On July 14, JPMorgan Chase, Bank of America, Citigroup, Goldman Sachs and Wells Fargo are scheduled to release their second-quarter results before Wall Street opens. The calendar matters because these five banks sit at several of the US economy's busiest intersections: consumers swipe cards, companies borrow, investors trade, and corporations raise capital. Kiplinger

For newer investors, a bank report can look like a simple test of whether earnings per share beat expectations. That number is only the cover page. What matters more is how the profit was made and whether customers are still servicing their debts. The central idea is straightforward: Q2 results become evidence of a healthier US economy only when consumer demand, credit quality and banks' revenue sources tell a consistent story.

Why one reporting day can say more than share prices

Banks are where household and corporate cash flows pass every day. Card purchases, deposits, mortgages and business credit lines gradually show up in their accounts. These figures are not an opinion poll, but they are a close view of real spending and borrowing behaviour.

Still, five reports should not become a single proxy for the entire United States. JPMorgan Chase and Bank of America have enormous consumer franchises, while Goldman Sachs relies much more on trading and financial advisory. That difference makes line-by-line comparison more useful than adding up group profit and drawing a quick conclusion.

Treat each bank as a different viewing angle before assembling the broader picture. That approach helps prevent an active trading quarter from being mistaken for a lasting improvement in borrowers' financial health.

First read: are consumers spending or borrowing to spend?

Three indicators belong together: card spending, outstanding consumer loans and delinquencies. Rising card spending usually means demand is still present. But if card balances are rising because customers keep debt for longer, while delinquencies and charge-offs increase, that spending is relying more on credit rather than on stronger income.

Think of a household that is still shopping and travelling but repays less of its card balance each month. Spending has not visibly declined, yet repayment pressure is building in the background. Bank reports matter because they show both sides rather than payment volume alone.

A more constructive signal has a balanced shape: spending rises, lending grows at a measured pace, delinquencies remain steady and the bank does not need to set aside much more for expected credit losses. Slower spending with stable delinquencies does not automatically mean recession either. Consumers may simply be more careful, which is why trends over several quarters are more useful than a label drawn from one report.

Corporate credit should be read separately. A company drawing a line to support working capital or invest in equipment signals something different from a household revolving card debt. If business lending is resilient while consumer credit weakens, the economy may be uneven. The reports do not establish a single cause for that divergence, but it would be a meaningful pattern to watch.

Lending income needs to be read with credit quality

Net interest income is the difference between interest a bank earns on loans and interest it pays depositors and other funding providers. Put simply, it is what a bank earns from the traditional business of taking deposits and making loans. It can increase because lending volumes are larger, loan rates are higher or funding costs are lower. An increase alone therefore does not establish that the profit is durable.

After net interest income, look immediately at provisions for credit losses. A provision is money a bank sets aside in advance for the possibility that some customers will not repay. If net interest income rises but provisions rise faster, the bank is earning more from credit while also acknowledging greater risk. Neither line should be called good or bad in isolation; they need to be read together.

Wells Fargo is a practical example. Before the release, analysts expected a 2.44% net interest margin and revenue of $21.85 billion, up 4.9% year over year. Kiplinger If revenue meets that expectation but provisions rise materially or delinquencies deteriorate, the headline figure will not tell the whole story. Stable margins alongside steady credit quality would make that part of earnings more credible.

Do not use provisions alone to declare that customers have already lost their ability to pay. They also reflect management's caution about the outlook. The better reading compares provisions with delinquencies, charge-offs and the explanation in the report. When those indicators deteriorate together, the evidence of credit stress becomes stronger.

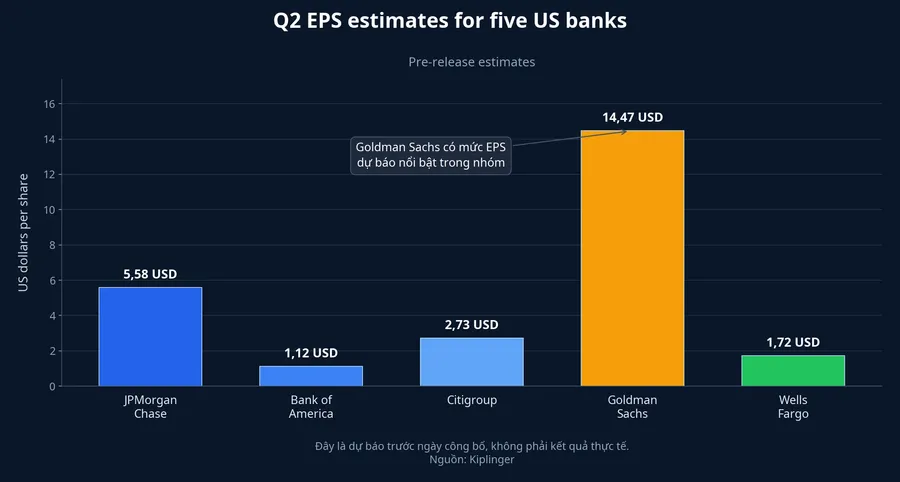

EPS is a reference point, not a diagnosis

Ahead of the reports, the EPS estimates are $5.58 for JPMorgan Chase, $1.12 for Bank of America, $2.73 for Citigroup, $14.47 for Goldman Sachs and $1.72 for Wells Fargo. Kiplinger Those figures are useful because markets often react to the gap between actual results and expectations. A high EPS figure or an earnings beat, however, does not prove that US consumers are healthier.

One bank might beat EPS because trading revenue or advisory fees increased while card credit worsens. Another might miss EPS after deliberately adding to provisions even though current customer data have not materially weakened. This is why a headline about a beat can matter for a short-term share-price reaction yet remain too thin to support a conclusion about the economy.

How much of the result comes from Wall Street?

JPMorgan Chase, Citigroup and Goldman Sachs do more than lend. Their businesses include equity and bond trading, merger-and-acquisition advice, and helping clients raise capital. These activities can produce strong results when markets are volatile or when issuance and corporate transactions are active.

That income is legitimate and central to the large banks' business models; it is not a weakness to dismiss. The problem begins only when readers use Wall Street profit as a stand-in for the whole economy. Strong trading fees can describe lively capital markets, while net interest income, delinquencies and provisions sit closer to borrowers' financial condition.

So if earnings exceed expectations mainly because of trading and advisory, while card spending slows, delinquencies rise and provisions increase, the sound conclusion is that Wall Street supplied much of the brightness. That does not prove the economy has weakened; it means the report has not confirmed broad-based improvement. Conversely, when capital-markets activity rises alongside measured loan growth and stable credit risk, the picture has a wider foundation.

A reading order that prevents EPS from taking over

When results arrive, start with borrowers: card spending, loan balances, delinquencies and charge-offs. Next, combine net interest income with provisions to see whether lending profit is being offset by more credit risk. Only then look at the contribution from trading, advisory and capital raising.

This order is not a recommendation to buy or sell bank shares. It is a way to distinguish three different stories that can produce an attractive earnings headline: healthier borrowers, banks benefiting from interest-rate spreads, or more active Wall Street markets. Q2 data will answer part of the question, but a single quarter still cannot define an entire economic cycle.

The appropriate conclusion for now is to wait for corroborating evidence. The constructive thesis is strengthened only if spending and lending expand at a measured pace, delinquencies and provisions remain stable, and profit is not overly dependent on one capital-markets business. After July 14, the most useful items to monitor are card-credit trends, provision expense and the share of trading revenue in each bank's results.