For a steelmaker, producing container shells can look like a detour from the core business. It is better understood as a logical extension of the value chain: weathering hot-rolled coil becomes the walls, roof and floor of freight equipment. For investors following HPG, the question is not whether Hoa Phat can manufacture containers. It is how far its in-house steel advantage has travelled toward the income statement.

On July 17, Hoa Phat said it had delivered more than 4,000 container shells in Q2 2026, showing that the plant has cleared the first hurdle of getting product into the market. That matters because a new production line only gains economic meaning when customers accept its output and put it to work. The delivery figure, however, does not disclose revenue from the business or its profit margin.Người Quan Sát

The central conclusion is therefore narrow: containers are a downstream outlet with a sound industrial rationale for Hoa Phat, but not yet a proven earnings driver. To avoid turning an operating milestone into an early financial forecast, investors should separate three layers of evidence: market acceptance, cost advantage and reported financial performance.

More than 4,000 shells are a market test passed

A container shell is not a product that can be sold simply because it meets a dimension standard. It works outdoors, faces salt air and impacts, and is stacked within international shipping networks. Customers therefore need to assess material durability, welding, coating and operating performance before equipment enters a fleet or leasing portfolio.

Hoa Phat said Hapag-Lloyd and CMA CGM had received its products, while the report also named Touax and Textainer among container-leasing companies. Its Vietnamese customers include transport, port and logistics businesses such as Hai An, VIMC Lines, Tan Cang Sai Gon, Vinafco, Vsico and Vietsun.Người Quan Sát The defensible conclusion from those names and the delivery number is commercial acceptance, rather than capacity that exists only on paper.

But a customer list is not a substitute for contracts and financial reporting. Investors do not yet know the volume split by customer, the value of each order, the share that is trial versus repeat business, or the realised selling price. A shipping line taking delivery is a positive sign on standards. An earnings conclusion requires evidence on price, volume and recurring demand.

That distinction is especially important in a cyclical shipping market. Demand for replacement equipment, cargo turnover and customers’ leasing plans can all shift. A plant can therefore be commercially active without delivering a stable margin through every phase of the cycle. The available evidence establishes commercialisation; it does not permit a precise attribution of a new business line’s contribution to Hoa Phat’s consolidated outlook.

In-house steel is an input advantage, not the final result

Container shells use SPA-H weathering hot-rolled coil rather than conventional steel. Hoa Phat makes that grade within its steel chain and then supplies it to the container plant. This setup gives the group more control over quality, delivery schedules and coordination between production stages.

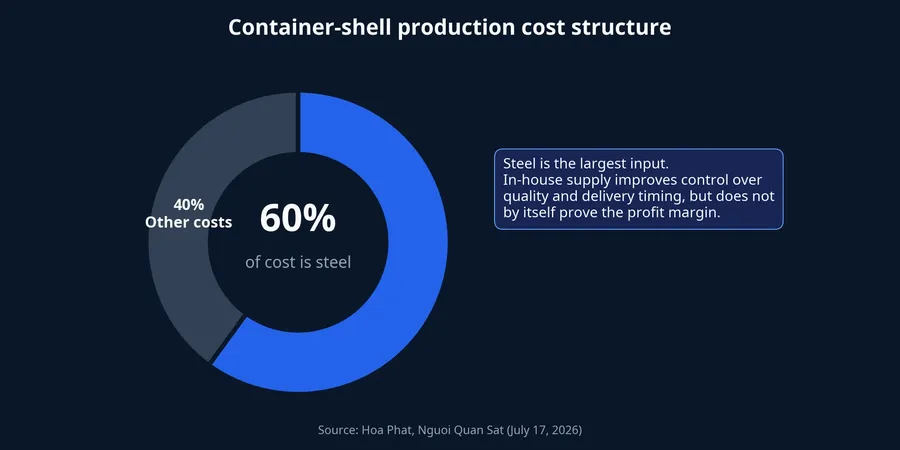

Steel accounts for approximately 60% of container-shell production cost, according to information published on July 17.Người Quan Sát That is why in-house supply is material: it controls the largest cost component and reduces the risk of disruption when sourcing specialised steel externally. It may also make order fulfilment more predictable when a customer requires tight delivery timing.

Hoa Phat put the local-content ratio for container-shell materials at approximately 90%.Người Quan Sát This strengthens the case for supply autonomy, but it does not automatically become a margin premium. Material waste, fittings, paint, labour, line productivity, depreciation and selling costs still matter. The selling price customers will pay determines how much of the input advantage remains with the manufacturer.

In other words, Hoa Phat has a plausible cost mechanism for entering this industry. There is still no segment revenue or gross-profit disclosure to show that the mechanism produces a better return than selling hot-rolled coil directly. For a new line of business, that boundary matters: an operational advantage is a premise, not a financial conclusion.

This distinction also protects against a common analytical shortcut. Vertical integration can make delivery more reliable and reduce exposure to external suppliers, while the financial return from the downstream product remains modest during ramp-up. The two statements can both be true. A useful future disclosure would show not only total shipments, but how the steel supplied internally is priced and how the container line absorbs its fixed costs as volume develops.

Delivery volume cannot be divided straight into capacity

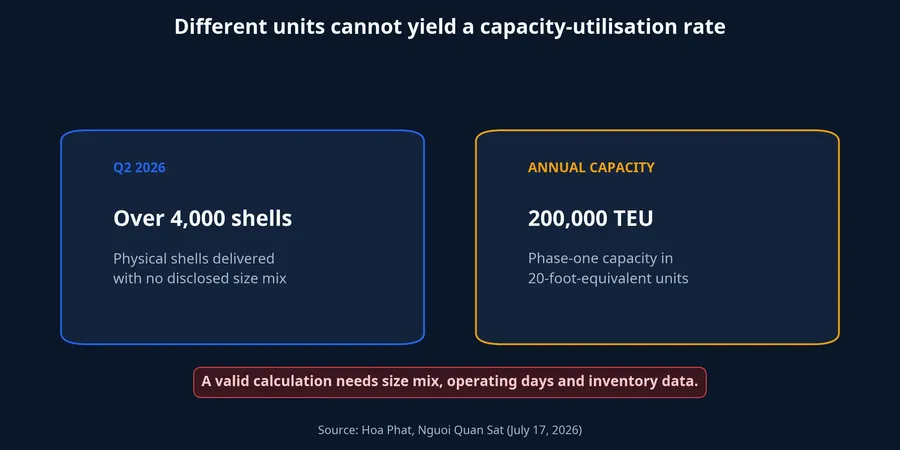

A tempting calculation is to divide more than 4,000 shells delivered in Q2 by plant capacity. It is not reliable because the measures use different units and periods. Deliveries are physical shells in one quarter, whereas phase-one capacity is 200,000 20-foot-equivalent units per year. Total design capacity is stated as 500,000 equivalent units per year.Người Quan Sát

A larger shell consumes more equivalent capacity than a standard small shell. Without the size mix, converting physical shells into equivalent units would be speculation. Moreover, a shell delivered during the quarter may have been produced earlier, while completed product may still await customer acceptance. Factory output and beginning and ending inventory are needed to connect production activity with deliveries.

The cautious conclusion is not that the delivery milestone lacks value. It does matter because it demonstrates commercial operations at the plant. What should be avoided is presenting it as a seemingly precise utilisation rate built from non-comparable measures. A valid comparison will only be possible once the company discloses enough operating detail to put production, deliveries and annual equivalent capacity on the same basis.

What would make containers relevant to an HPG earnings case?

The evidence needs to progress in sequence before the assessment can move from “commercial outlet confirmed” to “earnings driver”. First comes sustained delivery volume over several periods, with a disclosed size mix that enables conversion. Next comes proof of repeat orders and a customer base that is not overly dependent on a small number of contracts.

The decisive missing pieces remain container revenue, gross profit and margin. Once those are disclosed, investors can compare the value added by downstream manufacturing with selling the steel input. Shipping demand and input costs will then show whether that margin can hold.

For F0 investors, this is less a call to decide on a share than a framework for reading the next disclosure. Start with whether shipments persist, then look for repeat customers, and finally ask whether revenue and gross profit are reported separately enough to test the economics. That order prevents a familiar name or a large-looking unit number from doing more analytical work than it deserves.

The current thesis should remain proportionate: Hoa Phat has credible evidence of demand and an input advantage that fits container manufacturing. The main risk to this thesis is not a lack of sales, but the gap between activity and profit. Future reports, especially those on revenue, margins and repeat orders, will show whether in-house steel has completed the journey from the factory floor to reported earnings.