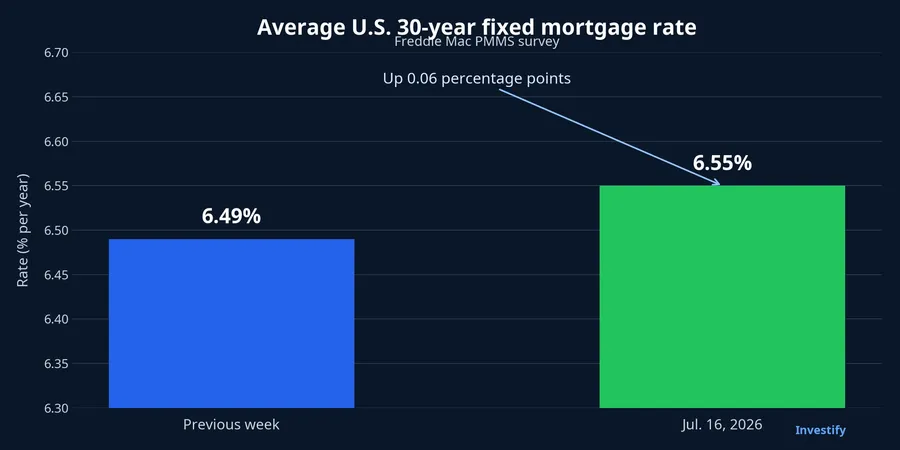

The average U.S. 30-year fixed mortgage rate has risen from 6.49% to 6.55%. That is a Freddie Mac Primary Mortgage Market Survey average, not a quote that every borrower will receive.Freddie Mac Yet the small movement carries a large lesson for new investors: the Federal Reserve influences the cost of money, but it does not sit down and price individual home loans.

Think of the Fed as controlling the valve near the source. Its policies have their most direct effect on very short-term funding. A fixed-rate mortgage is a long pipe: lenders have to assess inflation, growth, bond demand and cash-flow risk over many years. The rate shown in a loan contract is therefore the output of several pricing layers, with the 10-year U.S. Treasury yield usually offering the most visible signal on long-term borrowing costs.

The point is not that the Fed is unimportant. Its role needs to be placed correctly. Policy is one input; bond markets and mortgage-backed securities turn that input into the rate a borrower sees. Separating those layers makes it easier to avoid treating every headline about a Fed meeting as a complete explanation for mortgage-rate moves.

6.55% is a thermometer, not a personal quote

Freddie Mac's PMMS now draws on thousands of loan applications submitted through its Loan Product Advisor system during the week, rather than the older approach of calling a small group of lenders for quotes. The sample focuses on conventional, conforming, fixed-rate loans for one-unit homes and borrowers with strong credit profiles.Freddie Mac

That makes 6.55% most useful as a market thermometer. An actual borrower can receive a different rate based on credit score, down payment, loan size, property type and fees. Freddie Mac also notes that the survey does not report average origination fees and discount points. PMMS should not be used to calculate one household's exact bill. It is better used to identify the direction of long-term borrowing costs.

For the week released on July 16, the average moved up by 0.06 percentage points. A single week does not establish a new trend, especially for a weekly average. It is still worth watching because mortgage rates are where changing long-term expectations pass from trading screens into home purchases, construction decisions and household spending.

The Fed guides overnight money, markets price years ahead

The Fed's policy rate primarily affects short-term money markets and the banking system's overnight funding costs. Expectations for the policy path then spread across longer maturities. Transmission, however, is not the same thing as direct control over the final outcome.

A lender offering a 30-year fixed loan faces a different question: what will cash received in the future be worth? The answer depends on expected inflation, growth, Treasury supply, demand for safe assets and the extra compensation investors require to lock up capital for longer. The 10-year Treasury yield is commonly used as a reference point because a mortgage's actual life is often shorter than its contractual 30 years: borrowers can sell a home or repay early.

This is why two events appearing together should not automatically be turned into a simple causal story. A Fed statement can move long yields when it changes market expectations. Long yields can also move on inflation data, growth prospects or Treasury supply even when the Fed has not changed policy. Both explanations need to remain on the table before assigning a mortgage-rate move to the Fed.

How inflation expectations enter a Treasury yield

One useful teaching tool is to view a nominal Treasury yield as a real yield plus compensation for expected inflation, while remembering that liquidity and risk premia also affect the observed number. The real yield compensates an investor for postponing consumption after inflation. The other component reflects the market's view of purchasing power over the years ahead.

Put simply, if investors fear persistently higher prices, they usually demand a higher nominal yield to protect expected purchasing power. Stronger growth prospects or heavier Treasury issuance can also lift real yields and term premia without an equivalent jump in inflation expectations. A rising 10-year yield can therefore mean different things for equities, bonds and housing depending on what is driving it.

Reading the yield alone is not enough. The more useful question is whether the market is changing its inflation view, its growth view, or the compensation it demands for holding long-dated bonds. The source material does not provide enough evidence to allocate the current week's move precisely among those forces. Recognising that limit prevents an observation of timing from becoming an unsupported causal claim.

Mortgage-backed securities add another pricing layer

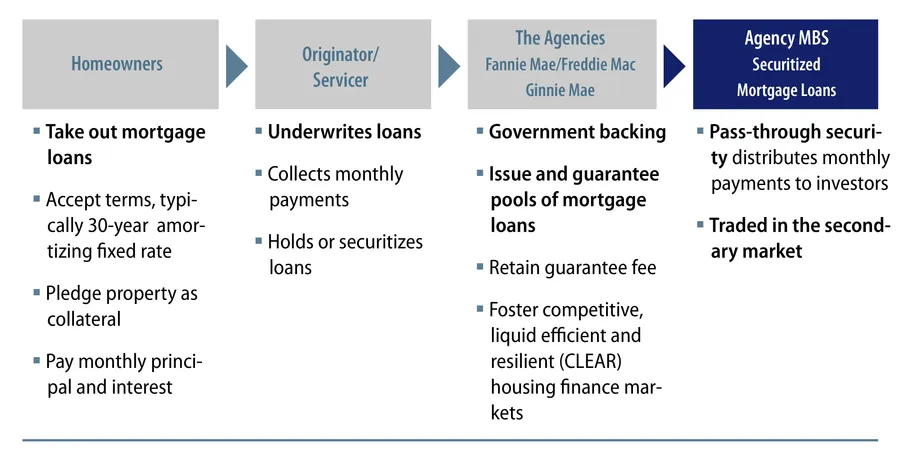

Home loans do not always remain on a lender's balance sheet until the final payment. Many qualifying loans are pooled into securities backed by homeowners' repayments. Investors compare the return on those securities with Treasuries of a similar average maturity, then require an additional spread for the risks and cash-flow features involved. Federal Reserve research describes mortgage-backed security yields as the bridge between long-term yields and primary-market mortgage rates.Federal Reserve

Prepayment is the difficult feature. When rates fall, borrowers often refinance and investors receive cash back when attractive reinvestment yields are scarcer. When rates rise, refinancing slows and cash flows can last longer than expected. This distinctive risk is why the spread between mortgage rates and Treasury yields is never a fixed constant.

Lenders then add underwriting, servicing, capital, hedging and profit costs. A Treasury-yield decline therefore does not guarantee that mortgage rates will fall in the same week. Conversely, mortgage rates may react quickly when demand for mortgage-backed securities or competition among lenders changes.

Three screens to watch together

First, watch the 10-year U.S. Treasury yield. It is not a formula for mortgage rates, but it is closer to long-term funding costs than an overnight policy rate. When it rises, investigate whether the change comes from inflation expectations, real yields or term premia.

Second, watch the spread between mortgage rates and Treasury yields. If Treasury yields fall while PMMS does not follow over several weeks, the mortgage-backed security layer or lender costs may be slowing transmission. A narrowing spread may reflect stronger demand for those securities or tougher lending competition, but more evidence is needed before choosing between those explanations.

Third, follow the PMMS series across several weeks instead of reacting to one data point. The series shows whether a change is becoming a sustained shift in borrowing costs or remains a short-lived fluctuation. For Vietnamese investors, this offers a clearer view of the global backdrop than trying to predict the Fed's next decision from one headline.

The conclusion is that a 6.55% mortgage rate is not a Fed button being pressed. It is a price created by several market layers: inflation and growth expectations enter long yields, mortgage-backed securities add cash-flow risk, and lenders add real operating costs. The thesis is straightforward: start with the 10-year yield, then read the mortgage spread and the PMMS series. Together, they reveal changes in long-term funding costs more clearly than any single Fed headline.