A VND 500 billion bond issue does not, by itself, prove that the market is back to normal. But once that deal is placed inside the full sequence from late May to late June, the story changes. Home Credit was issuing new bonds, repaying maturing ones on schedule, and then coming back for more funding. For a consumer finance company, that is a more meaningful signal than a single headline number.ANTT

In plain terms, banks have a large deposit base to lean on. Consumer finance companies do not. They depend far more heavily on wholesale funding, including bonds, bank borrowing, and other market-based sources. When the bond window shuts, pressure shows up quickly in their ability to keep lending. When they can refinance nearby maturities and still raise fresh money, the market is signaling that confidence is returning, at least for selected issuers.

The first thing to watch is the sequence, not the VND 500 billion headline

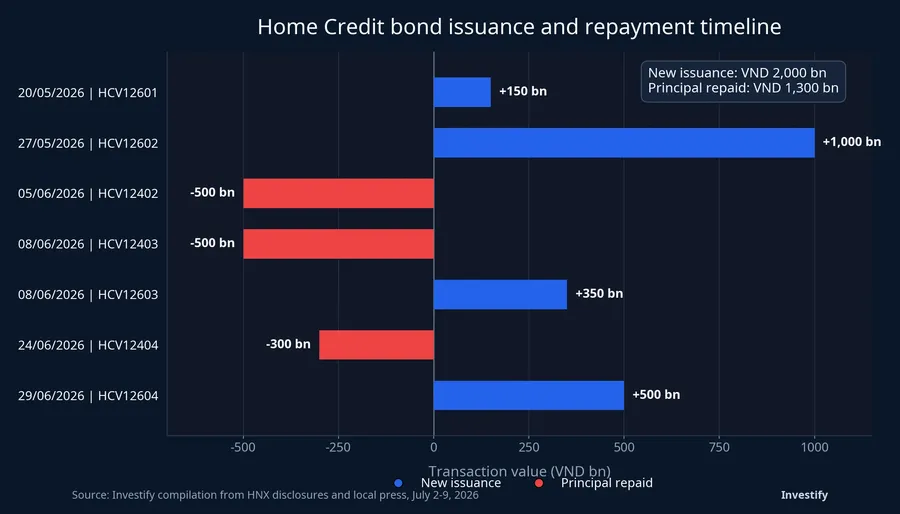

In its July 9 update, Home Credit disclosed a successful VND 500 billion issue under bond code HCV12604 on June 29, with a 36-month tenor and a blended coupon of 9.8% per year. Before that, it had sold VND 350 billion under HCV12603 on June 8, with a 24-month tenor and a 9.5% coupon.ANTT

The pattern did not begin in July. A July 2 report showed that Home Credit had already issued VND 1,000 billion under HCV12602 on May 27 and another VND 150 billion under HCV12601 on May 20, both with 36-month maturities.ANTT

That matters because repeated market access says more than a one-off deal. A single placement may simply reflect an immediate funding need. Several placements over a six-week stretch suggest that buyers were willing to keep showing up long enough for the issuer to pass multiple confidence checks.

That does not mean funding has become cheap again. The two most recently detailed deals were priced at 9.5% and 9.8% a year. That is a clear sign that institutional buyers still demand a meaningful risk premium when lending to consumer finance names.ANTT

Scheduled repayment matters just as much as new issuance

If readers focus only on the issuance side, they miss half of the picture. During June, Home Credit repaid VND 500 billion of principal on HCV12402 on June 5, another VND 500 billion on HCV12403 on June 8, and VND 300 billion on HCV12404 on June 24. It also paid the related coupon amounts of VND 33.8 billion, VND 33.8 billion, and VND 20.3 billion, respectively.ANTTANTT

For bond investors, that is the real test. Equities can survive on expectations for a long time. Bonds cannot. Bondholders ultimately care about whether principal and interest are paid on time. That is why a company that repays VND 1,300 billion of principal in one month and still raises new money deserves closer attention than a company that only announces fresh issuance without proving its recent repayment discipline.ANTTANTT

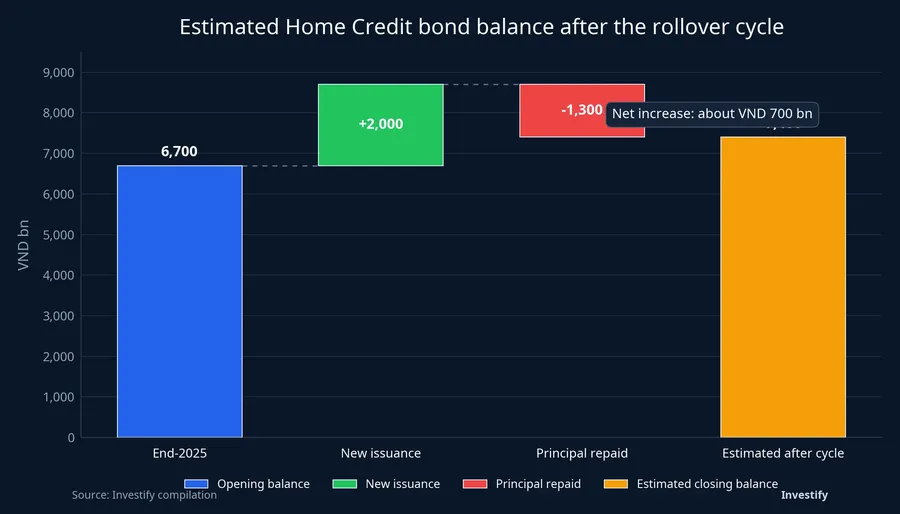

Using the figures disclosed this week, Home Credit's outstanding bond balance can be estimated to have moved from about VND 6,700 billion at the end of 2025 to roughly VND 7,400 billion after this issuance-and-repayment cycle. The math is straightforward: add VND 2,000 billion of new issuance and subtract VND 1,300 billion of principal already repaid.ANTTANTT

That roughly VND 700 billion net increase is not just arithmetic. It suggests that Home Credit is not simply piling on leverage as fast as possible. Instead, it appears to be running a controlled refinancing cycle: retiring old debt, maintaining access to fresh funding, and allowing the bond book to grow only moderately. For a consumer finance lender, that says more about market access quality than about expansion ambition alone.

The background is stronger earnings, but also a heavier liability structure

The July 9 report said Home Credit posted nearly VND 2,077 billion in after-tax profit for 2025, up 60.9% from the previous period. Equity stood at roughly VND 8,280.9 billion, while total liabilities were close to VND 29,109.3 billion. Bond debt alone rose from VND 3,100 billion to VND 6,700 billion by the end of 2025.ANTT

Read another way, Home Credit entered 2026 with two realities at once. Profitability improved, which gives the company a larger cushion against higher funding costs. But the liability side also grew materially, which means funding discipline matters more, not less.

That is why it would be too simplistic to conclude that stronger profit automatically makes the bonds safe. Earnings help, but the more important test in credit markets is whether the issuer can cross each maturity cluster without disrupting cash flow. Based on the disclosures published this week, Home Credit appears to have done that for one meaningful cluster. That is better than a profit headline alone, but it still does not erase the pressure created by a high cost of capital.

The bond channel is reopening, but not on equal terms for everyone

Home Credit's story also sits inside a broader market shift. According to a weekly VBMA market report cited by Thoi bao Tai chinh, Vietnam's corporate bond market recorded 35 issuance deals worth VND 49,650 billion during the June 29 to July 3 week. Cumulative issuance since the start of 2026 reached VND 218,958 billion, with private placements accounting for 88.7% of the total.Báo Mới

The message is fairly clear. The bond market is no longer frozen in the way it was during the post-crisis confidence collapse. But it has not returned to an easy-money regime either. Most issuance is still happening through private placements, where buyers are typically institutions or qualified investors with stronger screening standards.Báo Mới

So Home Credit can reasonably be read as a sign that the funding channel is reopening. What it cannot yet prove is that all corporate bonds have moved back into a comfort zone. The cleaner reading is that confidence is coming back selectively, and issuers still have to pay for that access through higher coupons and a credible repayment record.

What retail readers should take away

The key lesson is not that Home Credit raised another VND 500 billion. The key lesson is that new issuance only becomes meaningful when it is read alongside old debt repayments, the coupon on fresh funding, and the issuer's balance-sheet capacity to absorb that cost.

Viewed separately, the story fragments into disconnected headlines such as "new issuance," "paid on time," or "profit up sharply." Put together, the pattern is much clearer: the bond channel for consumer finance is showing signs of reopening, but it is reopening with tougher pricing and more visible selectivity. The most defensible thesis here is that confidence is returning in a disciplined way, and issuers still need to earn it with both higher coupons and cleaner repayment behavior.

The next thing to watch is not just whether another bond deal appears. What matters more is whether Home Credit and its peers can sustain this refinancing rhythm, and whether the current cost of capital starts to eat into future margins. That will tell readers whether the market window is truly widening, or whether it is only open for the strongest files.