VND 1 million in a one-year savings deposit may earn a few tens of thousands of dong. The same VND 1 million, if it becomes an interest-bearing credit-card balance, can generate a cost many times larger. Looking at those two percentages side by side can make the difference feel hard to justify.

The simpler way to see it is this: a deposit is money you let a bank use for an agreed term, while a credit card is money the bank advances for you to spend. Comparing their rates without their terms is like comparing a car-rental fee with a parking fee: both concern a car, but the payer, the risk, and the service are different. This article’s central point is not that one rate is inherently “expensive” or “cheap”; it is that understanding the terms prevents a short-term purchase from becoming a long-running balance.

The 48% rate applies to selected cards, not every cardholder

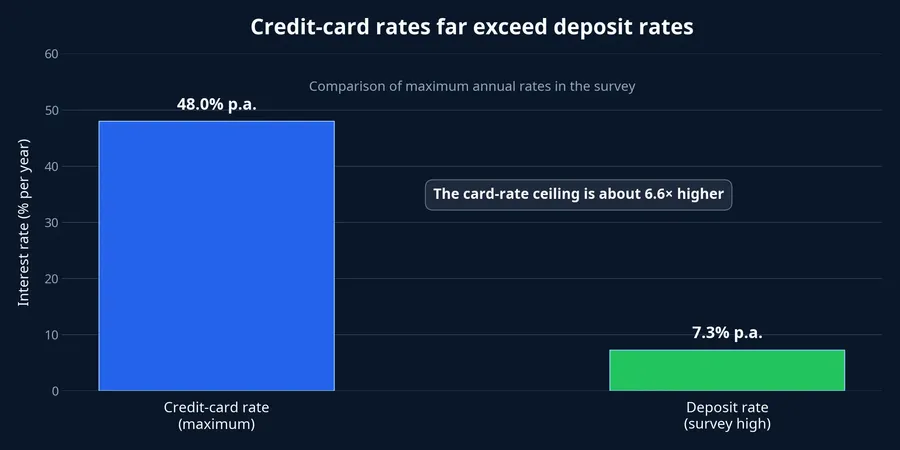

From July 16, 2026, ACB’s in-term interest rates for personal credit cards range from 20% to 48% a year. The 48% maximum applies to selected cards issued before October 10, 2025: ACB Visa Platinum, ACB MasterCard Gold, ACB Visa Digi, ACB JCB Gold, and ACB Visa Gold. The ceiling is 13 percentage points above the prior schedule, but it should not be treated as the standard rate for every ACB customer or card product.Znews

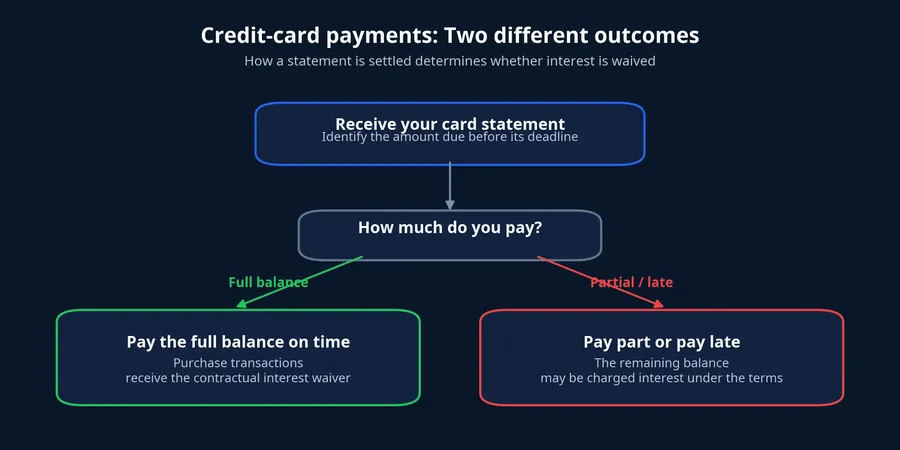

More importantly, interest does not appear automatically when a card is used for a purchase. Under ACB’s terms, purchase transactions are interest-free when the cardholder pays the full statement balance by the payment due date. Interest is charged when the user makes only a partial payment, does not pay, or pays late, and it accrues daily on the interest-bearing balance.ACB

That makes the 48% figure a prompt to read a statement closely, not a shortcut for estimating the cost of every card purchase. Even on the same card, the actual cost depends on the outstanding balance, transaction-posting date, repayments, and applicable terms. A revolving credit line carries a higher rate than a deposit because the bank advances unsecured funds for individual purchases and bears the risk of late or non-payment.

A deposit rate pays for stability and a fixed term

On the other side, a July 5 survey of online deposit rates found a high of 7.3% a year for a 12-month term, while most banks in the survey quoted 6.6% to 6.9%. That is a snapshot at the time of the survey, not a promise available to every deposit. The return can vary with the bank, deposit size, tenor, channel, and customer conditions.CafeF

With a term deposit, the customer provides the money first and agrees to leave it for the selected term in exchange for interest. An early withdrawal can sharply reduce the return; ACB’s general terms state that early withdrawals receive the lowest demand-deposit rate. So the useful number is not the highest headline rate in a survey, but the rate shown for your own amount, tenor, and channel.ACB

Seen together, the gap is less mysterious. Deposits give a bank a relatively stable funding source for a defined period. Credit-card balances allow customers to spend first and repay later, with daily changes in use and repayment; their rate therefore reflects funding, payments infrastructure, operating costs, loss provisions, and the flexibility of the revolving line.

One million dong over a year is only an illustration

Using 7.3% a year for illustration, VND 1 million placed for a full 12 months and paid at maturity would earn approximately VND 73,000. That is simply principal multiplied by an annual rate, assuming the deposit stays in place to maturity. It is not a guaranteed return for every deposit, because 7.3% was the highest rate in the July 5 survey.CafeF

For the card example, assume VND 1 million has become an interest-bearing balance, remains unchanged for a year, and is charged at 48% a year. The corresponding interest would be approximately VND 480,000. This illustration excludes fees, new spending, repayments, and day-to-day balance changes; it simply shows how a small balance kept open can cost far more than a deposit earns over the same period.ACB

The difference does not mean a bank takes one deposited dong, lends that precise dong through a card, and retains all of the spread. Banks also maintain liquidity, regulatory capital, and provisions for balances they may not recover. A more useful question is whether a quoted rate is merely a reference point or whether it will actually apply to the way you use the product.

A minimum payment does not preserve the interest waiver

This is where new card users often get caught out. The minimum payment is the lowest required amount shown on a statement; paying it may keep the account from immediately being short of the required minimum. It does not mean that the remaining balance is still interest-free.

For purchase transactions, the safer standard for preserving the contractual interest waiver is to pay the full statement balance on time. Cash withdrawals are different: ACB states that interest runs from the day the withdrawal is debited until it is repaid in full, in addition to a cash-withdrawal fee. The purchase grace-period rule should therefore not be applied automatically to every card transaction.ACB

When a statement arrives, separate four items: the statement balance, the minimum payment, the due date, and the rate for your particular card. If the goal is to avoid interest on purchases, the full statement balance matters more than the minimum amount. ACB also notes that payment is recognised when the bank receives the funds, while late transfers may be processed on the next business day.ACB

What to watch instead of one headline percentage

A credit card can be a convenient payment tool when the user controls the due date and clears the balance. A term deposit serves money that can be left untouched for an agreed period. They meet different needs, so the gap between their rates does not, by itself, establish that either product is better.

The practical takeaway is to check conditions before comparing the biggest numbers: which amount, term, and channel qualify for a deposit rate; and which card, timing, and situation trigger a card rate. The thesis remains straightforward: a card purchase becomes costly when its balance loses the interest waiver and is allowed to persist. For each statement cycle, the signals worth watching are the due date, the statement balance, and whether the bank has recognised the payment.