Some market mornings do not suffer from a lack of data. They suffer from a lack of disciplined reading. China's latest price data is a good example: factory-gate prices kept rising, while the prices consumers actually pay slowed. If you compress those two signals into a single headline about recovery, you are probably moving faster than the evidence allows.

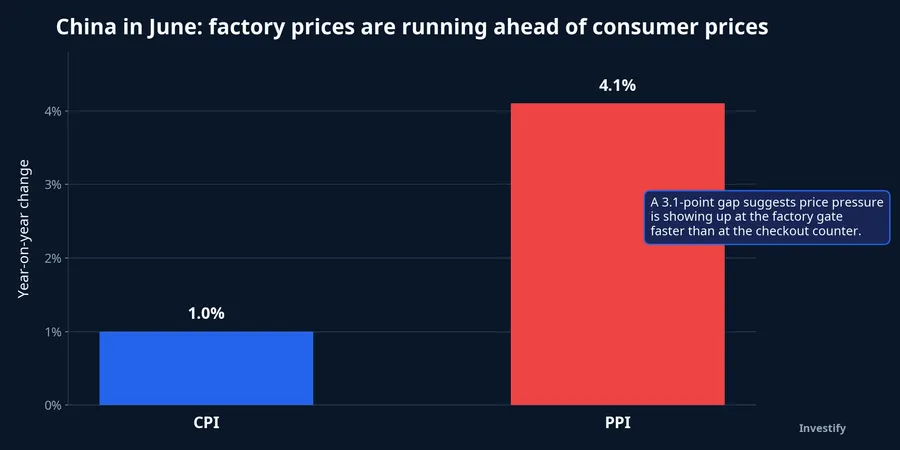

The gap is not trivial. China's June CPI rose 1.0% year on year, down from 1.2% in the prior month. At the same time, PPI climbed 4.1%, up from 3.9% previously.TradingEconomicsTradingEconomics In plain English, factories are still seeing more upward pressure in costs and selling prices, while end consumers are not absorbing that pressure at the same speed.

One economy, two different speeds

When CPI and PPI rise together, the story is usually easier to read. Companies are getting better prices, households are still spending, and the economy looks capable of digesting higher costs. This time, the picture is different. The 3.1-point gap between PPI and CPI suggests price pressure is staying closer to the production side instead of flowing cleanly through to consumer demand.

That matters because a busy factory floor is not the same thing as a broad consumer recovery. Production can hold up for a while thanks to supply-chain activity, existing orders, or the need to keep capacity running. But that does not automatically mean households are spending with more confidence. For newer investors, this is one of the easiest mistakes to make: seeing strength in factory data and assuming the whole economy has turned the corner.

The same gap also explains why "China recovery" trades often stall unless fresh consumer evidence shows up. A large economy can keep momentum on the industrial side for a time. But for that momentum to become a more durable growth story, someone still needs to buy goods, use services, and tolerate firmer prices at the checkout line.

What Vietnamese investors should take from that gap

For Vietnam, China is not just another overseas headline. It is a major trading partner, a demand center for several commodities, and an important anchor for broader Asian risk sentiment. That means a split data set like today's does not say everything is deteriorating. It says investors should stop forcing every asset class into the same conclusion.

The cleaner way to read it is to separate two layers of impact. The first layer is made up of sectors that respond quickly to production activity and supply chains. If Chinese factories still have support, materials and industrial names can keep a sentiment cushion. The second layer includes sectors that need stronger end demand to justify a more durable rerating, such as discretionary consumption, retail, and businesses tied more directly to final domestic demand in China. Today's data does not settle that case.

That distinction between "having support" and "being in recovery" matters more than it seems. The two phrases sound close, but they describe very different states. "Having support" means the worst-case macro fear has eased for now. "Being in recovery" means the evidence is strong enough for markets to reprice a much wider set of assets. The current data still fits the first bucket more comfortably than the second.

Commodities are telling a more practical story

If you want to see how markets are reading China in a more grounded way, commodities are the easiest place to look. Iron ore is sitting at USD 98.86 per ton, copper at USD 6.07 per pound, and Brent at USD 79.06 per barrel. That is not a collapse. But it is also not a clean confirmation of a synchronized growth cycle across every China-sensitive asset.

Iron ore holding close to USD 100 per ton suggests the market has not abandoned expectations around industrial activity. Copper remains at a relatively firm level, which implies industrial demand is not being priced as broken. Brent carries a more independent story because oil is also heavily shaped by supply risk and geopolitics, so it should not be folded too neatly into one view about Chinese domestic demand.

That is the practical takeaway: commodities may sit in the same asset bucket, but they do not all move for the same reason. If investors throw iron ore, copper, and oil into a single narrative, the decision that follows is likely to be noisier than it looks. A mature market separates what belongs to production, what belongs to consumption, and what belongs to energy-specific risk.

Asian equities are not confirming a straight-line recovery either

Regional index behavior points in the same direction. Shanghai stands at 3,970.88, down 1.4% over one week. Hang Seng is at 24,199.46, up 5.0% over a week but still down 3.1% over one month. Before the open, the VN-Index was at 1,853.70 after a 0.29% gain in the previous session. Those numbers describe a market that is stratifying risk, not one that has reached a strong consensus that China has entered a new, broad recovery phase.

For retail investors, that detail is more useful than whether the market opens up or down by a few points. A market that truly believes in a broad recovery usually produces better breadth, not just a rally in a handful of materials or industrial trades. If the reaction stays concentrated in commodity-linked names and supply-chain proxies, that is a selective read of the data, not a new market-wide thesis.

In other words, the tape may look upbeat in the short run, but breadth matters more than color. This is also where investors can avoid a familiar error: taking a single positive session and projecting it onto an entire quarter. This morning's China data does not justify that leap.

What this really says to investors

China's challenge right now is not the absence of positive signals. The issue is that the positive signals are showing up in the part of the economy that matters less for a durable recovery call. Factories may still be running. Factory-gate prices may still be firming. But if household demand does not catch up, the growth story stays vulnerable in the last mile.

So the disciplined conclusion is neither "China has recovered" nor "everything is getting worse." The better conclusion is that China's economy is still running at split speeds, and markets should be read at that same resolution. Materials and industrials may still have support. But a fuller recovery call needs clearer improvement in consumer demand, not just stability at a low level.

The next one to two weeks should therefore be watched through three lenses. First, does the market keep paying up for industrial commodities. Second, if equities rally, does breadth extend into sectors tied to final demand. Third, do the next Chinese consumption indicators begin to narrow the gap with the production side. As long as that gap stays wide, the safer thesis remains the same: factories have support, but the evidence is still too thin to call this a balanced recovery.