More than 4.21 million DIG shares were sold under forced-sale procedures between 7 and 9 July. That is not a detail to casually relabel as “management selling.” These shares were sold to recover debt after collateral conditions weakened, which is a very different proposition from an insider freely deciding to cut an investment.

For newer investors, the useful conclusion is straightforward. Forced selling can create compulsory supply, and that supply can prolong price pressure when buying interest cannot absorb it. Yet a forced-sale disclosure does not prove that an insider voluntarily lost confidence in the company, nor does it establish that forced sales explain every movement in DIG's share price.

A compulsory transaction, not an investment decision

Nguyễn Hùng Cường, Chairman of the Board of Directors of Development Investment Construction Joint Stock Corporation (DIC Corp, DIG), had 2,696,000 DIG shares force-sold between 7 and 9 July. His ownership fell from 5.43% to 5.09% of charter capital. In the same round, Lê Thị Hà Thành, a shareholder and related person of an insider at DIC Corp, had 854,000 shares sold; Nguyễn Thị Thanh Huyền, Vice Chairwoman of the Board of Directors of DIC Corp, had 660,400 shares sold on 7 July.Đầu tư Chứng khoán

Together, the round amounted to 4,210,400 shares. Including disclosed rounds on 25 May, 1 June and 9 June, forced sales since late May totalled 9,681,000 shares, or approximately 1.22% of DIG's charter capital.Đầu tư Chứng khoán That scale merits close attention to further disclosures, but it is not evidence that everyone named in the notices voluntarily changed their view of the business.

Think of the distinction this way. A voluntary sale is like an owner choosing to list a home. A forced sale occurs when that asset has been pledged against a loan and the lender is entitled, under the agreement, to liquidate it. Both result in shares reaching the market; they do not convey the same information about the holder's decision.

How a margin feedback loop works

With margin lending, an investor buys securities with a mix of personal capital and funds borrowed from a brokerage. The securities in the account become collateral. When the price falls, collateral value falls with it, while the loan balance and accrued interest do not automatically decline.

If an account's safety ratio drops below the maintenance level in its agreement, the brokerage may ask the customer to add cash or eligible collateral. The customer can also reduce the outstanding loan. If those remedies are not completed in time, the brokerage may sell the collateral to restore the account to the required level.

The risk is a two-way feedback effect. A falling price reduces collateral value. Shares sold to settle an obligation can add to market supply; if demand cannot absorb that supply, the price can remain under pressure. A lower price can then push other leveraged accounts holding the same stock closer to their own collateral requirement. This is a conditional mechanism, not a label that can be applied to every sell-off.

The word “can” matters here. Each brokerage has its own lending ratios, eligible-collateral list and liquidation timetable, while customers can add funds or repay debt. DIG's price is also affected by company news, the broader market and transactions by investors who use no margin at all. A down session alone cannot establish that all selling was forced.

What the numbers show, and what they do not

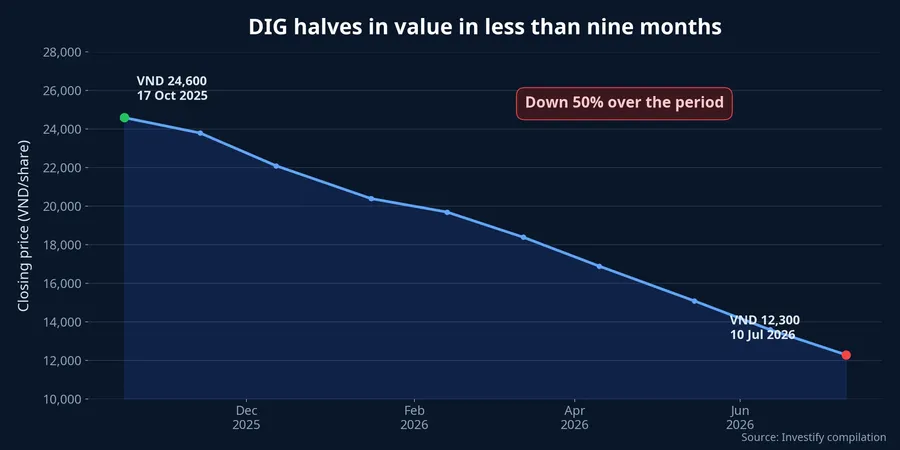

DIG closed at VND 12,300 on 10 July, 50% below VND 24,600 on 17 October 2025. Between 25 May and 10 July alone, the share price fell from VND 13,600 to VND 12,300, a decline of 9.56%. Those prices describe why collateral values became more sensitive; they do not establish that the disclosed compulsory sales caused the price move.

Of the four disclosed rounds, the 7 to 9 July period was the largest at 4,210,400 shares. The rounds on 25 May, 1 June and 9 June involved 1,787,000, 1,825,000 and 1,858,600 shares, respectively.Đầu tư Chứng khoán The series shows that compulsory supply has appeared more than once, rather than treating the 7 to 9 July event as an isolated trade.

Trading volume is supporting evidence, not proof of who sold. DIG matched 10,734,500 shares on 8 July, followed by 2,737,100 on 9 July and 4,368,200 on 10 July. Heavy turnover shows that more shares changed hands, but the trading screen cannot identify sellers and buyers or determine how many shares were collateral liquidations. Transaction disclosures are more reliable evidence for identifying the forced-sale component.

Read the disclosures in the right order

First, separate “expected” from “completed.” On 7 July, an MBS disclosure stated that it expected to force-sell 1,770,000 shares in total: 1,178,800 shares held by Mr Cường and 591,200 held by Ms Huyền. The sale would continue only until payment obligations were met or the account's collateral ratio returned to MBS's required level.Đầu tư Chứng khoán

An expected-sale notice is an alert about possible supply, not a final tally. The subsequent report for 7 to 9 July showed that 2,696,000 shares belonging to Mr Cường were actually sold, above the amount in the earlier MBS notice.Đầu tư Chứng khoán The difference is a reminder that one broker's notice may not cover all accounts, lenders or transactions that follow.

Second, pay attention to the verb. A registered sale describes an intention during a specified period. An expected forced sale says a brokerage has identified the possibility of collateral liquidation. A completed forced sale confirms that shares were actually sold under that process. Those phrases are not interchangeable, even when they are attached to the same insider's name.

Third, use the ownership ratio after the transaction to measure what has already changed. It cannot prove that selling pressure has ended. Sales may stop if obligations are repaid or collateral is added; if prices continue to decline, another disclosure may follow. A single rebound session therefore cannot establish that the feedback loop is over.

Conclusion: put evidence ahead of inference

This is not a price call on DIG. The available data confirm substantial compulsory supply across several rounds, and the margin mechanism explains why such pressure can reinforce itself under certain conditions. The evidence is not sufficient to assign a precise share of DIG's price move to forced selling, to separate it from the broader market, or to turn the transactions into a statement about management confidence.

For the next disclosures, the practical sequence is: a brokerage notice for shares that may be liquidated, a results report for shares actually sold, and the post-transaction ownership ratio. Only then should investors use volume and price reaction to judge how the market is absorbing supply. The question worth monitoring is not what sellers are assumed to think, but whether new reports continue to record compulsory supply.