Global markets have just received two green signals, but they do not tell the same story. The June US CPI report came in softer than expected and helped technology shares recover. At the same time, Brent crude rose as investors priced the risk of supply disruption around the Strait of Hormuz. Both developments can reach Vietnam, but through opposing transmission channels.

The working thesis for the next session is straightforward: softer CPI supports financial conditions, while higher oil warns of rising input costs. The VN-Index does not have to choose between them immediately. The useful indicators are USD/VND, market breadth and whether money leaves energy shares to spread into interest-rate-sensitive stocks.

Softer CPI changes the cost-of-capital calculation

US headline CPI fell 0.4% month on month in June and rose 3.5% from a year earlier. Core CPI, which excludes food and energy, was unchanged for the month and rose 2.6% year on year. After May's 4.2% annual increase, the report suggested price pressure had eased more broadly, rather than simply reflecting cheaper gasoline.AP

That matters because bonds often react before equities. The yield on the 10-year US Treasury slipped from 4.62% to 4.58% after the report. When yields fall, the discount rate applied to future earnings also falls, which tends to benefit companies whose value rests more heavily on expected growth.AP

This is the context for the S&P 500's 0.4% gain and the Nasdaq's 0.9% advance on 14 July. Micron rose 4.9% and Nvidia added 4.1%. Still, assigning the entire rebound to CPI would be an overreach: stronger-than-expected bank earnings and a recovery following the prior session's selloff are also plausible explanations.AP

In other words, CPI is a constructive signal for financial conditions, not a guarantee of an immediate decline in US policy rates. Markets still need subsequent inflation and employment reports to judge whether the disinflation trend will last. For newer investors, the distinction matters: one favorable release can shift expectations, but it cannot determine the course of monetary policy by itself.

There is a second distinction worth making. Lower yields can improve the valuation backdrop for equities without necessarily improving the operating outlook for every company. A technology stock can respond quickly to a lower discount rate, while a business facing higher freight or fuel bills may face the opposite earnings pressure. The index-level reaction can therefore look calm even when the sector-level implications are sharply different.

Brent is pricing a different risk

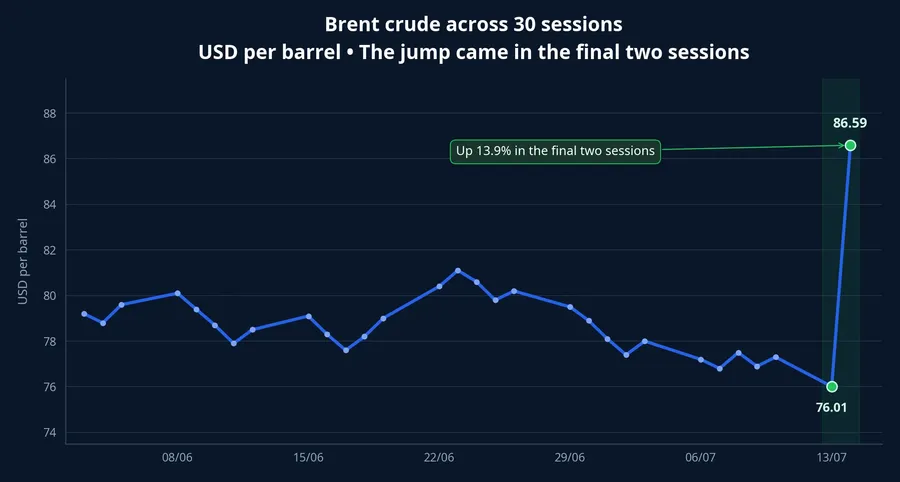

The CPI report is a snapshot of prices consumers paid in June. Oil prices, in contrast, reflect concern over barrels that may or may not move in the days ahead. On 14 July, oil rose sharply after news that the US had reimposed a naval blockade on Iran amid tensions around the Strait of Hormuz. Brent futures were reported up 10.7% intraday at USD 84.20 a barrel.CafeF

Investify's internal data show Brent moving from USD 76.01 a barrel on 10 July to USD 86.59 on 14 July, a 13.9% gain over two trading sessions. That is large enough for markets to reassess fuel-cost exposure, but not enough to declare that consumer inflation will reverse. Time is the bridge between the two stories: oil needs to remain elevated long enough to filter into fuel, transport, goods prices and inflation expectations.

The signals therefore do not conflict. June CPI describes recent inflation; Brent addresses how severely future supply may be constrained. One sharp oil move does not erase the CPI data, just as one encouraging CPI release does not remove a new supply risk.

That timing difference is especially relevant after an abrupt commodity move. Traders can price a potential disruption within minutes, whereas consumer inflation is observed only after costs have worked their way through supply chains and household spending. The appropriate question is not whether a single oil rally has invalidated June's CPI print, but whether the shock persists long enough to change the next several inflation readings.

It also helps avoid a familiar mistake. Rising oil does not mean every energy stock will rise by the same amount, much less that the broader stock market benefits. Each company has different exposure to oil prices, contracts, input costs and pricing power. The opening move on a trading screen is primarily a move in expectations, not proof that reported earnings have already changed.

Vietnam has three transmission channels to watch

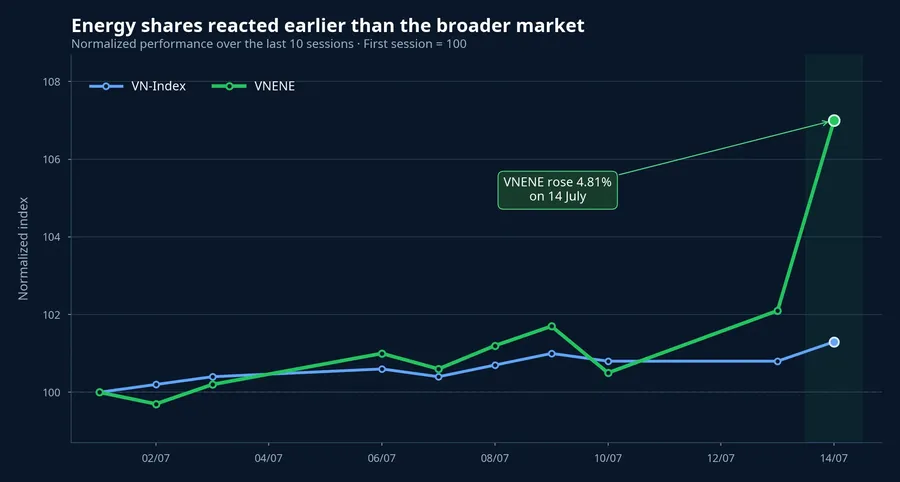

The VN-Index closed at 1,806.63 on 14 July, with 185 gainers and 106 decliners. The market enters the next session from a recovered price base rather than a state of panic. The VNENE energy index gained 4.81% that day, indicating that investors moved first toward businesses more directly tied to oil.

The first channel is energy. If demand broadens across multiple businesses in the value chain, the move will have a wider base. If prices remain concentrated in a few names and then fade with trading activity, it is more likely to be profit-taking on expectations already priced in than a new sector-wide trend.

The second channel is fuel-intensive businesses, including transport and airlines. Higher oil raises costs, but the effect on earnings depends on how long prices remain elevated, hedging arrangements, the ability to pass costs on to customers and domestic pricing cycles. A one-session decline in a transport stock is therefore not enough evidence that its earnings outlook has deteriorated by the same degree.

The third channel is exchange rates and interest rates. USD/VND ended 14 July at VND 26,261 per US dollar, little changed from the prior session in Investify's data. Lower US yields may support sentiment toward equities, real estate and growth shares, but that support is more credible only if exchange-rate pressure does not return. One night of lower US yields does not automatically lower rates in Vietnam.

For Vietnam, the exchange rate is the practical checkpoint linking the global narrative to domestic financial conditions. A stable USD/VND leaves more room for investors to focus on lower external yields. A renewed move in the dollar, by contrast, could keep local funding conditions cautious even if US bond yields remain softer. This is why a broad reading of the market is more useful than tracking Brent alone.

Read market breadth, not one sector

At this stage, market breadth says more than a headline about oil. If USD/VND remains stable, US yields keep falling and buying spreads to rate-sensitive groups, the CPI signal will carry greater weight for the index. Energy's strength would then be one part of the picture, not the whole picture.

The reverse scenario deserves equal attention. If oil continues to surge, exchange-rate pressure builds and transport stocks weaken, the supply shock could outweigh the benefit of lower yields. If energy names rise in isolation while the rest of the market is flat, investors are simply pricing two parallel narratives rather than forming a broad market trend.

The conclusion is not to choose between CPI and Brent. The evidence supports a balanced reading: funding conditions are less restrictive, while energy risk has increased. The next sessions should be read through three signals:

- Whether USD/VND remains stable.

- Whether buying extends beyond energy.

- Whether oil stays elevated long enough to turn expectations into actual cost pressure.