habit is useful even when no insurance event is in view. Product names can be similar while their issuer, currency, ownership status, or withdrawal terms differ. A few minutes spent matching the app screen to the contract can make the later review of insured balances much more reliable.

Deposits at different participating institutions, by contrast, are assessed separately. VND 300 million at institution A and VND 300 million at institution B are not combined merely because they belong to the same person. That does not mean everyone should divide savings using a fixed formula. Interest rates, maturity, early-withdrawal needs, service quality, and the fit with personal goals all remain relevant.

Interest is part of the same total

Another common mistake is to compare only the principal with the VND 350 million figure. The current limit applies to the full insured deposit balance, including principal and interest.DIV Interest is therefore not protected separately outside the limit.

For example, VND 340 million of principal plus VND 15 million of interest calculated when the payout obligation arises produces a VND 355 million amount for comparison with the limit. In that illustration, the standard insured payout remains no more than VND 350 million. When reviewing your position, include accrued interest rather than recording only each account's original face value.

There is one more subtraction to consider if you also owe money to the same deposit-taking institution. The law provides that the insured deposit amount is the amount remaining after debts, including outstanding principal and interest, are deducted at that institution.Chính phủ In practical terms, a personal review should include a column for relevant loans or other debt, not only deposit balances.

Not every product in a banking app is a deposit

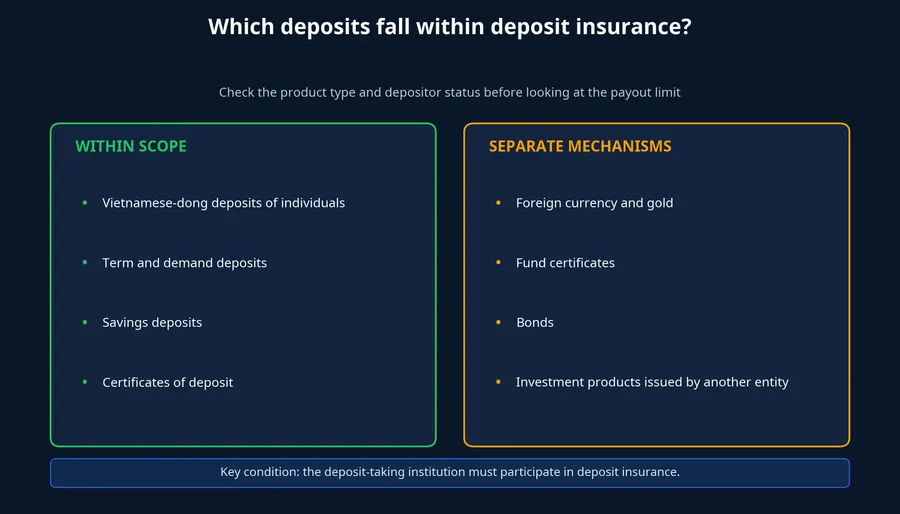

Deposit insurance focuses on Vietnamese-dong deposits of individuals held at participating institutions. The 2025 Deposit Insurance Law took effect on May 1, 2026, and Circular 05/2026/TT-NHNN, which sets the VND 350 million limit, took effect on July 13, 2026.Chính phủDIV Savers therefore need to check both the product type and the institution behind it.

Term deposits, demand deposits, savings deposits, and Vietnamese-dong certificates of deposit held by individuals are product categories to assess against the insurance conditions. Foreign-currency deposits and gold are outside deposit-insurance coverage.DIV Fund certificates, bonds, and investment products distributed through a banking app should not simply be called deposits either: their risks and investor rights follow separate arrangements.

A practical check is to confirm whether the deposit-taking institution participates in deposit insurance and then read the contract closely. Information about the certificate of participation must be publicly displayed under the rules. If a product's name is unclear, or the money is transferred to a different legal entity, ask the provider for a written explanation of the product and the applicable protection.

A joint account is not a separate insurance bucket

For jointly owned deposits, the insurance entitlement is allocated under the co-owners' agreement. Where there is no agreement or no possible agreement, the allocation is handled under the law. Each owner's share is then added to that person's other insured deposits at the same institution before it is compared with the payout limit.Chính phủ

Imagine that your share in a joint deposit is VND 100 million and you also have VND 300 million, including principal and interest, in an individual deposit at the same institution. The total used for the limit is VND 400 million. The joint account does not automatically become an independent insurance bucket, so ownership shares and co-owner agreements should be documented clearly before any problem arises.

A small worksheet can prevent a large misunderstanding

If you hold several savings products, group them by the legal name of each deposit-taking institution. Keep one line for each institution and record:

- The total principal across all accounts in your name.

- Interest that has accrued.

- Your share of jointly owned deposits.

- Outstanding principal and interest you owe to that institution.

- The currency and product type.

- Whether the institution participates in deposit insurance.

This list is not meant to turn saving into an unnecessarily complicated exercise. It simply separates two questions that are often mixed together. The first is which balances, and how much of them, fall within the insurance payout limit; the second is which institution and maturity suit your own financial goals.

The key takeaway is not the number of accounts. Splitting deposits can still be useful for staggering maturities, keeping cash available, or separating spending goals. But where all balances belong to one person at one institution, the insurance limit still applies to the aggregate insured principal and interest. The useful things to monitor are the legal entity taking the deposit, the nature of the product, and your total entitlement at each institution.