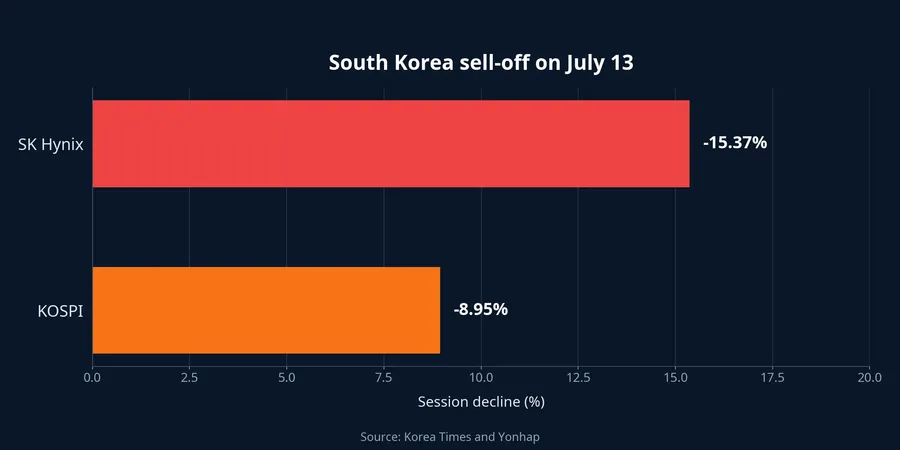

On July 13, SK Hynix shares in Seoul fell 15.37% to KRW 1,845,000, while the U.S.-listed SKHY depositary share remained above the converted value of the underlying Korean share. These are not two prices for two different companies. They are two routes to the same economic interest, serving different investor pools, trading hours and levels of convenience. That distinction matters because a sharp move in one line does not automatically measure a change in the company's operations. Korea Times

The central point is this: the Seoul sell-off is not enough to declare the memory cycle over. What it more clearly shows is that a high valuation is being tested on two fronts. SKHY's access premium can narrow, and earnings must keep beating expectations to sustain the growth narrative.

One company, two ways to hold it

SKHY is a U.S. depositary share, commonly called an ADS. Comparing it with the Seoul share requires the correct depositary conversion ratio and currency conversion; $168 cannot simply be set beside KRW 1,845,000. The comparison is a normalization exercise, not a glance at two numbers on separate screens. Exchange rates, different trading hours, depositary fees and conversion time can keep a gap in place for several sessions.

For a newer investor, the underlying share and the depositary share are not perfect short-term substitutes. They are tied to the same company, but each has its own liquidity layer and trading frictions. A move in SKHY should be separated into the part driven by SK Hynix's prospects and the part driven by the U.S. trading structure itself. That is also why a premium is not a standing guarantee that the U.S. line will deliver a better return.

Why the U.S. price carries a premium

The offering of 177.9 million depositary shares at $149 raised $26.5 billion. SKHY then rose 12.8% to close at $168.01 in its debut session, pointing to strong initial U.S. demand relative to the offer price. AP

After Seoul closed on July 13, the prior U.S. close of $168 was about 37% above the converted value of the Korean share. Early in the July 13 U.S. session, SKHY fell 7.9% to $154.70, yet the premium was still about 25.6%. Euronext

That gap can be read as the price of convenience. The receipt trades in dollars, settles through the U.S. system and gives investors access to SK Hynix without having to handle local currency conversion or Korean market rules themselves. Nasdaq describes its ADR structure as reducing friction from currency, time zones and local-market procedures. Nasdaq

Convenience does not, however, create new company earnings. Investors able to trade both markets have an incentive to buy the cheaper line and sell the dearer one after allowing for currency risk, fees and conversion time. That process may be slow and costly, but it is the force that limits a permanent divergence. SKHY can thus fall because the extra price paid for access narrows, even if SK Hynix's business has not deteriorated.

Seoul's decline was not only about SKHY

Before July 13, SK Hynix stock had more than tripled year to date. A share that has run that far needs more than high profits; it needs profits that exceed what investors already expected. Completing the U.S. listing may have offered some investors a moment to take profits, while some flows may have shifted to the more convenient trading vehicle. Euronext

It would be an unsupported leap, though, to say that the 15.37% decline came only from profit-taking or only from U.S. demand. Korea Investment & Securities forecast second-quarter revenue of KRW 80,900 billion and operating profit of KRW 60,400 billion, roughly 8% below the KRW 65,000 billion consensus. For a stock priced for ambitious outcomes, even a very large result can compress valuation if it falls short of expectations. Yonhap

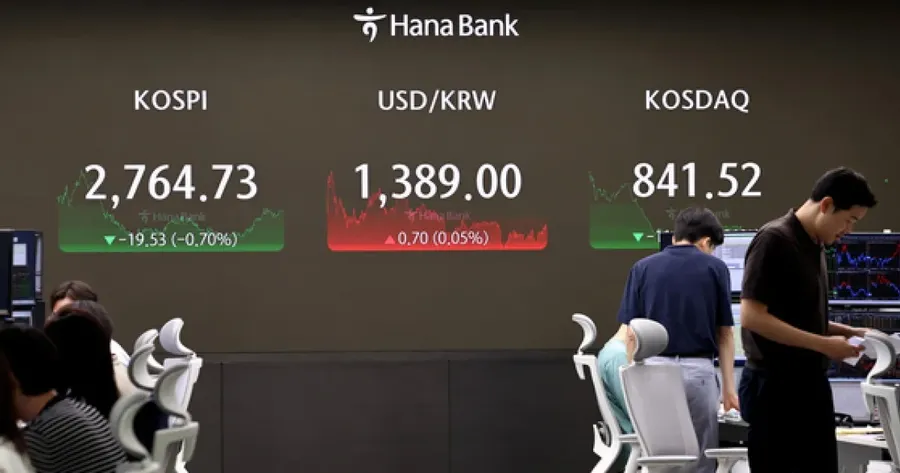

The broader market is another material explanation. The KOSPI fell 8.95% to 6,806.93 and trading was halted for 20 minutes as technology shares were sold amid rising Middle East tensions. The available evidence therefore points to a combination of profit-taking, earnings concern and market-wide risk aversion; it does not precisely allocate the contribution of each factor. Yonhap

HBM leadership still has to become output

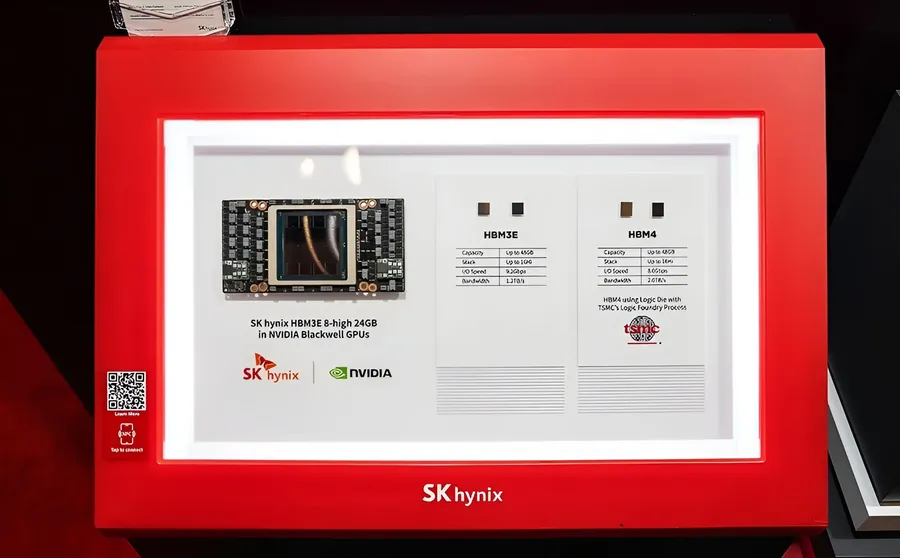

SK Hynix led high-bandwidth memory with 58% of first-quarter revenue market share, while Samsung and Micron each held 21%. That is an important basis for the company's AI-server story because HBM is a critical component for high-performance processors. Euronext

Leadership in one segment does not mean equal gains in every memory-price upswing. When conventional computer memory prices rise, a competitor with more exposure to those products may benefit relatively more. Investors should not use a single statistic, such as HBM market share, as a substitute for the full earnings outlook.

HBM4 is the nearer test. The market had expected output to rise from the second quarter, but the increase had not appeared at the scale anticipated. That may reflect manufacturing progress, packaging or delivery timing rather than weaker demand; still, the gap between expected and actual ramp-up is enough for the market to become more cautious. Euronext

How to read the screen after a volatile session

The second-quarter report should help distinguish a sharp trading day from a genuine change in the business. Rather than looking only at absolute revenue or profit, investors should track realized selling prices, HBM mix and HBM4 delivery progress. A clear second-half increase in output could make a second-quarter disappointment a timing issue; a continued shortfall versus plan would require growth assumptions to be reset.

The longer risk sits in supply. Some analysts expect new capacity in 2027 and 2028 to ease market tightness, while Kwak Noh-jung, Chief Executive Officer of SK Hynix, said 2027 could see the most severe shortage and demand could exceed supply beyond 2030. Those are competing forecasts, not confirmed outcomes; factory investment and new orders will determine which is closer to reality. Euronext

The sensible conclusion today is neither to treat SKHY as identical to the Seoul share nor to read one sell-off as a verdict on the memory cycle. The cross-market premium is a standalone valuation risk, while HBM4 and second-quarter results are the business test. Reading those risks separately keeps a market-structure move from being confused with an operating setback. Over the coming weeks, the converted price gap, quarterly report and evidence on HBM4 output are the signals that will show which part of the expectation remains embedded in the screen.