For many Vietnamese households, a larger real-estate stack still feels like the clearest sign of financial strength. The logic is familiar: property is tangible, long-lived, and easier to trust emotionally than a line on a brokerage app. It can preserve wealth over time, signal status, and serve as something that can be passed down across generations.

That instinct is not wrong. But fresh data from TVS's 2026 Financial Health and Investment Confidence survey suggest investors need to separate two different questions. One is whether an asset can hold value over the long run. The other is whether it can be turned back into cash on a timetable the owner actually controls. Real estate often scores well on the first test and much worse on the second.

What the data say about Vietnamese portfolios

TVS surveyed 1,000 people in five major cities who held at least VND 500 million in savings. The pattern was straightforward: the higher the income bracket, the larger the real-estate share of the portfolio. Property accounted for 31% of portfolios in the under-VND-500-million group, 37% in the VND 500 million to VND 1 billion group, and 44% in the above-VND-1-billion group.DNPL

In plain terms, rising income in Vietnam often means a larger share of family wealth gets parked in a big, indivisible, slow-moving asset class. That is not a surprise. Property has long occupied a special place in Vietnamese household finance, not just as an investment, but as a store of stability. So the real story is not that affluent investors like real estate. The real story is what they may be giving up in exchange for that comfort.

As income rises, the cash and bank-deposit share falls from 42% to 29%, while gold drops from 16% to 10%. Stocks, mutual fund certificates, and private business capital still remain below 10%.DNPL That means additional wealth is not flowing in a major way into more flexible financial assets. It is being concentrated primarily in housing and land, which is exactly where the portfolio-liquidity mismatch begins.

TVS also found that 70% of respondents already owned real estate. On average, property made up 36% of personal assets, while bank deposits, real estate, and gold together accounted for 87% of total holdings.DNPL That is a portfolio structure tilted heavily toward preserving visible wealth, not maximizing flexibility. Wealth on paper and resilience in a cash squeeze are not the same thing.

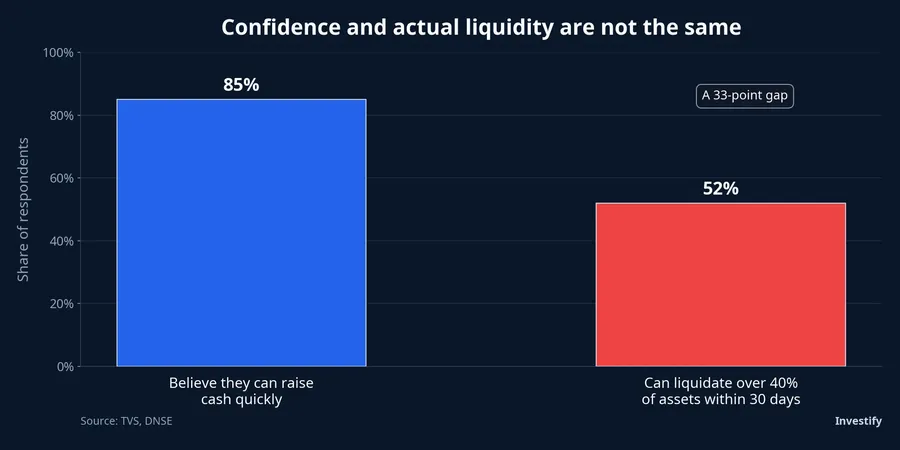

The weakness is not value, but conversion speed

The most striking number in the TVS survey is the gap between confidence and actual liquidity. While 85% of investors said they believed they could raise cash quickly if needed, only 52% said they could liquidate more than 40% of their assets within 30 days. DNSE, citing the same TVS data, highlighted that same disconnect.DNSE

This is where portfolio size can become misleading. A house may have a high market value, but turning it into cash within a month is a completely different exercise. A seller has to find the right buyer, complete legal paperwork, negotiate on price, and accept the market's terms at that exact moment. If the need for cash is urgent, the cost usually shows up not as an explicit fee, but as a weaker selling price or a much longer waiting period.

That is why real estate can be excellent at preserving wealth and still be weak at funding near-term needs. Those are two different functions. An investor can look very wealthy on a balance sheet and still become financially constrained if too much of that wealth sits inside hard-to-sell assets. So a high property share is not enough to prove a portfolio is healthy. The more relevant question is how much of total wealth can be converted into cash without a severe price concession.

2026 market conditions are stress-testing that assumption

The first half of 2026 has made the liquidity issue easier to see. Vietstock, citing OneHousing, said absorption rates at primary-market projects in the first half of the year were only about 50-60%, well below the above-80% level seen in the same period of 2025.Vietstock That does not mean money has abandoned real estate altogether. It means buyers have become more selective, and assets now need to clear a higher bar to sell quickly.

In Ho Chi Minh City and nearby areas, DKRA Consulting data cited by Tạp chí Kinh tế Tài chính showed land-lot projects absorbing only about 4% of total supply. Townhouses and villas posted absorption of roughly 9%, down 71% from the second quarter of 2025. Primary apartment demand fell 11% year over year, while secondary-market apartment prices were broadly down 2-6% from the prior quarter, especially among owners facing financial pressure.KTTC The important takeaway is not collapse. It is a widening difference between high-quality inventory and assets that need a quick exit.

CafeF, citing CBRE Vietnam's second-quarter report, said Ho Chi Minh City saw 6,573 newly launched apartments and 1,934 newly launched landed units over the past three months, up 20% from a year earlier. Average primary prices reached about VND 76 million per square meter, up 8% quarter over quarter and 16% year over year. Marketwide absorption was still 90%, but new-supply absorption was only 73%.CafeF In other words, the market is still functioning, but it no longer offers easy turnover at yesterday's profit expectations.

Hanoi shows the same tension in a different form. VTV, citing CBRE, reported that apartment supply launched in the first six months reached 16,600 units, the highest first-half level since 2020. But the market has now gone two straight quarters without a new project priced below VND 60 million per square meter. Mid-year average primary prices stood at VND 95 million per square meter, up 12% quarter over quarter and 21% year over year. Sell-through at launch events fell to below 70%, versus 90-95% in 2024-2025, while transactions in landed property fell 74% from a year earlier.VTV

These numbers do not prove real estate is suddenly a weak asset class. What they do show is that liquidity is no longer evenly distributed across the market. Buyers with real cash still exist, but they are pricing legal clarity, location, project quality, and yield prospects much more carefully. In that environment, a portfolio that leans too heavily on property becomes vulnerable whenever the owner's timing and the market's timing stop lining up.

A durable portfolio needs a liquidity layer

The practical lesson is not to turn against real estate. That would be too simplistic for Vietnam, where property remains a core household asset. The more useful distinction is between a core asset layer and a liquidity layer. The core layer protects long-term value. The liquidity layer handles near-term cash needs without forcing the owner to dump the largest asset in the portfolio at the wrong time.

That liquidity layer can include cash, bank deposits, open-end fund certificates, government bonds, or other instruments with a clearer path back to cash. They may not produce the same emotional sense of wealth as owning property, but they are what keep a portfolio usable under stress. For newer investors, this is the key reframing: financial safety is not only about how much you own. It is also about how much of it can actually be used when time matters.

That leads to a clean thesis. Real estate still deserves a central place in Vietnamese portfolios, but a high property weighting only translates into resilience when it is paired with a sufficiently large liquidity buffer. Without that second layer, a portfolio can look powerful in calm periods and become unexpectedly rigid the moment cash turns into the priority. The signals worth watching next are primary-market absorption, secondary-market pricing pressure, and the cash-flow health of asset owners themselves. Those will tell investors whether property remains a stable anchor or becomes the part of the portfolio that is hardest to mobilize.