On July 16, the Bank of Korea raised its base rate from 2.50% to 2.75%, its first increase since January 2023. All seven members of the Monetary Policy Board voted for it. This was not a knee-jerk response to one oil session or one volatile equity day. It reflected a changed policy calculation: inflation remains sticky, the exchange rate remains sensitive, and semiconductor exports give the economy more room to absorb a higher cost of capital.Bank of Korea

The broader picture is a collision of two forces. South Korea imports energy and is therefore exposed when oil rises or the won weakens. At the same time, a powerful chip-export cycle means policymakers do not face the same stark choice between controlling inflation and protecting growth that they would in a weakening economy. The central point is straightforward: semiconductors did not cause the rate hike, but they provided a buffer that made it more feasible.

What one rate hike changes

The policy rate is a central reference point for the economy's funding costs. A rise usually puts upward pressure on lending rates, short-dated bond yields and the cost of raising capital. The aim is not to make prices fall the following week. It is to cool demand and to stop businesses and households from assuming that elevated prices will persist.

The July 16 decision matters because it ended a period of more than three years without a rate increase. The Bank of Korea said June CPI rose 3.2% year on year, while core inflation stood at 2.5%. It judged that elevated costs and exchange-rate conditions could continue to pressure prices, and kept its full-year inflation forecast near 2.7%.Bank of Korea

That does not mean a lengthy hiking cycle is certain to follow. The July action is a confirmed fact; the next move still depends on inflation, the exchange rate, growth and financial stability. What markets need to reassess is the central bank's lower tolerance for imported inflation than they had assumed.

Oil reaches inflation through several channels

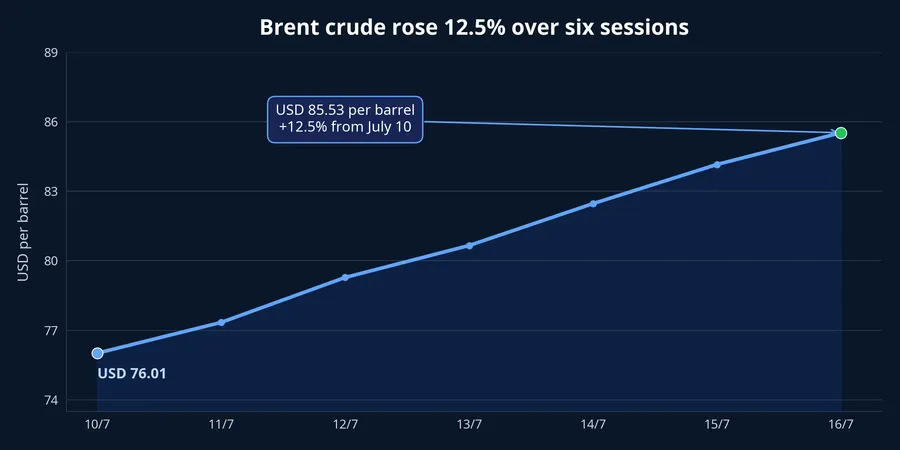

Over the six sessions from July 10 to July 16, Brent crude rose from USD 76.01 to USD 85.53 a barrel, a 12.5% gain. Internal data show a move large enough to keep energy risk in focus for an oil-importing economy such as South Korea. Monetary policy, however, does not follow each commodity session; central banks judge the outlook for prices over months.

The transmission starts with the import bill. More expensive oil lifts fuel and transport costs, which can then move into goods and services prices. If companies expect those costs to last, they may revise selling prices; if households expect living costs to keep rising, wage pressure can build. Once those links reinforce each other, bringing inflation back to target becomes far harder than dealing with a single spike in oil.

Timing and causality need to be kept separate. The week's oil increase signals that energy risk has not disappeared, but it does not prove that oil alone decided the July 16 meeting. The more direct evidence is the statement itself: policymakers pointed to inflation, elevated costs and exchange rates as continuing sources of pressure. Oil is part of that transmission chain, not the whole story.Bank of Korea

A firmer won does not end currency risk

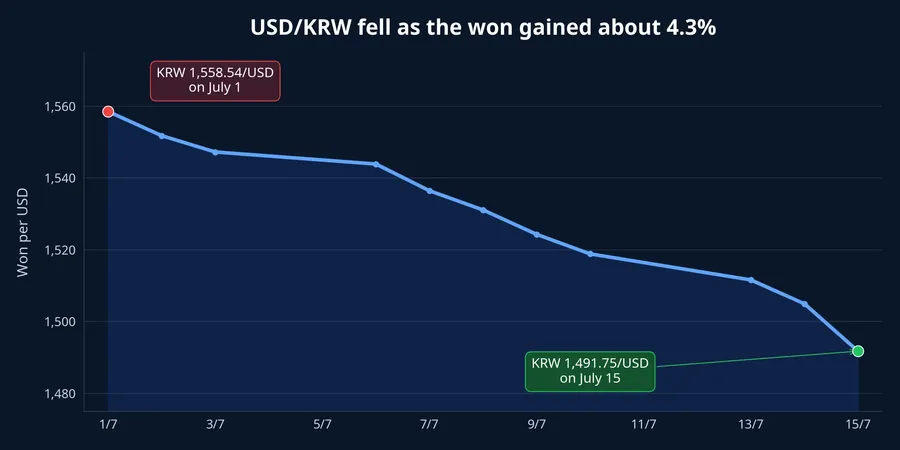

The exchange rate is the second amplifier. From July 1 to July 15, USD/KRW fell from KRW 1,558.54 to KRW 1,491.75 per dollar, meaning the won strengthened by roughly 4.3%, based on internal data. A firmer currency reduces the local-currency cost of imported oil, gas and industrial inputs. That helps inflation, but it is only a snapshot in time.

The won also depends on the dollar, expectations for Fed policy, energy prices and international capital flows. A Korean rate increase can support the won through yield differentials, but it cannot be separated from the rest of the global market. The Bank of Korea still described exchange-rate volatility as high, so treating the won's rebound as the end of imported-inflation pressure would be premature.Bank of Korea

For investors, the chart matters for more than its downward slope. If USD/KRW turns higher while oil remains elevated, Korea's won-denominated energy bill will expand again and strengthen the case for tighter policy. If the won stays stable, markets can instead see July 16 as a precautionary adjustment rather than a response to an urgent inflation problem.

Semiconductors are a buffer, not an inflation cure

Raising rates into weak growth is usually difficult because higher borrowing costs can slow consumption and investment. South Korea has a meaningful buffer in exports. June exports reached USD 102.25 billion, up 70.9% year on year; semiconductor exports alone were USD 44.82 billion, nearly triple the level a year earlier. Yonhap also reported that the Bank of Korea saw this year's growth as potentially well above its 2.6% forecast made in May.Yonhap

The numbers matter because an economy with an export engine can absorb more of the impact from higher funding costs than one relying solely on domestic demand. Profits, investment and orders across the semiconductor supply chain may cushion that impact. This does not mean every Korean company benefits, nor does it mean chips caused higher inflation. It means the growth cost of fighting inflation is lower.

It is important not to push that inference too far. Seoul property prices, household debt and foreign capital flows were also part of the Bank of Korea's financial-stability assessment. Oil, the exchange rate and semiconductors form a persuasive explanation when viewed together, but they are not a single formula that fully explains the policy decision.Bank of Korea

Bond yields and equity valuations tell the next chapter

Before the meeting, the three-year Korean government bond yield was 3.865%, while the comparable AA- corporate bond yield was 4.561% on July 15. Those levels suggest markets had already accumulated expectations of tighter policy before the announcement. The key post-meeting question is whether short yields keep rising, and whether the curve points to persistent inflation or a slower economy under higher funding costs.E-Daily

Equities offer no single answer. The KOSPI closed at 7,284.41 on July 15, up 6.24% for the session, before internal data recorded a 5.9% decline during the July 16 session. There is no basis for assigning all of that volatility to interest rates. Concerns about artificial-intelligence investment, sizeable foreign net selling, profit-taking after a strong session and semiconductor-specific moves are all plausible explanations.Yonhap

The valuation mechanism is nevertheless clear. Higher yields lower the present value of future profits. Growth shares tend to be more sensitive because more of their value rests on earnings further out in time. If chip profits continue to grow fast enough, earnings growth can offset part of the pressure from a higher discount rate. If not, expectations need to adjust.

A practical read-through for Vietnamese investors

South Korea's decision is not a signal to copy directly into a call on the VN-Index. The two markets have different investor bases, valuations and earnings drivers. Its value lies in exposing a regional chain: high oil prices, a weak domestic currency and rising yields can jointly pressure risk assets; strong exports can ease that pressure, but cannot erase it.

The thesis to watch over the next sessions is how closely that chain moves together. Further increases in Korean yields alongside a higher USD/KRW rate and weaker chip shares would favor a scenario in which funding costs overwhelm growth. If the won remains stable while export and chip-profit data retain their momentum, markets have reason to treat the July 16 move as an absorbable precaution. The next inflation data, Brent's path and signals from the Fed will show whether this was a single adjustment or the start of a more extended tightening phase.