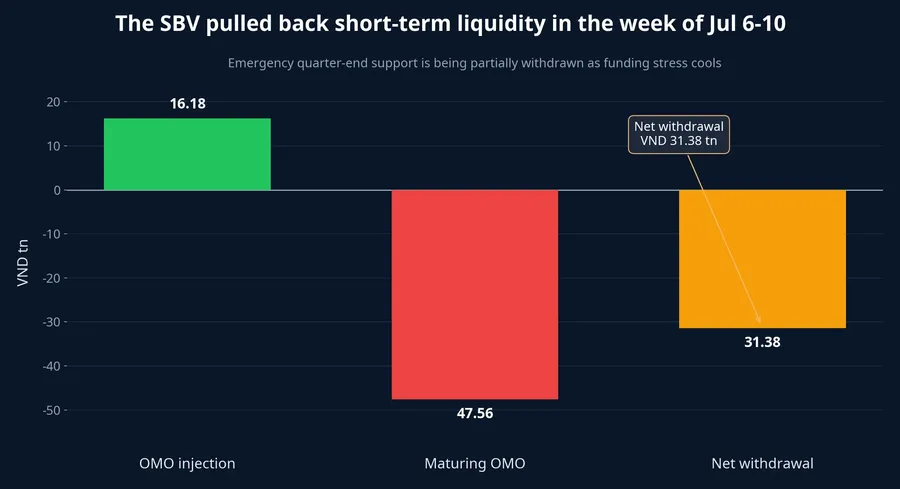

The most important signal at the end of this week is not tied to a single stock. It sits in the plumbing of the banking system. In the week of July 6-10, the State Bank of Vietnam withdrew a net VND 31,379.6 billion through open-market operations, while the central exchange rate rose another VND 8 to VND 25,214 per dollar, marking its eighth straight weekly increase.TBTCVN For newer investors, that combination easily sounds like a simple tightening story.

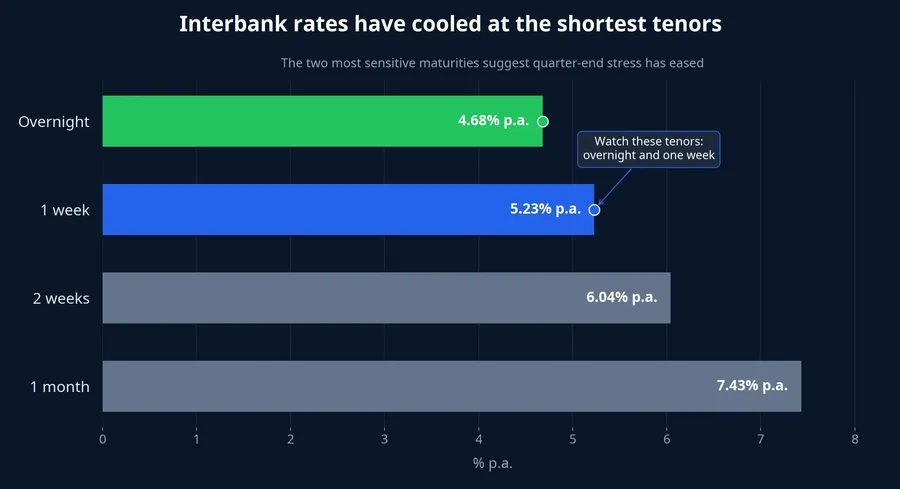

That reading is too blunt. During the same week, overnight VND interbank rates fell to 4.68% per year, while one-week funding costs eased to 5.23% per year.TBTCVN In plain English, the SBV is pulling back part of the short-term support it had already injected, but the latest data do not yet describe a broad-based liquidity squeeze across the system.

A net withdrawal does not automatically mean money is scarce

For retail readers, open-market operations can sound abstract. The cleaner way to think about them is as the SBV's short-term control panel for system liquidity. When funding stress appears, cash goes out. When the stress fades, some of that cash comes back. The key is not the headline verb, but the rate reaction that follows.

Last week, the SBV injected VND 16,181.55 billion through OMO, while VND 47,561.15 billion matured. That gap created the net withdrawal of VND 31,379.6 billion.TBTCVN If this were a genuine tightening shock, you would normally expect short-term interbank rates to jump and stay elevated. Instead, overnight and one-week rates both moved lower. That matters more than the headline phrase "net withdrawal."

This distinction matters for how investors frame the coming week. When interbank rates cool even as the central bank withdraws liquidity, the more defensible interpretation is that policymakers are rebalancing short-term money conditions rather than choking the system. Those are very different messages. One is about rhythm management; the other would imply a real shift in monetary stance.

The exchange rate is the reason VND funding costs may stay sticky

If OMO data say liquidity is not critically tight, why should investors still be cautious? Because the exchange rate is telling a different part of the story. The central rate has now risen for eight consecutive weeks, and with a 5% trading band, commercial banks are allowed to quote USD in a range of VND 23,953.3 to VND 26,474.7 per dollar.TBTCVN Internal market data for July 10 place USD/VND at VND 26,285.5, still close to the top end of that corridor. DXY stood at 100.64 on the same day.

That matters because it suggests the authorities still need to pay attention to FX pressure even as short-term liquidity gets easier. In that kind of setting, the cost of holding VND may stop getting hotter without becoming truly cheap. Rates can cool, but they are less likely to fall sharply if policymakers are still defending the currency backdrop.

This is also where investors should avoid forcing a single-cause narrative. A shaky week for the VN-Index does not prove that FX pressure is the only driver. Market breadth, foreign flows, and stock-specific news still matter. Still, when the official exchange rate rises week after week, short-term rates are less free to drop quickly. That means risky assets must compete against a higher alternative yield floor.

Why deposits remain a serious competitor to equities

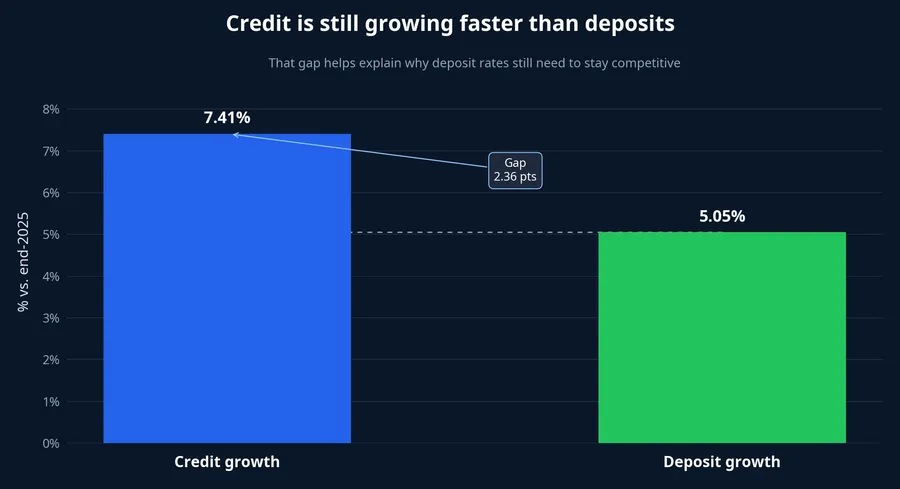

Another useful clue is the gap between credit growth and deposit growth. According to figures cited by Thời báo Tài chính Việt Nam, credit expanded 7.41% in the first half of the year, while deposit growth reached 5.05%. After the first five months, deposit growth had been only 2.98%.TBTCVN Deposits are improving, but they are still not catching up with the pace of credit demand.

That gap helps explain why deposit rates cannot fall too quickly. Banks still need to keep idle cash interested, especially while FX conditions remain sensitive. A July 9 survey by VietnamNet showed that four banks were offering online six-month deposit rates of at least 7% per year: ACB at 7.1%, Bac A Bank at 7.05% for deposits from VND 1 billion, and MBV and VCBNeo at 7%.VietnamNet

That is not an argument to abandon equities and pile into savings. The more useful takeaway is that idle cash has a respectable home base again. When six-month deposits already pay around 7% and stocks remain volatile, retail investors naturally demand a higher compensation for taking equity risk. That mechanism alone can slow speculative flows, even without a dramatic tightening shock.

Read the week ahead through three signals, not one headline

For the coming week, investors do not need a heroic forecast. They need a short watch list. The first signal is the path of overnight and one-week interbank rates. If both tenors keep easing or at least stay flat, the market can reasonably conclude that the quarter-end funding squeeze has passed. That would lighten the monetary pressure on equities.

The second signal is where banks keep quoting their USD selling rates relative to the top of the permitted band. If those quotes remain clustered near the ceiling, the issue is not simply liquidity scarcity. It is continued demand for FX protection. In that scenario, rates are less likely to fall deeply, and risky assets are less likely to enjoy the full benefit of calmer liquidity conditions.

The third signal is whether aggressive deposit offers spread further across the banking system. If more banks cluster around 7% for six-month money, the competition for household cash is still very much alive. That does not make equities immediately unattractive, but it does raise the hurdle rate for taking market risk.

It is also worth separating correlation from causation. The VN-Index closed July 10 at 1,828.34, down 12.36 points on the day and roughly 33.74 points below the prior weekend. That still does not prove FX pressure single-handedly weakened the market. The more disciplined reading is narrower: when the exchange rate stays sensitive and deposit rates remain competitive, equities cannot be priced as if money were cheap again.

Start with money, then move to prices

The core thesis is straightforward. The week of July 6-10 did not yet point to a system-wide tightening shock, because the shortest interbank rates cooled even while the SBV withdrew liquidity on a net basis. But the eight-week climb in the central exchange rate suggests the cost of holding VND is not ready to fall fast enough for the equity market to relax completely.

That is why the next week should be read through money first and prices second. If overnight and one-week rates stay stable and bank USD quotes move away from the top of the band, pressure on risky assets can ease. If not, and if deposit rates keep inching higher, stocks will still be forced to compete with a more attractive safe alternative. That is the real question for the next few sessions: is the system genuinely getting cheaper to fund, or is it merely becoming less strained while the FX problem remains in place.