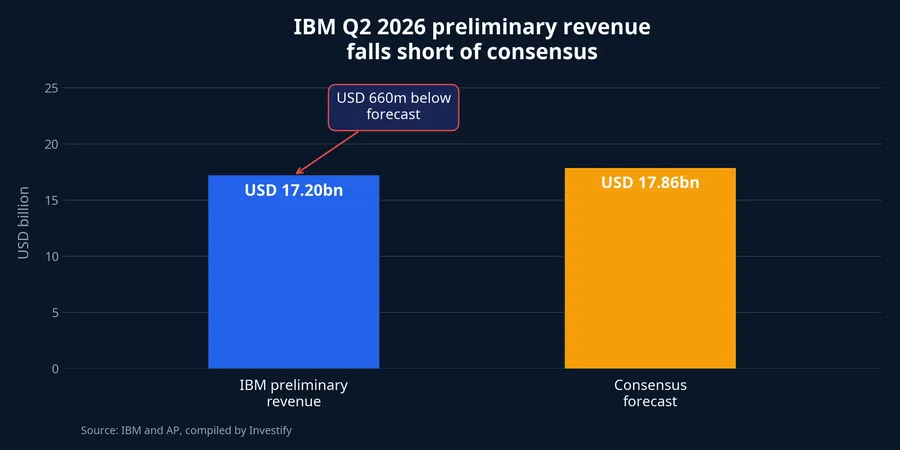

IBM has just illustrated an easily missed feature of the artificial-intelligence investment cycle: customers can increase technology spending while a supplier still misses revenue expectations. In its preliminary Q2 2026 results, IBM estimated revenue of USD 17.2 billion, below the USD 17.86 billion consensus forecast. The USD 660 million gap is modest in absolute terms, but it forces investors to reconsider how quickly customer spending turns into booked revenue.AP

Technology budgets are not a fixed pie apportioned evenly among suppliers. When a company urgently needs servers, storage and memory to expand its AI infrastructure, those purchases can move to the front of the queue. A software contract may still have value, but negotiations, security review and internal approvals can push its signing date into the following quarter. IBM's lesson is not that AI has weakened; it is that capital in an investment cycle does not reach every supplier at the same time.

A modest miss, a much larger market reaction

IBM's preliminary release also put adjusted earnings at USD 2.93 per share, below the USD 3.01 expected by the FactSet-surveyed analyst group. IBM shares fell about 23% in morning trading in the United States on July 14. That response was far larger than the roughly 3.7% revenue shortfall versus consensus, suggesting that investors were repricing both execution and the timing of revenue recognition in coming quarters.AP

Still, a one-day price decline should not be treated as proof that IBM's technology demand has disappeared. A share price reacts to the gap between expectations and results; a revenue report shows where spending was recognized and what has not yet become a contract. The two are connected but not identical. For newer investors, separating these layers helps avoid treating a stock-price move as a final judgment on the entire company.

Why hardware can move ahead of software

In a July 14 letter to investors, IBM said customers prioritized servers, storage equipment and memory in the final weeks of the quarter to secure supply ahead of potential price increases. These are physical inputs needed to build or expand AI processing capacity. When supply must be secured, companies usually need to decide earlier and pay against a clearer delivery schedule.IBM

Software has a different rhythm. Before signing, a large organization often needs to define its requirements, test compatibility with legacy systems, conduct cybersecurity reviews and settle contract terms. If quarterly funding is allocated first to infrastructure, a software project may be delayed rather than cancelled. Lower-than-expected software revenue therefore does not automatically show that customers have abandoned software.

Think of it as renovating a home. If the foundation and frame need work, a homeowner tends to prioritize materials and builders; smart devices can be chosen later. The total renovation budget may still rise, but different vendors receive cash at different times. The same is true in technology: the label “AI beneficiary” is too broad unless it identifies which part of the spending chain a company sells into.

IBM's segments are moving at different speeds

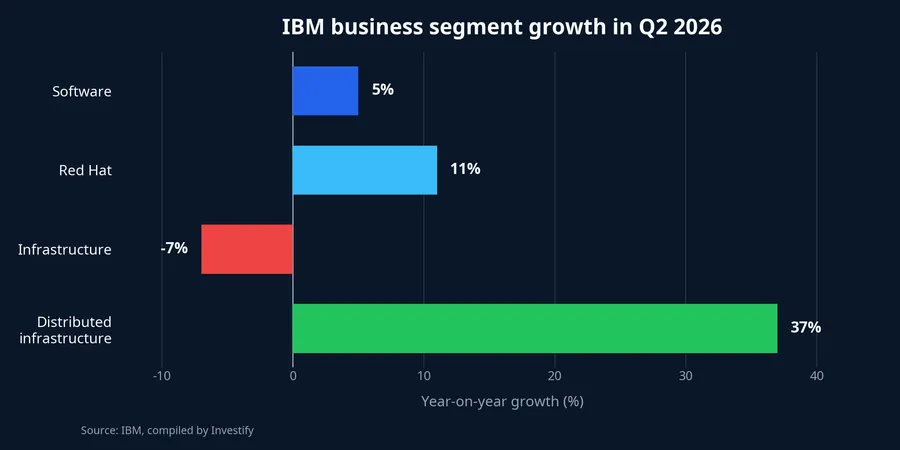

IBM's figures do not tell a simple story of software falling while infrastructure rises. Software revenue still grew 5% year on year and Red Hat grew 11%. By contrast, the overall infrastructure segment declined 7%, chiefly because mainframe Z systems and related software, especially Transaction Processing, came in below expectations.IBM

Within that infrastructure segment, distributed infrastructure grew 37% year on year, its best performance since IBM began reporting the metric. The group's backlog was approximately USD 500 million at quarter-end. Seen together, the numbers show why a segment label alone cannot identify where money is flowing: one product group can expand rapidly while another within the same segment misses plan.IBM

That is also why IBM's result cannot be used to make a blanket claim about every software company. The available evidence confirms IBM's preliminary outcome and its execution issues; it does not allocate the impact across competitors. Differences in products, contract cycles and customer mix can produce very different outcomes. Each company's own reporting is the appropriate test of whether a slowdown is actually appearing elsewhere.

What IBM still has to own

It would also be inaccurate to assign the entire miss to changing customer priorities. Arvind Krishna, IBM's Chairman of the Board, Chairman and Chief Executive Officer, said industry-wide cybersecurity concerns had distracted customers. He also acknowledged that IBM had not reacted quickly enough and that many large deals did not close on schedule, accounting for most of the shortfall.IBM

This distinction matters because it separates two risks. The first is a temporary reordering of customer spending, which may reverse once infrastructure has been purchased. The second is IBM's ability to sell and close contracts. The report does not quantify each factor's contribution, but IBM's own explanation means this cannot be treated as a purely macro AI story.

Profit quality is another metric to watch. IBM's adjusted gross margin declined to 59.4% from 60.1% a year earlier. When the product mix and timing of recognition change, the same dollar of revenue can produce a different amount of profit. For technology companies, rising revenue does not always mean earnings improve at the same pace.IBM

Reading an AI story through the financial statements

Rather than starting with the AI label, newer investors can follow the path of the money. Start with revenue mix: does the company sell servers, memory, subscription software or implementation services? Then examine the pace at which sales opportunities become signed contracts and backlog. Finally, check gross margin, which shows how much value the new revenue retains after cost.

A large pipeline is not yet revenue. If contracts are delayed, the current quarter can miss even when long-term demand remains intact. In contrast, growing backlog and stable close times are more concrete signs that demand is moving from intent into financial statements. This is a more useful approach than grouping all AI-related companies together.

The thesis from IBM is straightforward: AI can still drive technology spending, but the quarterly benefit depends on a company's place in the customer budget and on its ability to close deals on time. IBM's full results call on July 22 is the next test. The indicators worth monitoring are whether delayed large contracts move into the next quarter, how backlog changes, and whether gross margin stabilizes.IBM