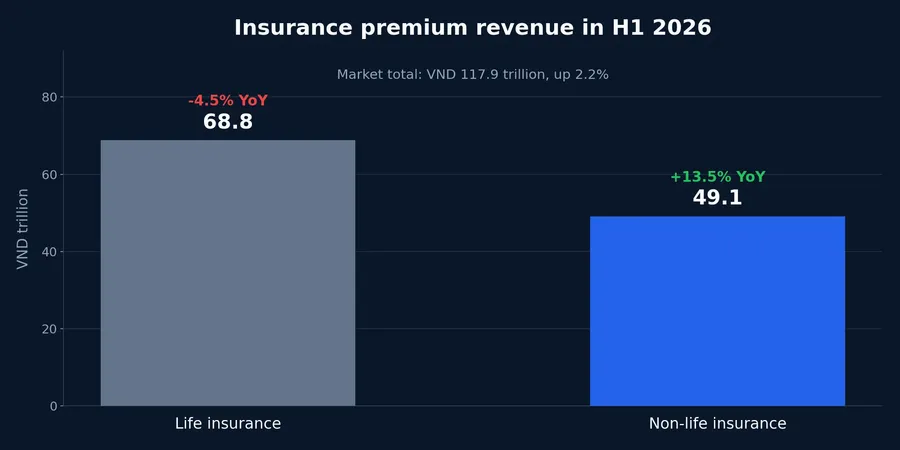

Vietnam's insurance market is offering a useful lesson in why a headline number can conceal two very different stories. Total premium revenue was estimated at VND 117.9 trillion in the first half of 2026, up 2.2% year on year. Yet life insurance brought in VND 68.8 trillion, down 4.5%, while non-life insurance reached VND 49.1 trillion, up 13.5%.Doanh nghiệp Kinh tế Xanh

That is not a contradiction that requires choosing one segment as healthy and the other as weak. The two businesses sell different promises, meet different needs, and build revenue on different timetables. The central point is simpler: premiums are diverging, but value for shareholders will still be determined by the quality of earnings after claims, expenses, and reserves.

Non-life insurance follows assets and activity

Think of non-life insurance as protection for risks that already exist in the real economy. Cars, cargo, construction projects, factories, machinery, and third-party liability are generally covered over shorter periods and attached to an identifiable asset or transaction. As the stock of assets requiring protection rises, premium revenue can respond relatively quickly.

Property and engineering insurance were the principal sources of non-life growth in the first half.Doanh nghiệp Kinh tế Xanh A new construction site needs cover while work is underway. A factory expansion adds equipment, inventory, and business-interruption risks. Asset-backed lending may also bring protection needs alongside the loan. That chain helps explain why non-life premiums can grow early in a more active investment, production, and transport cycle.

Bank distribution is an important advantage for some insurers, but it should not be turned into an industry-wide conclusion. Seven insurers with a parent bank or a major banking shareholder hold about 35% of the non-life market, according to Thời báo Tài chính Việt Nam.Thời báo Tài chính Việt Nam A ready-made network can connect an insurer with borrowers and assets that need cover. It does not, however, prove that the resulting policies are inexpensive to sell, properly priced, or durable.

Life insurance is rebuilding its new-business model

Life insurance works differently. A customer is not simply insuring a car or a shipment for a year. They are entering a multi-year contract in exchange for future protection or savings benefits. Confidence in the advice, clarity of policy terms, and the claims experience therefore have a direct bearing on whether customers sign and retain policies.

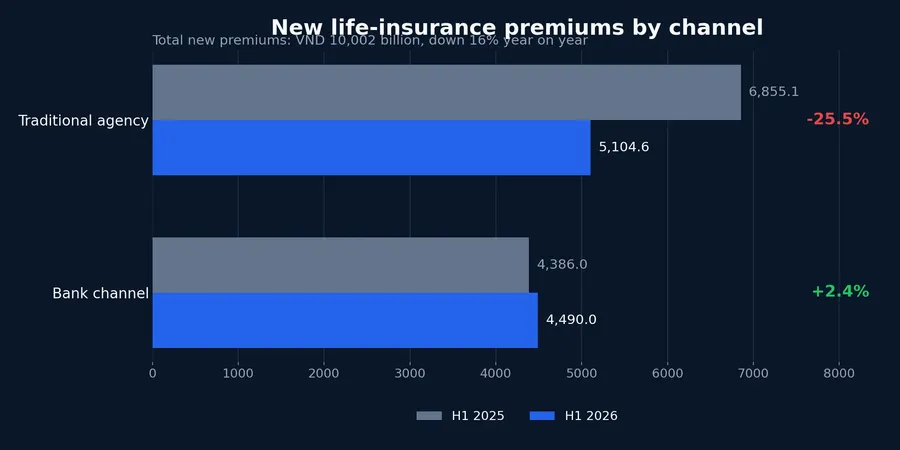

During a restructuring of sales channels, new business can decline before the quality of the market improves. New life-insurance premiums were about VND 10,002 billion in the first half, down 16% from a year earlier.Báo Đầu tư Chứng khoán That metric covers newly signed policies, not total life premiums, which also include recurring payments from existing policies. A 16% decline in new business can therefore coexist with a 4.5% decline in total premiums.

The channel mix makes the shift visible. New premiums through traditional agents fell from VND 6,855.1 billion to VND 5,104.6 billion, a 25.5% decline. The bank channel rose from VND 4,386 billion to VND 4,490 billion, or 2.4%.Báo Đầu tư Chứng khoán Bank distribution improved, but it did not offset the much steeper drop among agents. The evidence does not show demand disappearing altogether; it shows the market changing how it creates new contracts.

Premium growth is not profit growth

This is the distinction newer investors most often miss with insurance shares. A premium received today is not immediately available as profit. The insurer must still provide for unfinished coverage, reported losses, and claims that may emerge later. Premium growth becomes meaningful only when policies are priced appropriately and the cost of serving them stays under control.

Start with the claims ratio: it shows how much of earned premium is used to pay losses. An insurer may grow quickly by writing more business or accepting looser terms, but higher claims later can thin the profit left behind. The ratio must be compared within a similar business mix because motor, health, property, and marine insurance do not carry the same risks.

That comparison also needs a time dimension. A period with unusually low claims can make underwriting look stronger than it will be over a full year, while a large loss event can temporarily push the ratio in the other direction. The useful question is not whether one quarter looks neat in isolation. It is whether the company is writing enough premium for the risks it is accepting, and whether the pattern of claims fits the mix of policies it sells. For a newer investor, this is often more informative than ranking insurers by premium growth alone.

Then consider acquisition and administrative costs. A sales channel that creates premiums quickly but requires high commissions, large promotions, or heavy after-sales support may not produce matching margins. The apparent advantage of bank distribution is therefore a constructive hypothesis, not a conclusion; costs, persistency, and the quality of advice still need to validate it.

Reserving deserves a second look. Releasing reserves can lift current-period profit without a commensurate improvement in new underwriting. Building reserves because loss estimates have become more conservative can reduce short-term profit while creating a better buffer for future obligations. A single earnings number cannot tell investors which of those situations is at work.

The same principle applies to life insurance, where the renewal base matters as much as the sale of new policies. Existing contracts can keep paying premiums and cushion the top line, but their economic value depends on customers retaining the policies and on the cost of servicing promised benefits. A recovery in new premiums would be more persuasive if it comes with evidence that policyholders understand the product and remain with it, rather than with a short-lived push in sales activity.

Investment income is the final layer. Insurers receive premiums before paying benefits, so they temporarily invest the funds in deposits, bonds, and financial assets. Investment returns can support profit even when underwriting is not improving. When financial statements arrive, recurring interest from deposits and bonds should be separated from asset revaluations and one-off gains.

The share prices are already differentiated

The July 13 session showed that the market is not treating every insurance share as the same story. PGI closed at VND 18,150, up 6.76%; MIG was unchanged at VND 17,750; BIC slipped 0.88% to VND 22,650; and BVH fell 2.54% to VND 57,500. One trading session cannot establish a long-term valuation, especially when liquidity differs by ticker. It does reinforce the discipline of not extending non-life premium growth into an identical outlook for the whole group.

The conclusion is not that non-life insurance is automatically more attractive than life insurance. Current evidence only shows premiums heading in different directions; the earnings retained for shareholders still require confirmation in half-year reports. Claims ratios, acquisition costs, reserve movements, policy persistency, and the share of investment income are the signals worth following. Only alongside premium growth will they make each company's picture clear.