At first glance, many investors will read PLX's latest move in the most familiar way possible: the company is selling stock, supply is going up, and the share price could come under pressure. That reading is not entirely wrong, but it misses the most important layer. In Petrolimex's case, the treasury-share sale is first a capital-structure and public-company-compliance story, and only after that a short-term supply story on the tape.PetrolimexNhịp sống Kinh doanh

The July 8 resolution matters because PLX is not selling a small portion of its treasury stock. It is planning to sell all 23,285,846 treasury shares it currently holds. The transaction is expected to be executed through order matching on HOSE after approval from the State Securities Commission and after the company completes its disclosure procedures.PetrolimexDoanh Nghiệp Biz

What PLX is actually trying to fix

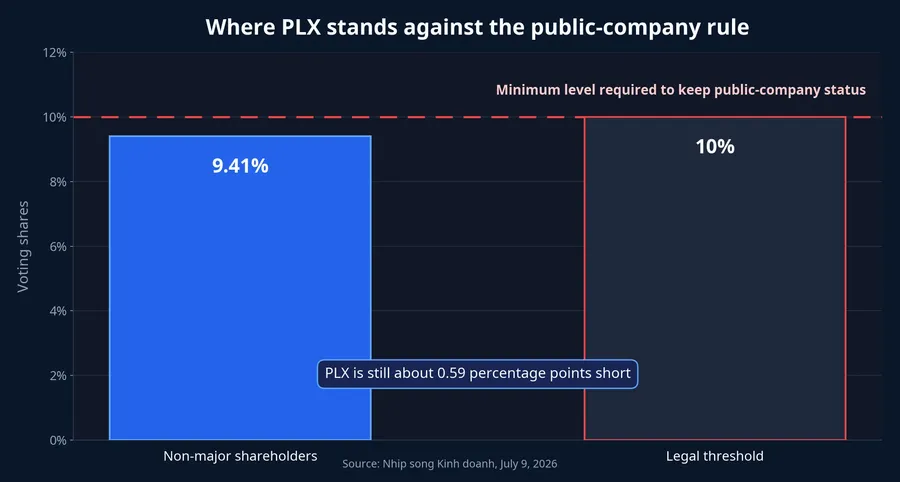

To read this properly, investors need to go back to the rule for a public company. Based on the way local outlets summarized the regulation, a company must have at least 10% of its voting shares held by at least 100 investors who are not major shareholders. PLX currently falls short of that line even though it has a large shareholder count.Doanh Nghiệp Biz

Nhip song Kinh doanh reported on July 9 that PLX's "other shareholders" group currently holds 9.41% of voting shares, below the 10% minimum. The gap is only 0.59 percentage points, but with ownership already tightly concentrated, that shortfall does not disappear on its own unless the company actively releases more stock into outside hands.Nhịp sống Kinh doanh

This is where many first-time investors misread the situation. A company can have tens of thousands of shareholders and still fail the public-company test if too little of the voting stock sits outside the major-shareholder circle. In PLX's case, the real issue is not how many people hold the stock, but how much stock is actually outside the control of large holders.

Once viewed through that lens, the treasury-share sale makes more sense. PLX does not have to wait for a large shareholder to sell down immediately. Instead, it can return shares from treasury to the market, lift the amount of stock available for trading and voting, and push the outside-holder ratio closer to or above the 10% threshold.Nhịp sống Kinh doanh

Why the word “sale” can be misleading

For many newer investors, “the company is selling shares” triggers two instant reactions. The first is more supply. The second is price pressure. Those instincts can be useful in some situations, but they become misleading when applied mechanically to treasury shares.

A treasury-share sale is not the same thing as a new issuance. These shares already exist. They were previously bought back by the company and are now being held in treasury. When PLX sells them, the shares return to investors and trade normally again. The main change is in the amount of stock available to the market and the voting pool outside the company, not in the creation of brand-new shares.PetrolimexDoanh Nghiệp Biz

That does not mean shareholders can ignore supply risk. Because the deal is expected to be executed through on-exchange matching on HOSE, the market still has to absorb a specific block of stock. If the eventual sale price comes at a steep discount to the market price, or if the process drags on, PLX could still face short-term technical pressure.

But between “supply pressure” and “dilution,” investors need to use the right term. With a new issuance, the concern is that new shares change existing ownership percentages. With a treasury-share sale, the key question is how the market absorbs old shares returning to circulation, who buys them, and where the actual execution price lands.

Why this tool makes sense for PLX

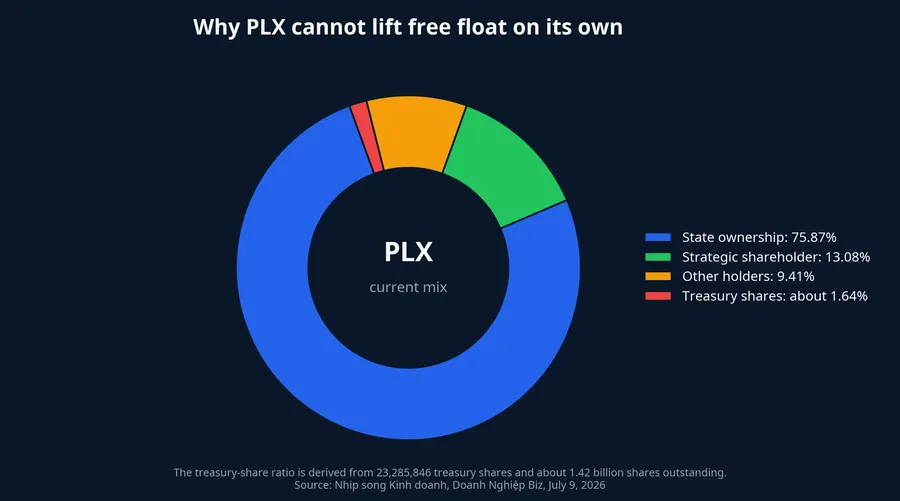

Nhip song Kinh doanh says the State currently holds 75.87% of PLX, the strategic shareholder owns 13.08%, and other shareholders hold only 9.41%. That mix shows why PLX's free float has been structurally tight for some time. When ownership is that concentrated, even a small shortfall can push the company below the public-company line.Nhịp sống Kinh doanh

There are at least two plausible ways to read the decision to sell all treasury shares. The first, and the one most strongly supported by the current sourcing, is that PLX needs an immediate fix to a legal ownership-structure problem. The second is that the company also wants more financial flexibility after management flagged capital needs at the 2026 annual general meeting.Nhịp sống Kinh doanhDoanh Nghiệp Biz

The evidence leans more heavily toward the first explanation. Even the July 9 reporting puts “meeting public-company requirements” ahead of “strengthening financial capacity.” In plain English, if PLX were not facing this ownership-threshold issue, the market would probably read the move as less urgent.

Still, the two motives should not be treated as totally independent. By returning treasury shares to the market, PLX can repair its free-float problem and raise cash at the same time. For a company of Petrolimex's scale, with meaningful working-capital needs, that secondary benefit is still material even if it does not appear to be the primary driver.

The real market test is price execution

One constructive detail is that PLX is not talking about selling at any price. According to July 9 reporting, the minimum offer price cannot fall below the appraised share value stated in a June 9 valuation certificate from CPA Vietnam. The order price must also comply with a HOSE rule tied to the reference price and 50% of the daily price band.Nhịp sống Kinh doanh

That matters more than the initial reaction to “more supply.” If the eventual execution price stays reasonably close to the market range, investors may see this as a controlled technical restructuring step. If later disclosures show a meaningful discount was required, the market will have grounds to reassess how strong demand for PLX really is.

The transaction is also not ready to happen immediately. The resolution makes clear that the plan still depends on regulatory approval and the completion of required disclosure steps. So the disciplined response here is not to guess the final price impact right away, but to watch how quickly the plan moves from board resolution to actual execution.Petrolimex

What PLX shareholders should watch next

The first signal is timing: when approval comes through and when the sale window actually opens. A technically sound plan that takes too long to execute can still leave the market pricing in supply risk for multiple sessions. In that case, short-term volatility may reflect uncertainty rather than business quality.

The second signal is the realized sale price relative to where PLX trades on the exchange. The test is not just whether the company can sell the block. It is whether it can do so at a level the market accepts without demanding a large concession. With treasury shares, execution quality usually matters more than the headline.

The third signal is the outside-holder ratio after the transaction. If the real objective is to push that figure above 10%, investors should not stop at a successful sale announcement. The more important question is whether the deal actually resolves PLX's public-company compliance issue.

The clearest conclusion is this: PLX's treasury-share sale should be read first as a public-float and capital-structure adjustment, not as an automatic negative signal for the stock. Supply risk is still real, but it only becomes the dominant issue if execution is weak or market absorption is poor. The key markers to watch in the coming sessions are regulatory approval, the realized sale price, and the post-transaction free-float ratio.