After the July 13 sell-off, anyone still holding VN30F2607 entered a period fundamentally different from intraday trading: the position remains open after the bell, while the ability to respond does not. VN30 fell 30.98 points, or 1.57%, while the July futures contract closed at 1,941.5, down 1.77%.Thời báo Tài chính VN With expiry due on July 16, the useful question is not whether the next morning will be green or red. It is whether the account can absorb an opening move against the position, with cash and a plan already in place.

Put simply, holding overnight swaps immediate control for the chance to stay with an investment view. The cost is exposure to out-of-hours news, moves in other markets, and an opening price that can differ materially from the prior close. In futures, that gap matters more because profit and loss are amplified by the contract multiplier, while the initial cash posted is margin rather than the full notional value.

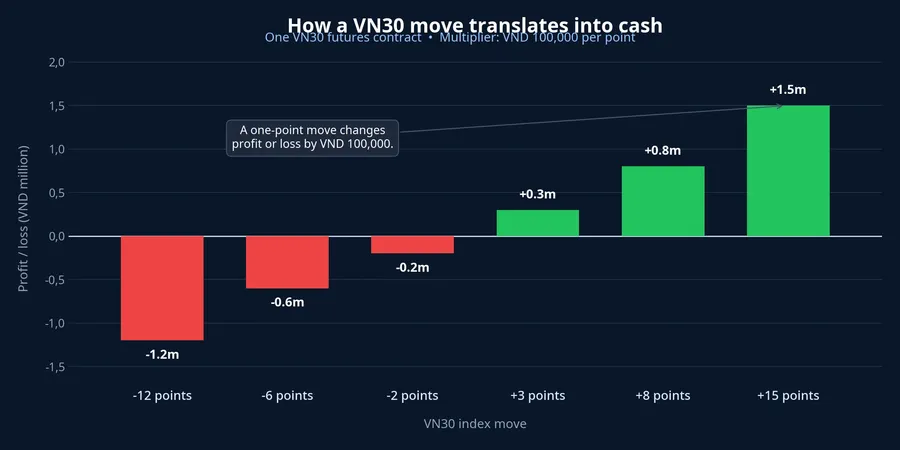

A point is not small when leverage is involved

The VN30 futures contract has a value equal to the index multiplied by VND 100,000 per point. That is a VSDC product specification, not a brokerage estimate.VSDC A 10-point move against a position therefore changes profit or loss by VND 1 million per contract, before fees and taxes. It says nothing about whether a long or a short will be right, but it shows why a modest index move can produce a meaningful cash result.

For example, VN30F2607 fell 35 points, from 1,976.5 on July 10 to 1,941.5 on July 13.Thời báo Tài chính VN For someone who held one long contract throughout that period, the adverse change was VND 3.5 million before fees and taxes. This is not a forecast for the next session; it is a conversion that makes the unit of risk visible.

The common mistake is to take VN30's percentage move and apply it directly to cash margin. Those are not the same thing. Margin controls a notional value larger than the cash initially posted, so the same point move can consume a much larger share of the capital actually committed to the account.

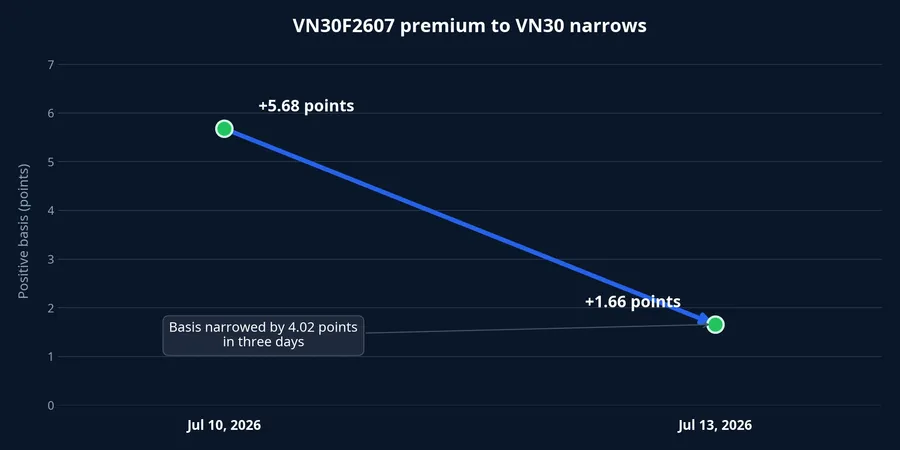

A narrowing basis is not a promise about direction

On July 13, VN30F2607 traded 1.66 points above VN30; on July 10, the positive basis was 5.68 points.Thời báo Tài chính VN Think of this as the distance between the futures price and its underlying index. As the final trading day approaches, settlement mechanics tend to pull the two closer together, but that does not tell investors whether VN30 will rise or fall.

For a short seller, seeing a positive basis narrow and then concluding that profit is certain is a leap beyond the evidence. The futures price can fall toward the index, the index can rise toward the futures price, or both can move in the same direction. July 13 data only show broad weakness in the underlying basket, with 27 VN30 members down and three up, alongside a narrower basis for the near-month contract.Thời báo Tài chính VN They do not establish the driver of each position or forecast the direction of expiry-day trading.

Trading volume in VN30F2607 rose 41.7% to 194,462 contracts on July 13.Thời báo Tài chính VN High turnover can reflect closing trades, fresh positions, or rolls into the next maturity. Since every futures contract has a buyer and a seller, a large volume number alone cannot tell an investor which side has the advantage.

Expiry changes the mechanics, not the need for risk control

The final trading day for a VN30 futures contract is the third Thursday of its expiry month. For VN30F2607, that is July 16, 2026.VSDC The contract is cash-settled, so a holder does not receive a basket of VN30 shares. That distinction matters for newer investors: expiry closes the contract under a prescribed rule; it does not automatically turn it into stock ownership.

The final settlement price is also not simply the index level visible at one closing moment. Under VSDC rules, it is the arithmetic average of the index in the final 30 minutes of the final trading day, including 15 minutes of continuous matching and 15 minutes of the closing auction; the three highest and three lowest readings from the continuous period are removed.VSDC This explains why the near-month contract must converge toward the index, but it does not turn expiry into a formula for predicting market direction.

Expiry-day rumours often make the story sound simpler than it is. Closing and rolling positions can make trading busier, but the index direction still depends on supply and demand across the VN30 basket and on information emerging during the session. Instead of assigning every move to expiry, a holder should separate what is known, the settlement rules, from what remains unknown, the price path.

Four checks before leaving an order open overnight

1. Name the position's purpose accurately. Selling futures is a hedge only when an investor owns an underlying portfolio that moves broadly with VN30 and contract size is intended to offset part of that portfolio risk. Without a corresponding underlying asset, it is a leveraged directional position. The labels lead to different expectations, but only one describes the risk honestly.

2. Convert the loss limit into points. Divide the maximum cash loss acceptable on one contract by VND 100,000 to obtain the adverse point move that can be tolerated, before fees and taxes. If that figure is small relative to an opening move the investor considers plausible, the problem is position size rather than the forecast. Do this before the market closes, when the decision is not being shaped by a live loss on the screen.

3. Check the margin cushion in the actual account. The minimum margin requirement is not the entire risk budget. Each brokerage has its own warning thresholds, collateral calculations, and deadline for additional margin, so investors need to review the rules applicable to their own account. A cushion that is too thin can force a position to close before the original view has a chance to be tested.

4. Decide how to handle July 16 in advance. If the hedge remains necessary after expiry, compare the cost and basis of the next maturity before the last minute. If the purpose is only to anticipate a rebound or a further decline, call it what it is: a leveraged bet, with a matching loss limit. This plan cannot make price cooperate, but it prevents the expiry calendar from becoming an operational surprise.

The conclusion to keep

VN30F2607 is close to expiry, so its basis to VN30 is data to monitor, not a signal to make a one-way bet. The core conclusion is simpler: holding overnight is defensible only when the position's purpose is clear, the loss limit has been converted into points and cash, the margin cushion is adequate, and the expiry plan is already decided. This discipline matters most when the market is moving quickly and a tempting narrative is replacing arithmetic. Without one of those conditions, the risk is no longer just market movement; it is an incomplete calculation in the account.