Vietnam lowered domestic gasoline prices from 3:00 p.m. on July 9, while Brent still closed July 10 above USD 76 per barrel. At first glance, that looks like a contradiction. For new investors, though, it is a useful lesson in how the same energy story can travel through different clocks before it reaches households, logistics firms, and listed companies.Thanh Niên

The short version is simple. Vietnam's retail fuel prices do not move in lockstep with each Brent candle. They are built on the average price of refined products between two pricing windows, plus exchange rates, import-related costs, taxes, and regulated cost items inside the base-price formula. That means a sharp late-week jump in Brent can matter a great deal for global commodity sentiment and still fail to change domestic pump prices immediately.Nhân Dân

What the market sees is not what the pricing window reads

Under Decree 80/2023/NĐ-CP, Vietnam shortened the fuel-pricing cycle from 10 days to 7 days and moved it to every Thursday. More importantly, the world-price input in the base-price formula is calculated as an average across the days with quoted prices between two pricing announcements. It is not anchored to one closing print.Nhân Dân

That is where many readers go wrong. When Brent runs from the low-USD 71 area to above USD 76 in a handful of sessions, the instinct is to assume Vietnam's pump prices must move higher right away. But the domestic mechanism does not respond to the emotion of a single late-week rally. It responds to the average level across the full pricing window, which is a much wider frame than what investors see on an international futures screen.

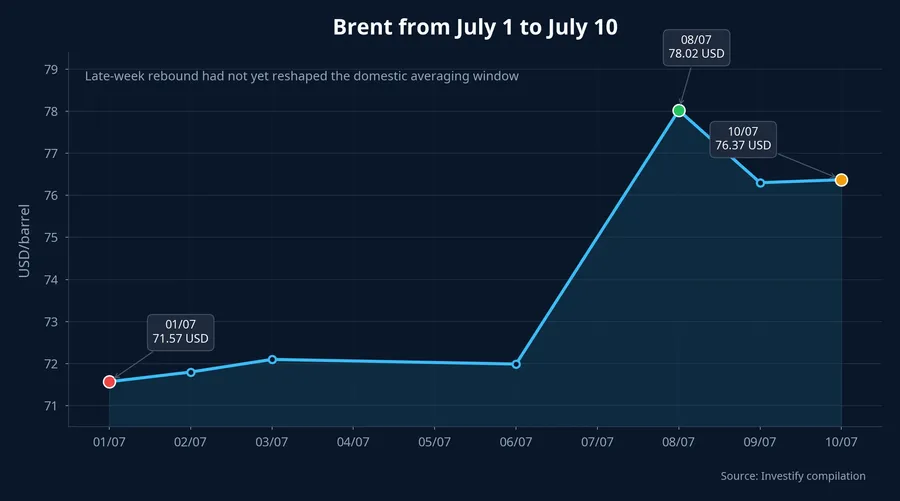

The early-July sequence makes that point clearly. Brent stood at USD 71.57 per barrel on July 1, edged up to USD 71.80 on July 2 and USD 72.10 on July 3, then sat at USD 71.99 on July 6. Only on July 8 did it jump to USD 78.02, before easing back to USD 76.30 on July 9 and USD 76.37 on July 10. That move was strong enough to change sentiment, but it had not lasted long enough to erase the lower prices that dominated the earlier part of the window.

That leads to the core thesis of this post. Vietnam's July 9 retail fuel cut did not disprove the rise in Brent. It showed that the domestic mechanism carries a built-in lag, and investors will misread the picture if they use one international oil session to infer an immediate impact on Vietnamese consumers.

The July 9 adjustment already split gasoline and diesel into two stories

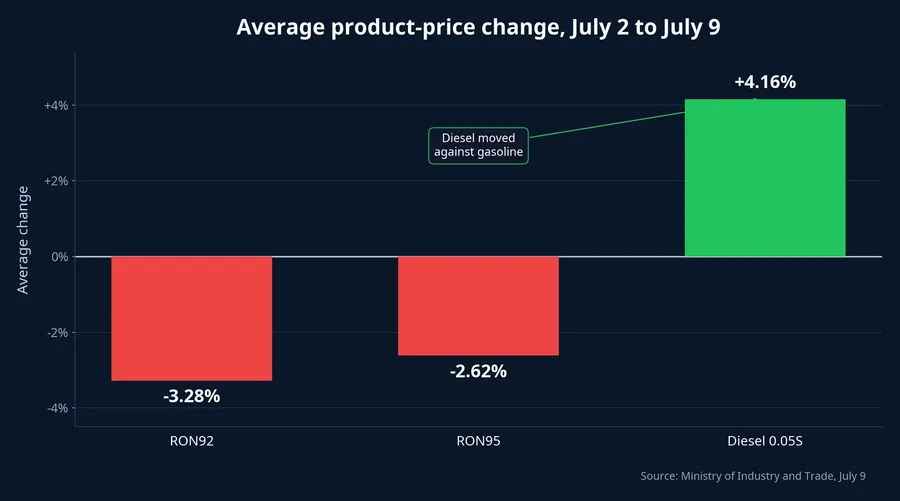

The July 9 adjustment made that divergence visible at the product level. The average price of RON92, which feeds E5RON92, fell 3.28% between the July 2 and July 9 windows. RON95, used for E10RON95-III, fell 2.62%. Diesel 0.05S, by contrast, rose 4.16% over the same period.Thanh Niên

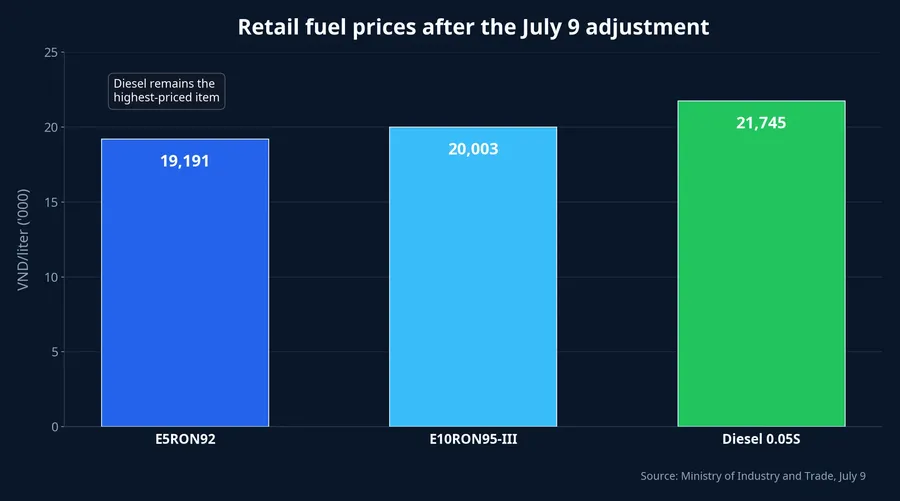

That is why the retail outcome did not move in one direction across all fuels. E5RON92 fell to VND 19,191 per liter, E10RON95-III fell to VND 20,003, while diesel 0.05S climbed to VND 21,745.Thanh Niên The lesson for investors is that even inside the same broad "fuel" bucket, each product still follows its own refined-product basket.

For first-time investors, that may be the single most useful takeaway. If you only watch Brent and conclude that the entire fuel bill of the economy is rising or falling in a straight line, you are skipping the more important layer of information: which refined product is pulling the pricing average higher, and which part of the market is exposed to that product.

Why Brent is a poor substitute for every fuel cost in the economy

Brent is a crude benchmark. Vietnam's retail formula is built on refined products. That difference creates the lag, but it also creates dispersion across industries. In plain language, the same move in oil prices can support the revenue outlook for upstream or oil-services names while leaving distributors to deal with inventory effects, working-capital needs, and regulated margins.

The same logic applies to transportation. Households naturally focus on gasoline because that is what they see at the pump for motorbikes and passenger cars. But for logistics and freight operators, diesel matters more. The July 9 adjustment is the cleanest example possible: gasoline fell, yet diesel rose. Anyone reading only the gasoline part of the story could conclude that transport costs were easing, even though a large share of corporate fuel demand was still under pressure.

That is where the investment reading becomes more nuanced. A consumer-facing retailer may benefit if household travel costs fall on a sustained basis. A freight operator or distributor may not get the same relief from a modest cut in E5RON92 if the main fuel inside its cost structure is still diesel.

Inflation also moves through a lag, not through one oil session

Vietnam's macro backdrop remained broadly stable in the first half, and June CPI fell 0.39% from the prior month while average six-month inflation rose 4.38% year over year. That is enough to show that fuel remains a meaningful input into the broader price level.Báo Chính phủ

But the timing still matters. June CPI reflects pricing windows that had already passed. It does not yet capture the full effect of Brent's rebound in the second week of July. If Brent stays elevated for several more sessions and the move feeds through to the average prices of RON92, RON95, and diesel in the next window, the inflation signal for the following month becomes more convincing. If the rebound fades quickly, the CPI effect will be much softer than the headline noise around global oil might suggest.

So the big picture is not "oil up, inflation up immediately." The better framing is that global oil influences Vietnam through several transmission layers, and the most important layer for retail prices is the average refined-product basket between two domestic pricing windows. Investors who ignore that layer tend to react too quickly to a global move that has not yet completed its trip through the local system.

Reading the timing correctly matters for related stocks

In oil rallies, the market often swings between two extremes. One is to throw every oil-linked stock into the same bullish basket. The other is to see a domestic gasoline cut and assume the energy story has cooled. Both readings are too blunt.

A more practical approach is to separate three signals. The first is global crude, which reflects geopolitics and supply risk. The second is refined-product pricing inside the domestic window, which tells you whether that shock has actually entered the base-price formula. The third is the retail price paid in Vietnam, where households and companies start to feel the impact in cash terms.

When those three layers are out of sync, investment conclusions should not run too far ahead. Brent holding above USD 76 per barrel is a signal worth watching for crude-linked names. But to claim that Vietnam's retail fuel costs have already shifted to a new floor, investors still need evidence that the next pricing window has been pulled up by a higher average. Without that link, "pump prices must rise immediately" is still a step too far.

The most important signal for next week

If I had to pick one thing to watch next week, it would not be whether Brent finishes one session green or red. It would be the average level of RON92, RON95, and diesel inside the new pricing window. That is what will decide whether the recent rebound in global oil is strong enough to feed into Vietnam's retail prices or whether it remains a short-lived tremor in the international market.

That is why the conclusion here is fairly direct. Vietnam's July 9 fuel-price cut and Brent's late-week rise do not cancel each other out. They simply describe two different measurement rhythms within the same energy chain. For investors, reading that timing correctly matters far more than reacting quickly to a single international oil move, because the lag is what ultimately determines the real effect on inflation, corporate costs, and the listed sectors tied to fuel.