On July 16, FPT closed at VND 68,000, its lowest level in roughly two and a half years. That put the share price about 35% below its early-year peak.Znews This is more than a single trading session: the market is asking FPT to show that profit growth can become durable revenue growth across its markets.

The underlying business does not point to a broad-based deterioration. Yet the new accounting treatment for FPT Telecom, the slow pace in the United States and the gap between signed contracts and booked revenue all mean that a lower P/E should be read as a test. The central view is straightforward: FPT still has growth engines, but a valuation recovery needs operating evidence that those engines are producing higher-quality growth.

A lower share price raises two separate questions

A falling share price does not, by itself, establish that the business is getting worse. VND 68,000 sits at the intersection of growth expectations, fund flows and the multiple investors are prepared to pay. For newer investors, the more useful question is not whether the stock is already cheap, but whether upcoming results can close the gap between expectation and execution.

At the July 16 close, FPT traded at roughly 11.96 times P/E, based on trailing four-quarter EPS of VND 5,688. That says the market is paying less for each dong of earnings than it did before; it does not isolate whether the change comes from the share price, lower profit expectations, or both. A low P/E can offer more valuation support. It can also be a discount for growth that still needs to be verified.

It is also important not to assign the entire decline to one cause. Foreign investors sold a net VND 16,500 billion of FPT from the start of the year through July 15; on July 15 alone, net selling was about VND 350 billion as the stock fell 4.98% on volume of more than 21 million shares.DNSE This selling pressure is observable. But portfolio rebalancing, concerns about the technology-services model and earnings expectations may all be at work, and the available evidence cannot precisely apportion their effects.

Reading the accounts after the accounting change

For the first half of 2026, FPT reported revenue of VND 26,269 billion and pre-tax profit of VND 5,714 billion.VietnamBiz Against the unadjusted consolidated numbers from the prior-year period, revenue fell by more than 24% and pre-tax profit by almost 8%. That comparison can make the business appear to be shrinking, but it does not put the two periods on the same accounting basis.

From this year, FPT's investment in FPT Telecom is accounted for under the equity method rather than by consolidating all of its revenue and profit as a subsidiary. On a restated comparable basis, FPT said revenue rose by nearly 13% and pre-tax profit by about 18% year on year. Profit attributable to parent shareholders reached VND 5,055 billion, up 14%, while EPS rose 13% to VND 2,967.Znews

The two sets of figures do not conflict; they answer different questions. Consolidated numbers describe the scale now included in the accounts after the ownership and accounting change. Restated figures describe underlying performance on a comparable basis. For first-time investors, that distinction matters: the decline in consolidated revenue is not direct evidence that customer demand has fallen by the same amount.

The second quarter needs the same treatment. Revenue was estimated at VND 13,789 billion and pre-tax profit at VND 2,910 billion, down more than 17% and 7%, respectively, on an unadjusted consolidated basis.VietnamBiz Profit attributable to parent shareholders still rose by nearly 14%. Investors therefore need to separate a technical reporting effect from the underlying operating trend.

Technology remains the core engine

The technology segment generated VND 23,138 billion in revenue and VND 3,314 billion in pre-tax profit in the first half, up 15% and nearly 17%, respectively, on a comparable basis. After the accounting change, it represented about 88% of FPT's revenue and 58% of pre-tax profit.VietnamBiz The valuation debate is therefore fundamentally about FPT's ability to sustain technology growth, rather than any single consolidated profit line.

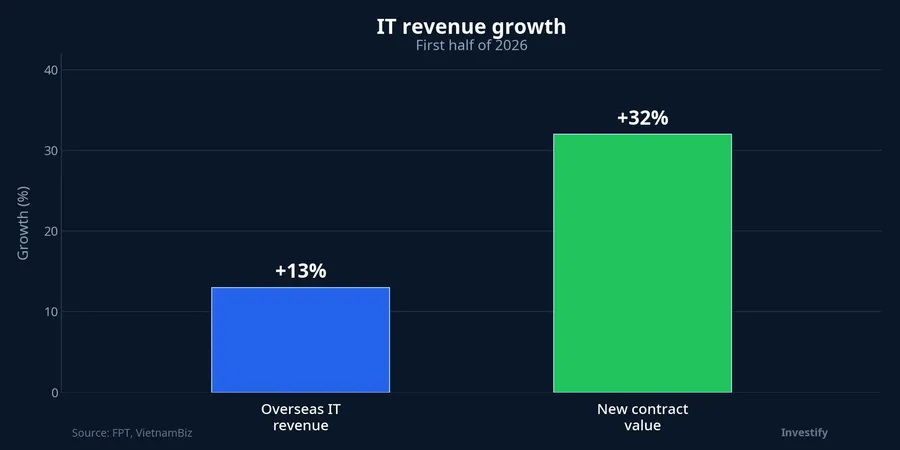

Overseas IT services brought in VND 18,902 billion of revenue, up 13%, while new contract value reached VND 26,338 billion, up 32%, including 14 contracts worth more than USD 10 million each.VietnamBiz Faster contract signing is constructive for future workload. But contracts only become revenue and profit after implementation, acceptance and collection. The gap is therefore a metric to watch, not profit already secured.

If overseas revenue accelerates in the next reporting periods, the market will have stronger evidence that signed work is converting on schedule. If the gap persists, investors should examine implementation timelines and contract mix rather than only the aggregate value signed. That is the difference between a leading indicator and a result already recognised in the accounts.

Artificial intelligence is adding another layer of growth. Revenue from AI services and data analytics was VND 1,842 billion, up 54% and accounting for nearly 10% of overseas revenue. The two AI Factory clusters in Vietnam and Japan operated at more than 90% utilisation and turned profitable in the second quarter.VietnamBiz The data suggest that AI can create additional services rather than only replace jobs. They do not yet prove that the newer business fully offsets pricing pressure in traditional services.

Growth differs sharply by market

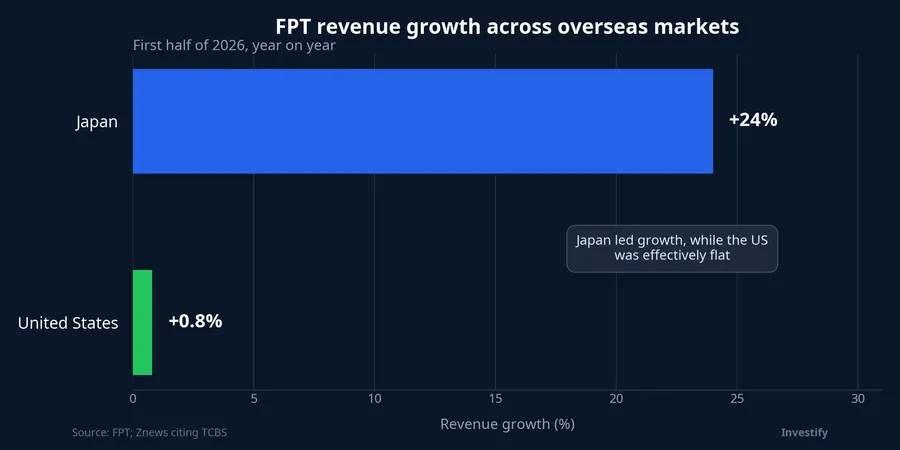

Japan was the clearer bright spot, with revenue there up 24% in the first half. The United States, by contrast, contributed about 23% of software-export revenue but grew only 0.8%. Japan accounted for roughly 43.7% of export revenue, so translated results are also exposed to the yen.Znews This does not negate overall overseas technology growth, but it shows that the quality of that growth is more concentrated in one leading market.

At home, IT services generated VND 4,236 billion in revenue, up 23%, while pre-tax profit doubled year on year to VND 308 billion.VietnamBiz In education, investment and other businesses, revenue fell 2% to VND 3,131 billion, but pre-tax profit rose 20% to VND 2,400 billion, mainly because of joint ventures and associates.VietnamBiz That profit increase should not automatically be treated as a matching improvement in education operations.

Conclusion: a lower valuation is a demand for proof

First-half results represented about 45% of FPT's 2026 revenue plan and more than 49% of its pre-tax-profit plan.VietnamBiz That progress is not enough to say that FPT will either beat or miss its full-year targets. It is enough to focus attention on the right markers: whether overseas technology revenue catches up with new contracts, whether the US improves, and how much profit comes from core operations rather than associates.

The thesis is neither that FPT is cheap simply because its P/E is lower nor that the business foundation has broken down. The current valuation reflects a higher burden of proof. Risks around US growth, contract conversion and the profit mix warrant monitoring, but they do not overturn the evidence of comparable core growth. The next few quarterly reports will show whether the market has grounds to narrow that discount.