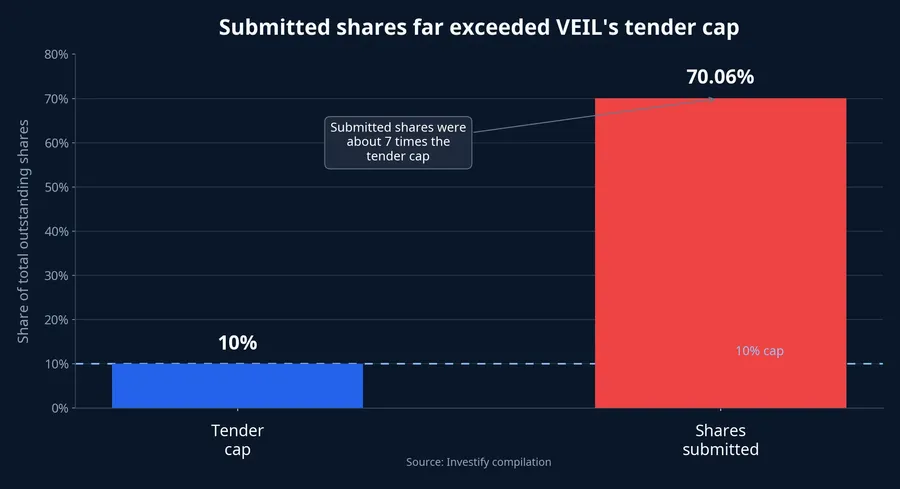

At midday on July 9, the VN-Index stood at 1,844.75, down 8.95 points. With the market already slightly in the red, news that investors had submitted 70.06% of VEIL's outstanding shares into a tender offer was always going to sound alarming, especially to newer investors.

But this is not, at least not yet, a story about foreign capital fleeing Vietnam's stock market as a whole. The more accurate framing is narrower: VEIL is only buying back up to 10% of its outstanding shares, so any market pressure depends on how the fund finds liquidity to pay exiting shareholders.Investegate

What actually happened

VEIL said on July 9 that shareholders submitted 96,290,939 shares into the offer, equal to 70.06% of outstanding shares excluding treasury stock. Of that amount, 72,995,315 shares elected cash, while 23,295,624 shares opted to receive a slice of the portfolio in specie instead.Investegate

That headline number matters, but only up to a point. The tender itself is capped at 10% of outstanding shares, and excess submissions above basic entitlements are only being accepted at an additional 1.69%. In plain English, a lot of investors want out, but the fund is not buying everything they offered to sell.Investegate

That distinction is where many retail readers can go wrong. A figure like 70.06% sounds like a direct signal that Vietnamese equities will be dumped into the market. It is not. Between the cap, the allocation rules, and the in-specie option, the transmission mechanism is much more complicated than a straight line from redemption demand to forced selling.

VEIL has also laid out a clear timetable. The purchase price will be based on adjusted NAV as of July 8, after a 2.5% discount. Cash settlement is expected on July 13, while the in-specie transfer for eligible shareholders is expected to complete before July 14.Investegate

The key question is where the cash comes from

For investors, the practical question is not why so many people wanted to submit shares. The more useful question is how much real cash VEIL needs to pay out, and how quickly it can raise that cash if the final accepted mix tilts heavily toward cash elections.

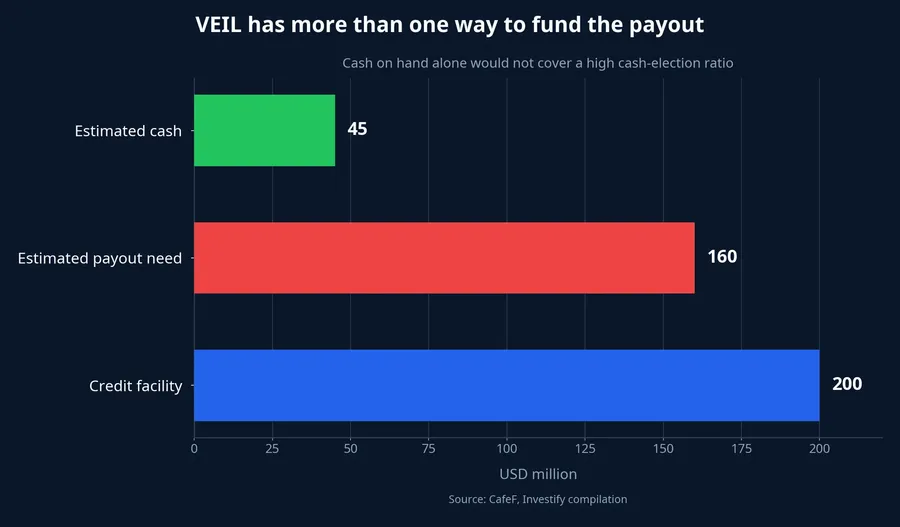

Dragon Capital's May report, published in July, showed VEIL was already close to fully invested, with cash at just 2.8% of net assets and NAV at USD 1,618.2 million. Based on the figures cited by CafeF, that implies around USD 45 million in cash on hand, versus an estimated USD 160 million needed for the buyback program.Dragon CapitalCafeF

That funding gap is exactly why the story should not be reduced to "redemptions mean immediate selling." CafeF also reported that VEIL had a USD 200 million credit facility and USD 50.3 million in debt at the end of May. That gives the fund several ways to bridge payouts before it has to lean aggressively on the underlying portfolio.CafeF

There are at least three liquidity channels worth watching. First comes cash already on hand, plus receivables from prior trades. Second comes short-term borrowing, which can buy time and reduce the need for rushed selling over a few sessions. Only after that do investors get to the third channel: selling part of the equity portfolio to restore the balance sheet.

That sequencing matters because it changes the risk assessment. If VEIL relies more on credit, near-term selling pressure could be softer even though leverage rises. If it chooses to sell part of the portfolio, pressure is unlikely to hit the market evenly. It would be more logical for the fund to monetize the largest, most liquid positions first.

Where selling pressure would likely show up first

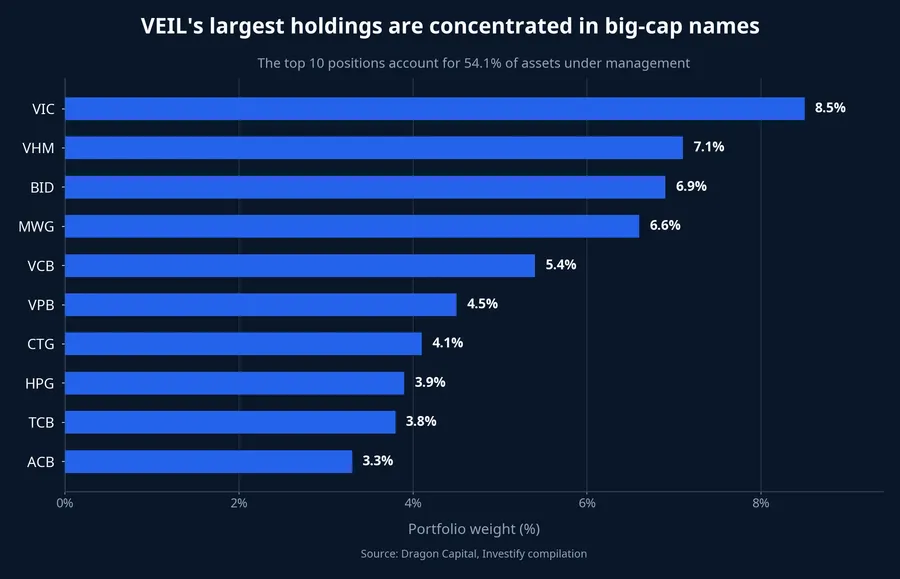

At the end of May, VEIL's top 10 holdings accounted for 54.1% of assets under management. The list included VIC at 8.5%, VHM at 7.1%, BID at 6.9%, MWG at 6.6%, VCB at 5.4%, VPB at 4.5%, CTG at 4.1%, HPG at 3.9%, TCB at 3.8%, and ACB at 3.3%.Dragon Capital

Those are exactly the kind of names the market would scrutinize first. They are large caps, liquid, and already widely held across institutional portfolios. If VEIL does need to turn assets into cash, the most plausible technical pressure would show up here rather than across the market at random. That is a portfolio-structure story, not a macro verdict on Vietnam.

The midday tape on July 9 still looked tentative rather than decisive. VHM was at VND 149,100, down 0.60%; BID was at VND 41,450, down 0.84%; MWG traded at VND 78,100, down 0.89%; and VCB was at VND 61,200, down 0.65%, while VIC still edged up 0.09% to VND 220,900. The numbers suggest investors are aware of the headline, but they do not prove that VEIL-related selling has already been fully priced in.

That caution matters. A mild down session in large caps can still reflect broader market sentiment, unrelated portfolio rebalancing, or simply incomplete midday price discovery. Saying these moves happened because of VEIL would go beyond what the tape actually proves today.

How retail investors should read this

The first layer is the fund itself. A very large share of holders wants liquidity, but the amount VEIL will actually buy back remains capped at 10%. So the 70.06% submission rate is a signal about stress inside a closed-end fund structure, not a one-for-one proxy for how much Vietnamese stock is about to be sold.Investegate

The second layer is liquidity. VEIL's cash buffer looks thin relative to estimated payout needs, but cash is not the fund's only lever. There is still credit, there is still the in-specie route, and there is still flexibility in how the fund stages transactions. Investors will get a much cleaner read once the final cash-election mix and funding choices become more visible.

The third layer is market impact. If pressure emerges, it is more likely to be concentrated in VEIL's large-cap holdings than to become proof that foreign investors are abandoning Vietnam across the board. Those are two very different claims. One is about a London-listed closed-end fund managing liquidity. The other would require much broader evidence from foreign flows, price action, and market breadth.

The most coherent conclusion for now is that technical pressure is real, but the correct scope is still VEIL and the fund's biggest holdings. That view only changes if the post-settlement period brings wider evidence such as sustained foreign selling across the market, clearly weaker liquidity in large caps, or repeated heavy-volume declines in the names where VEIL is most exposed. Until then, VEIL looks more like a test of portfolio structure and liquidity management than a verdict on Vietnam's entire equity market.