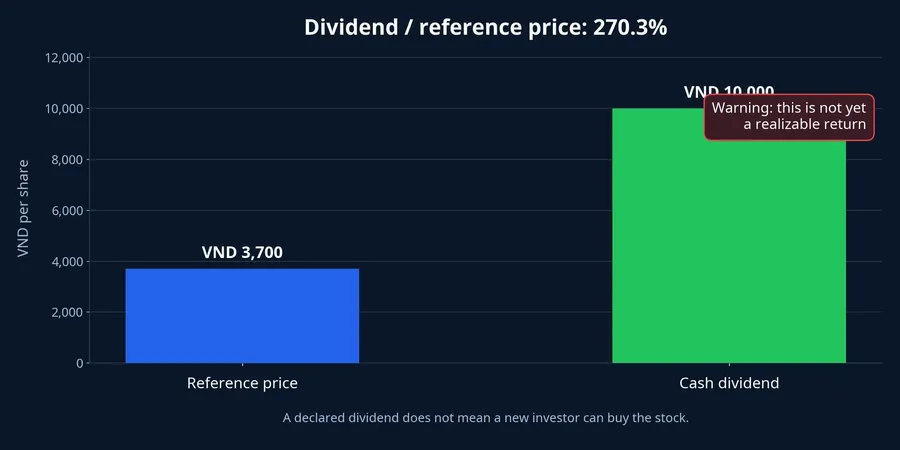

A VND 10,000 dividend on a share with a VND 3,700 reference price produces a 270.3% calculation. It is eye-catching, but it is not a yield that a new investor automatically receives. With FBC, the question that comes before “how high is the yield?” is “can the shares actually be bought?”

Think of it as a price tag in a shop window: it does not prove that the item is in stock. A quoted price only helps an investment decision when there is a seller to enter with and a buyer to exit to. FBC is a particularly clear reminder that liquidity comes before dividend arithmetic.

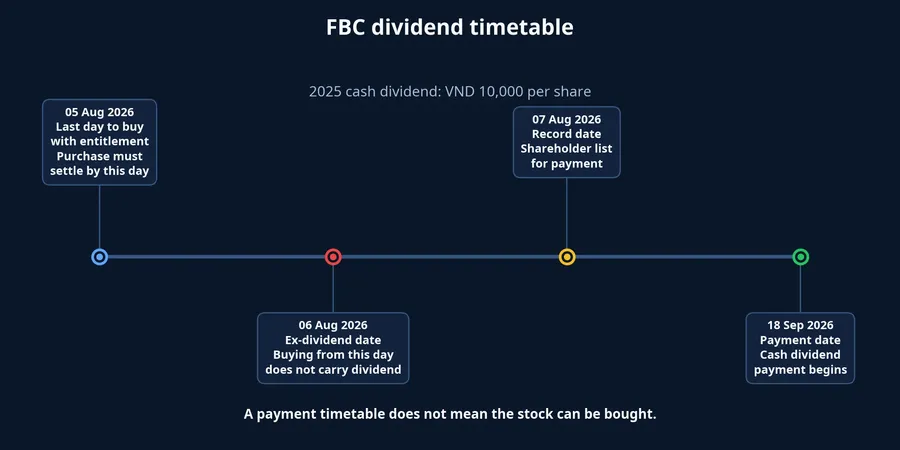

The dividend is declared and the entitlement dates are clear

Vietnam Securities Depository and Clearing Corporation has announced that FBC will pay its 2025 cash dividend at 100% of par value, or VND 10,000 per eligible share. The record date is 7 August 2026 and payment is due to begin on 18 September 2026.VSDC

To appear on the payment list, a purchase must settle no later than 5 August. The stock goes ex-dividend on 6 August, so buyers from that date onward do not receive this dividend.CafeF That is an entitlement rule, not a promise that shares will be available for purchase before the deadline.

Another frequent misunderstanding is to treat a 100% dividend as a guaranteed 100% gain on a new buyer’s cash outlay. The percentage is calculated on the VND 10,000 par value, so it translates into VND 10,000 in cash per eligible share. The actual return on a position still depends on the execution price, fees, tax and the ability to sell afterward.

Why 270.3% is not a realizable yield

The VND 3,700 reference price makes VND 10,000 divided by VND 3,700 equal to roughly 270.3%.CafeF The arithmetic is correct. Its hidden assumption is that an investor can buy immediately at VND 3,700 and later sell when desired. A reference price alone guarantees neither condition.

A reference price is a technical marker, not an offer to sell. With no sell order, a buy order placed at the reference level may remain unfilled for a long time. Raising the bid only records a willingness to buy; it does not create stock on the offer.

The problem does not end if an investor somehow acquires FBC and qualifies for the payment. The dividend is real cash for existing shareholders. But the economics of the whole position still include the entry cost and the exit route. A hard-to-sell share can leave the remaining value difficult to turn back into cash even after the dividend arrives.

What FBC's quote screen does not establish

Investify's internal data records 2,179 sessions in FBC's UPCoM trading history, yet only 10 sessions showed any volume. Six were order-matched sessions and four were negotiated trades, leaving order-matched sessions at about 0.3% of the full series. The last order-matched trade was on 17 May 2022 for 100 shares; no later matched session was recorded through 14 July 2026.

The figures suggest more than merely low liquidity. The ticker has almost no continuous order-matching market through which a new investor can observe supply, demand and an executable price. That is why VND 3,700 should not be read as a purchase price without an observable ask and an actual transaction.

Several explanations for the absence of trading are plausible, including a small free float, incumbent holders unwilling to sell, or little buying interest. Transaction data alone cannot determine which explanation dominates. What it does establish is the outcome: an old reference price is not evidence that an outsider can access the shares.

What the announced payment does and does not tell investors

The formal notice answers a narrow but important question: an eligible shareholder is due VND 10,000 per share on the stated payment timetable. It does not answer what a new buyer would have to pay to acquire a share, whether an order can be filled before the record date, or what the residual holding could be sold for later. Those are market-access questions, and they require observable orders and completed trades rather than a historical quote.

This distinction also separates a corporate action from an investment result. A company can execute a disclosed cash payment exactly as announced while a buyer still fails to realize the headline percentage because the buyer could not enter at the reference price. Existing shareholders and prospective buyers are therefore looking at the same dividend through different economic constraints.

The ex-dividend price is not a mechanical subtraction

It is also wrong to subtract VND 10,000 from VND 3,700 and conclude that the post-entitlement reference price must be negative or mechanically collapse to a minimum. That ignores the UPCoM pricing mechanism. Under the rules for registration and trading management of unlisted securities issued with Decision 23/QD-HDTV in 2025, the normal reference price is tied to the volume-weighted price of board-lot continuous matched trades on the preceding trading day. The rules also provide a 40% trading band, with no reference-price adjustment, where a cash dividend is at least as large as the relevant price.Hệ Thống Pháp Luật

Put simply, the mechanism provides room for the market to discover a price rather than forcing an absurd subtraction. A wider band, however, cannot substitute for buyers and sellers. If orders do not meet, there is no fresh trade to test what price fits the stock after the ex-dividend date.

For that reason, HNX notices and the live quote screen on 6 August are the relevant places to watch the operational mechanics. They may show how the ticker is handled technically. They still cannot answer whether there is an opposing order.

How to read an exceptionally high dividend yield

When a yield looks extraordinary, do not begin by multiplying an expected profit. First check whether there have been recent trades, how much matched volume there was, whether both bids and offers exist, and how wide the gap is between them. For an infrequently traded share, each of those conditions matters more than a reference level carried on the screen.

Only then should an investor check the entitlement timetable, payment amount and the formal disclosure. For FBC, the dividend timetable has been formally announced. The constraint for someone who does not already own the stock is whether shares can be acquired before the ex-dividend date, not whether “100%” can be interpreted as a certain return.

The FBC case supports one clear conclusion: a cash dividend larger than a reference price does not automatically create a realizable investment return. Illiquidity does not negate the payment entitlement of existing shareholders, but it reverses the analytical order for outsiders. Dividend yield becomes an investment number only after the market confirms an executable way in and out.