On July 14, US markets must process two messages in sequence: the June CPI release at 8:30 a.m. Eastern Time, followed by monetary-policy testimony from Kevin Warsh, Chair of the Board of Governors of the Federal Reserve System, before the House Financial Services Committee. The first release shows how consumer prices changed; the second helps explain whether the Fed sees that change as a trend or short-term noise. The Bureau of Labor Statistics (BLS) lists July 14 as the release date, while the House has scheduled the hearing for 10:00 a.m. that day.House Financial Services

This is not a case of guessing one number and trading the first move. The central point before the data arrives is straightforward: a decline in headline CPI is only a necessary condition. A less restrictive Fed outlook needs support from softer core CPI and an explanation from the Fed that price pressure is easing broadly.

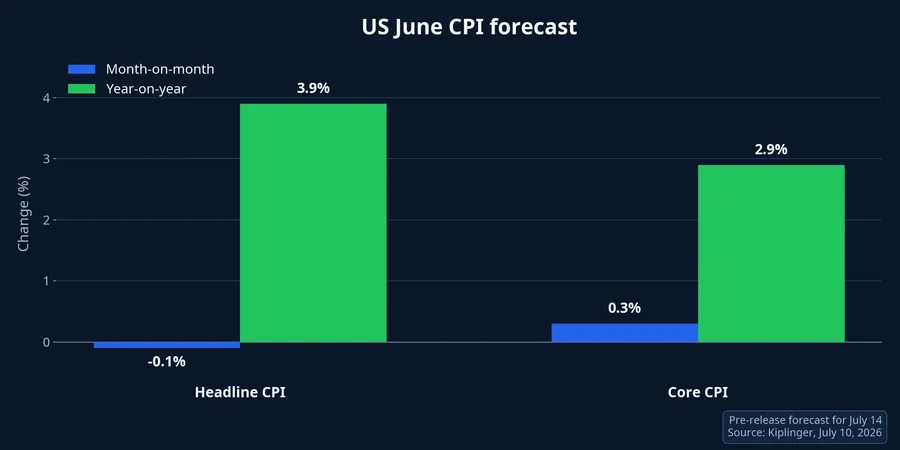

Two measures, two stories

Kiplinger's July 10 preview expects headline CPI to fall 0.1% month on month in June while remaining 3.9% higher than a year earlier. Core CPI, which excludes food and energy, is expected to rise 0.3% for the month and 2.9% year on year.Kiplinger For newer investors, the distinction matters: headline CPI includes highly volatile categories, while core CPI offers a clearer view of more persistent price pressure.

Gasoline can pull the headline measure down for one month without saying much about services, housing, or non-energy goods. A “lower CPI” headline is therefore not enough to conclude that inflation is returning to the desired path. If core CPI matches or exceeds 0.3%, markets can reasonably treat the headline figure as narrow relief rather than a decisive change in the inflation picture.

The forecasts are not yet reported facts. The 0.1%, 3.9%, 0.3%, and 2.9% figures are benchmarks for the July 14 result. The gap between the actual print and expectations, especially for core CPI, often matters more than whether the headline number is negative or positive on its own.

Testimony is the second filter

Warsh's testimony adds another layer of information on the same day. The BLS will report what happened to consumer prices in June. The Fed Chair may clarify how the institution assesses the breadth of price pressure, the balance between inflation and growth, and how much more evidence it needs before policy changes. That is why the same CPI result can produce very different market readings.

Minutes from the June meeting, released by the Fed on July 8, show that all participants agreed to hold rates at that meeting. Their views of the appropriate year-end rate, however, were not uniform: some saw it at or below the current range, while others saw a higher appropriate level. The minutes also reaffirm the Fed's 2% longer-run inflation goal.Federal Reserve

Investors should not assign a single cause to every market move. Higher yields after the testimony might reflect the reading of CPI, the Chair's message, or both. When the evidence does not separate each contribution, the more accurate approach is to treat them as a connected flow of information, rather than claim that one event alone caused the whole move.

A hawkish branch: when core inflation stays firm

A more hawkish outcome becomes plausible if headline CPI falls mainly because of energy while core CPI meets or exceeds its forecast. Markets would then listen for whether Warsh stresses broad price pressure, upside inflation risk, or the need for more evidence before policy changes. This is a condition to watch, not a forecast that the Fed will certainly raise rates.

The first response signal is the two-year US Treasury yield because it is more sensitive to policy-rate expectations than longer maturities. On July 10, the two-year yield was 4.21%, below the 10-year yield at 4.56%.US Treasury A clearer rise in the two-year yield after the data would usually indicate that markets are pricing rates staying high for longer, or an additional increase.

The US dollar is a useful confirmation signal, not independent proof. DXY closed at 100.64 on July 10. A simultaneous rise in DXY and the two-year yield would fit a hawkish reading better. If only one market moves, more context is needed before concluding that the Fed has changed course.

For equities, higher rates raise the discount rate applied to future earnings. Companies whose expected profits lie further into the future tend to be more sensitive, although the actual response also depends on earnings and starting valuations. For fixed-income securities, higher market yields generally pressure prices, especially for instruments with a longer average maturity.

A softer branch needs agreement between data and message

A softer outcome requires more than a negative headline CPI print. Core CPI would need to come in below forecast, while the testimony would need to acknowledge broader easing or place greater weight on growth and employment. When both layers point in that direction, expectations for rate increases have firmer grounds to recede.

In that case, the two-year yield could fall faster than the 10-year yield as markets reprice the near-term policy path. A weaker DXY would reinforce that reading. Gold closed at USD 4,105.30 per ounce on July 10; lower rates and a softer dollar usually reduce the opportunity cost of holding gold, but they do not explain every move in the metal.

That is where new investors should resist oversimplifying. Gold also responds to demand for protection and geopolitics. The 10-year yield also includes growth expectations and a term premium. Equities have an earnings season to process. CPI and testimony may be the leading drivers on the day, but they are not a master key for every asset class.

Bringing the signals back to Vietnam

The transmission to Vietnam is not one for one. A stronger dollar can add pressure to the exchange rate; higher international yields can lift the return demanded by global capital and weigh on asset valuations. Domestic interest rates, however, also depend on banking-system liquidity, credit demand, and policy management by the State Bank of Vietnam.

A practical reading order is to start with core CPI, then the two-year yield, then DXY. A conclusion has more support only when all three point in the same direction. If CPI appears softer but yields and the dollar rise, markets may be focused on details inside the report or on the hearing message; it is too early to label that a softer policy signal.

For holders of fixed-income instruments, maturity remains the basic distinction: shorter-maturity instruments are generally less sensitive to yield changes than longer ones. For equities and gold, the more useful observation is not the first green or red move, but whether it persists after both the data and the Fed's explanation are available.

The conclusion is an explicit conditional wait, not an evasion. Lower headline CPI is not enough to soften the Fed. That view changes only if core CPI undershoots expectations and the Fed's message confirms broad-based easing in price pressure; otherwise, the two-year yield and DXY are the two measures to watch for how markets price the rest of the story.