A 6-7% rally always creates the feeling that the story is already settled. In fertilizer stocks on July 8, however, the market was not confirming a brand-new upcycle. It was pricing in an assumption: DPM's estimated first-half results are strong enough to put the whole sector through a margin durability test.

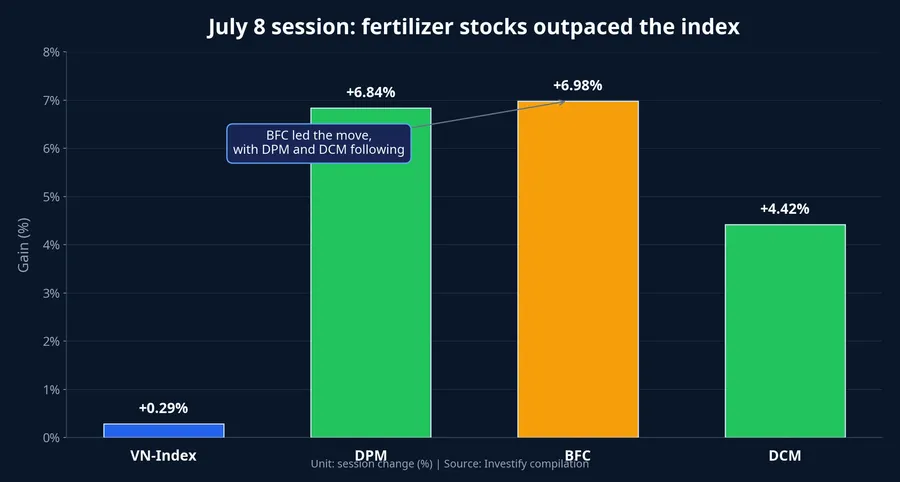

Put simply, the tape shows the surface, not the substance. DPM rose 6.84% to VND 24,200 per share, BFC gained 6.98% to VND 56,700, and DCM added 4.42% to VND 36,650 while the VN-Index edged up just 0.29%. That gap suggests money was not following the broader market. It was chasing a sector-specific earnings narrative.

A strong session does not settle the case

If you only look at the green screen, it is easy to conclude that the entire fertilizer group suddenly became attractive at once. That is understandable, but incomplete. Stocks moving together in one session does not mean they are being re-rated for the same reason.

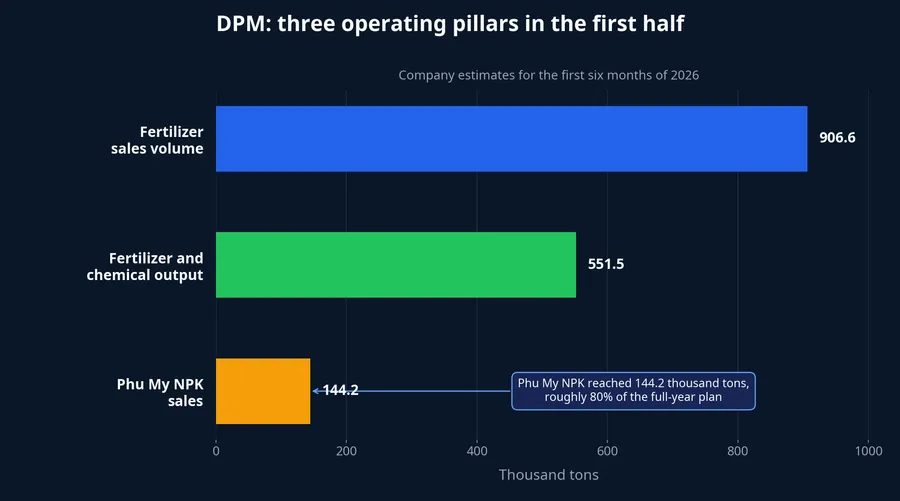

The starting point this time was DPM, not a fresh commodity shock or a sweeping policy catalyst. According to Fili, DPM estimated first-half 2026 production at 551.5 thousand tons of fertilizers and chemicals. Phu My urea equivalent reached 434.3 thousand tons, or 106% of the six-month plan, while Phu My NPK reached 111.2 thousand tons, or 126% of plan.Fili

The commercial side looked even stronger. DPM estimated fertilizer sales volume at 906.6 thousand tons, equal to 132% of its first-half target. Phu My NPK alone sold 144.2 thousand tons, beating the six-month plan by 45% and contributing more than VND 1,800 billion in revenue.Fili

That matters because DPM is not just reporting a one-off headline. The company is showing that plants ran steadily, sales held up, and NPK is no longer a side note in the earnings mix. For investors, that is the difference between a rumor-driven spike and the early phase of an earnings re-rating.

What exactly is the market paying for

Fertilizer producers do not live off tonnage alone. The real question is how much pricing power they keep, how expensive feedstock becomes, and how much spread remains after plants run at high utilization. That spread is the margin story.

DPM is drawing attention because two pieces are showing up at the same time. First, volumes came in well above plan. Second, the company still posted a constructive operating picture even though average gas prices in the first half were about 16% above plan, while cost-saving measures still amounted to roughly VND 90 billion.Fili

That is why this move is more interesting than a routine momentum burst. If input costs are rising and the company still delivers a strong operating update, the market has reason to ask whether actual earnings could end up stronger than earlier expectations. But asking that question is not the same as answering it. Fertilizer profitability moves quickly once urea prices change direction.

Margins, not price action, are the real test

Retail investors often miss the sequencing here. Stocks usually react before the official financial statements arrive. The market buys the expectation first, then uses the reported numbers to confirm or reject it. That means the July 8 rally should be read as the opening phase of a validation process, not the final verdict.

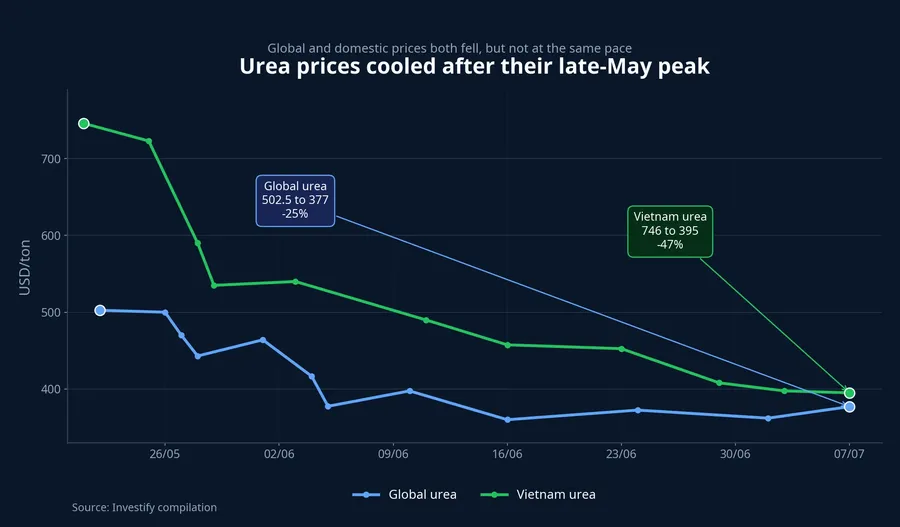

Commodity data in the source article shows global urea at USD 377 per ton on July 7, down materially from USD 502.5 per ton on May 22. Vietnam urea prices also fell from USD 746 per ton on May 21 to USD 395 per ton on July 7. During the same period, global natural gas hovered around USD 3.30 per MMBtu on July 8.Fili

That does not mean DPM's gas cost will track international gas prices one for one. Domestic gas pricing depends on local contracts and its own formula. But it is enough to remind investors that urea earnings are a spread business. If selling prices fall faster than input costs, margins get squeezed. If pricing holds while plants continue to run well, profits can stay on firmer ground.

Why BFC moved with DPM, but is not the same story

When the whole group turns green, the most convenient conclusion is that every fertilizer company is about to benefit in the same way. That is rarely true. DPM is heavily tied to urea economics, gas costs, and the growing contribution of NPK. BFC is more exposed to NPK, seasonal demand, and the markets it serves.

That distinction matters. BFC's surge in the same session may show that the market is extending DPM's earnings story to the broader fertilizer complex. But that is still a sector-level inference, not proof that every company's profit engine is improving at the same pace. In sector rallies, the basket usually moves first and fundamentals sort the winners out later.

This is where new investors often confuse a shared narrative with shared earnings quality. One stock can rise because revenue is real, volumes are real, and costs are under control. Another can rise because capital is simply rotating into the theme. The same color on the screen can still imply very different staying power.

What will decide whether this move lasts

The first signal to watch is DPM's next financial statement. The estimated operating data looks strong, but only the official numbers will show how much gross margin held and where profit actually came from. If revenue expands while gross margin compresses sharply, expectations will need to be marked down fast.

The second signal is the role of Phu My NPK. Sales volume of 144.2 thousand tons in the first half suggests the segment is no longer peripheral to the urea story. If NPK keeps selling well, DPM gains a second earnings cushion and becomes less dependent on one variable alone: urea pricing.Fili

The third signal is the next move in domestic urea prices. If output prices keep softening while input costs do not fall in step, the current enthusiasm will be hard to sustain. If selling prices stabilize better than expected and volumes remain solid, the market will have a stronger case for treating this as more than an early reaction to good news.

Conclusion: this is a test, not a certificate

The cleanest thesis right now is that the market is testing the durability of fertilizer earnings, with DPM as the lead case. The July 8 rally has more grounding than a random burst of speculation because it followed a strong estimated set of data on output, sales, and cost savings. But it still does not certify that the sector's second-half earnings story is secure.

In other words, the market has a basis for optimism, but it still needs proof. If official results show resilient margins and NPK continues to contribute meaningfully, this rally could mark the start of a broader earnings re-rating. If urea prices fall faster than companies can protect the spread, the group is likely to diverge again, and quickly.

The three signals worth watching over the next two weeks are clear: DPM's actual gross margin, the pace of NPK sales, and any fresh move in domestic urea prices. Those will tell investors whether July 8 was the beginning of a bigger reset, or simply capital moving early on a good headline.