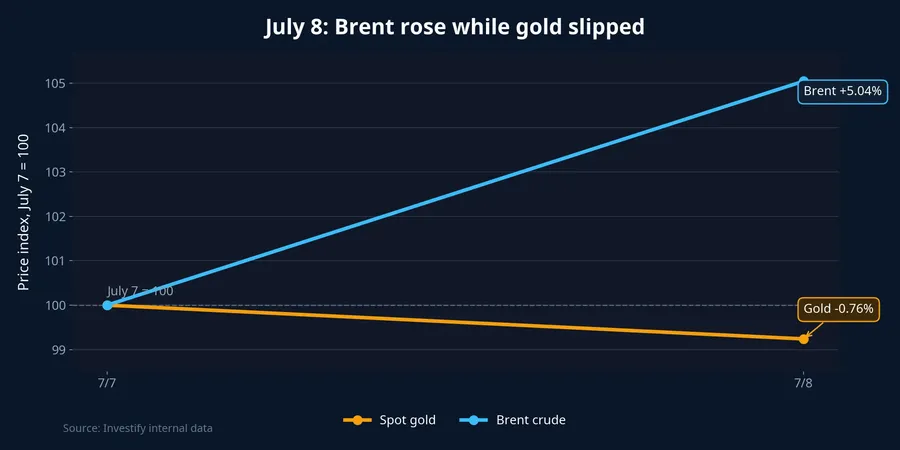

A common beginner reflex is to assume that any geopolitical flare-up must push gold higher. The US session on July 8 showed why that shortcut can fail. On the same day, Brent crude rose from USD 74.16 a barrel to USD 77.90, up 5.04%, while spot gold slipped from USD 4,105.70 an ounce to USD 4,074.50.

The simple version is this: oil responds directly to fears of supply disruption. Gold does not. Gold generates no cash flow on its own, so every decision to hold it is also a decision not to hold something else that may be safer, more liquid, or more rewarding in the moment.

That leads to the central argument of this piece. July 8 did not prove that gold has lost its safe-haven role. It showed that gold is a multi-variable haven. When the US dollar strengthens, the opportunity cost of owning gold rises, and Wall Street is not in full liquidation mode, geopolitical headlines alone may not be enough to push gold higher immediately.

Oil and gold react to different kinds of fear

The easiest mistake for new investors is to place oil and gold in the same box simply because both appear in geopolitical headlines. That is how people end up assuming that if Brent is up, gold should follow. In reality, the two assets climb for very different reasons.

Oil rises when traders fear that supply will be interrupted or that barrels will take longer and cost more to move. With Brent, the market can react fast as soon as Middle East tensions create concern about shipping routes or physical availability. Gold does not trade on that channel alone. It tends to respond more decisively when fear is strong enough to pull money out of risk assets and into a clearer defensive allocation.

Put differently, oil prices a supply shock. Gold prices how investors rank fear against the dollar, interest rates, and the rest of the risk landscape. If you look only at the phrase "escalating conflict," you collapse two separate stories into one. That is the first reading error.

The variable beginners most often miss is the dollar

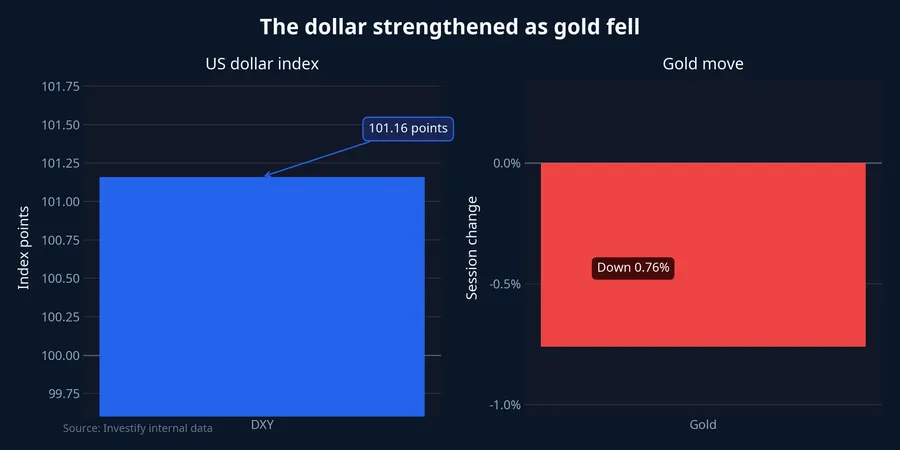

Gold is priced globally in US dollars. When the dollar strengthens, gold becomes more expensive for buyers using other currencies, and both physical and investment demand usually face more resistance. Investify's internal data shows the DXY dollar index at 101.16 on July 8, up 0.31% from the prior session.

A 0.31% move may not sound dramatic in isolation. But in a session when gold needed a strong defensive flow to overpower everything else, a firmer dollar was a meaningful headwind. In plain terms, if holding cash in dollars suddenly looks more attractive, global investors may not rush into gold on the first day of bad news.

The risk for beginners is to treat war as a one-way switch. Gold never trades that cleanly. One force comes from demand for protection. The other comes from dollar strength, the level of rates, and whether markets are actually panicking. When that second set of forces is stronger, gold can fall even as the news cycle turns darker.

That still does not justify an equally simplistic conclusion in the other direction. A stronger dollar does not always mean lower gold. What July 8 showed is that, in that time window, a firmer dollar explained gold's weakness better than the assumption that "more conflict must mean higher gold." The market was putting more weight on currency strength and holding costs than on a pure safe-haven reflex.

Wall Street did not flash full panic

Another important signal is that US equities did not move into a uniform liquidation pattern. On July 8, the Dow Jones Industrial Average fell 576.76 points, or 1.1%, the S&P 500 lost 0.3%, but the Nasdaq still managed to rise 0.2%.AP

The key takeaway is not simply that "US stocks fell." It is that money still split across sectors. In a cleaner panic regime, equities usually sell off together while investors run aggressively toward Treasuries, the dollar, and gold. That did not happen here. Nasdaq stayed green, which suggests capital had not fully abandoned risk assets.

That leaves at least two plausible explanations for gold's decline on July 8. One is that dollar strength reduced gold's short-term appeal. The other is that fear had not deepened enough to trigger a broad move into bullion. The available evidence supports a combination of both, not a single-cause story.

This is where investors should be suspicious of overly neat narratives. Markets love one-line explanations because they are easy to remember, but actual capital rotates across several signals at once. The more an asset is seen as a haven, the more carefully you need to read those layers before reaching a conclusion.

Vietnamese buyers also have to separate global gold from the SJC layer

If global gold is already hard to read, domestic gold in Vietnam is one step harder. Buyers of SJC bars are not just buying international gold moves. They are also paying for the structure of the local bullion market.

On the morning of July 9, Simplize showed SJC bullion at around VND 145.5 million to VND 148.53 million per tael, down VND 1.5 million on both the bid and offer from the previous day.Simplize That is enough to show that local prices do react to the global move. But they do not always match the same pace, the same magnitude, or the same timing.

Using Vietcombank's exchange rate at the end of July 8, VOV calculated the world gold price at about VND 130.15 million per tael, which was VND 19.35 million below SJC's end-of-day selling price.VOV That gap is the part many first-time buyers miss. They think they are buying an international safe-haven asset, but they are also paying a large domestic premium created by market structure.

That matters in two ways. If global gold falls, SJC may not fall by the same amount because the local premium is still embedded in the price. If global gold rebounds, SJC may also fail to rise in lockstep if the domestic spread is already stretched and sellers decide to compress margins instead of pushing headline prices further.

The practical framework is to split the question in two. First, what is driving world gold right now: the dollar, haven demand, or capital leaving equities. Second, how much extra is SJC adding above the converted global price, and is that spread widening or narrowing. Without separating those two layers, it is hard to know whether you are reacting to the international gold market or to a local pricing premium.

A more useful framework for the next bad-news session

The main lesson from July 8 is not that gold has stopped being a haven. The lesson is that gold does not respond in the simple way new investors expect. Geopolitical stress can be the spark, but it may not be the dominant force if the dollar is stronger, capital is still willing to stay with technology stocks, and markets have not shifted into broad defense mode.

A more disciplined reading order helps. Start by asking whether the shock is about physical supply or just sentiment. Then check whether the dollar is strengthening or cooling off. Next, look at whether US equities are selling off across the board or only splitting by sector. Finally, if you are buying in Vietnam, ask how far SJC is trading above the converted world price.

The conclusion that best fits the evidence is straightforward: in the short run, gold is not a button that says "war up, price up." The July 8 session suggests that dollar strength and the state of global capital flows deserve closer attention than the latest Iran headline if you want to read gold correctly. The next signals worth watching are whether DXY eases and whether US equities shift from sector rotation to broad defensive positioning.