Before Vietnam's market opens on July 8, investors are facing a familiar but uncomfortable setup: a dramatic geopolitical headline arrives overnight, yet asset prices do not react in a single line. The U.S. resumed strikes on Iran after attacks on commercial vessels near the Strait of Hormuz, while also tightening Iran's ability to sell oil under a temporary arrangement.AP For newer investors, the instinct is usually simple: if the war story gets bigger, everything risky must fall together. The market is not saying that yet.

The core thesis is straightforward. At this stage, the Hormuz shock is being priced first through oil, not through a broad-based flight from risk across every asset class. That does not mean Vietnamese equities are insulated. It means the cleanest way to read the July 8 session is to start with crude, then move to gold, then the dollar and exchange rate, and only then draw conclusions about VN-Index.

Why Hormuz hits oil before it hits everything else

The Strait of Hormuz is not just another geopolitical flashpoint. The U.S. Energy Information Administration says an average of 20 million barrels per day of crude oil and petroleum products moved through the strait in 2024, or about 20% of global consumption.EIA When military risk rises around a chokepoint of that size, oil is almost always the first asset to respond because the story is immediately about supply.

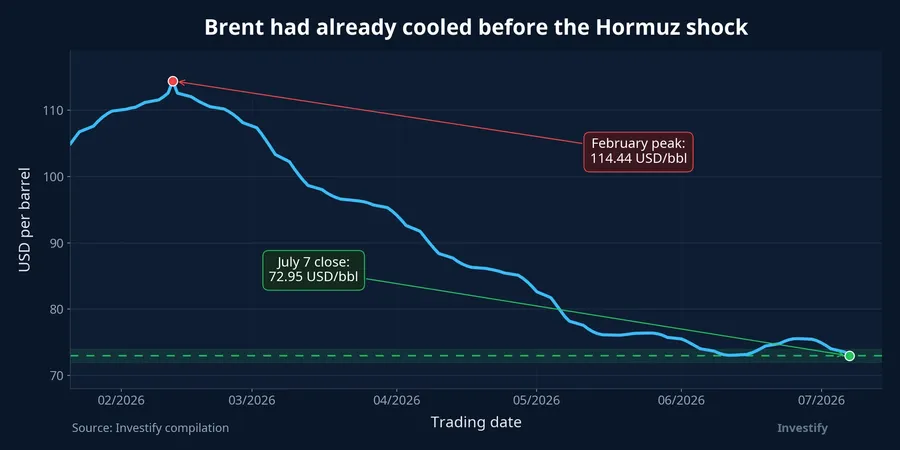

But the first move is not always the final verdict. Brent closed on July 7 at USD 72.95 per barrel, up 1.33% from the previous session. That is enough to show the market adding a geopolitical risk premium, but not enough to suggest panic pricing around a prolonged supply disruption. Money is reacting to the threat, not yet to a confirmed supply shock.

The more revealing point is the starting level. In Investify's internal series, Brent had reached USD 114.44 per barrel on May 4 before sliding back to the low-USD 70s ahead of July 8. That matters because this is not an already overheated market being pushed further. It is a cooler oil market being tested by a fresh geopolitical event. If Brent only oscillates around current levels over the next few sessions, traders are likely treating the event as a short-term risk premium. If it quickly reclaims the USD 78-80 range, the market will be telling a different story: supply risk is being repriced more seriously.

That is why oil has to be read before equities. Retail investors often make one of two mistakes at this point. They either sell everything because the headline feels dangerous, or they rush into any stock associated with oil without checking whether the commodity move is durable. Both reactions skip the central question: what exactly is crude itself confirming?

Gold has moved, but not enough to confirm a full defensive shift

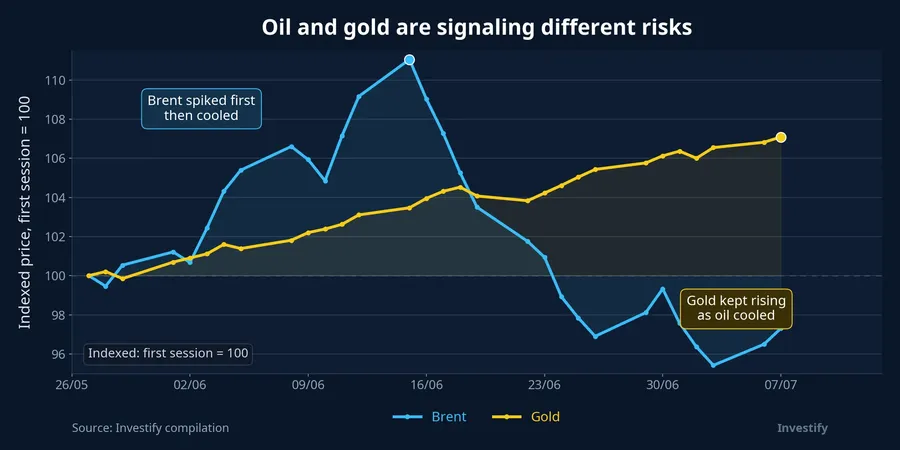

Gold is usually the second chart people open when geopolitical stress rises. But in the first hours of a shock, gold does not always move more aggressively than oil. On July 7, spot gold closed at USD 4,169.70 an ounce, up just 0.12%. Against Brent's move in the same session, that is a restrained reaction.

That restraint matters. When gold is lagging oil, the market is often treating the event as an energy shock more than a full-system risk event. If gold clears USD 4,200 an ounce while Brent keeps climbing, the two signals begin to reinforce each other and suggest that defensive positioning is broadening. If oil rises while gold stays flat, the shock is still concentrated in commodities rather than in generalized risk aversion.

For Vietnamese readers, gold always comes with extra domestic noise, from local price gaps to product-specific supply conditions. But ahead of the open, discipline matters more than local narratives. Global gold needs to confirm the safe-haven story first. Without that confirmation, using oil alone to conclude that the whole market is panicking would be a leap beyond the evidence.

Wall Street weakened, but that is not yet a verdict on VN-Index

U.S. equities did show a risk-off tone on the night of July 7, but even there the move cannot be reduced to a single cause. AP reported that the S&P 500 fell 0.4% to 7,503.85, the Nasdaq dropped 1.2% to 25,818.69, and the Dow Jones Industrial Average slipped 0.2% to 52,925.15.AP Those numbers matter, but they are not enough on their own to say Vietnam must open in the same direction.

Vietnam does not absorb global stress through exactly the same channels as the U.S. VN-Index closed July 7 at 1,848.25, up 0.26%. The latest DXY print in the system was 100.96, while USD/VND stood at VND 26,303.50 per dollar. As long as the dollar is not breaking sharply higher, oil's pass-through into exchange-rate stress is still cushioned. The same geopolitical headline may hit U.S. semiconductors first, while in Vietnam it can surface earlier in energy, airlines, transport, or other fuel-sensitive groups.

Put differently, a weaker Nasdaq is a reference point, not a command. If investors skip the FX layer and only stare at Wall Street, they fall into a mechanical framework: the U.S. is red, so Vietnam must be red too. In practice, Vietnam often absorbs external shocks through sector rotation and the resilience of domestic liquidity rather than by copying New York's color board.

Vietnamese oil names are already showing why sector detail matters

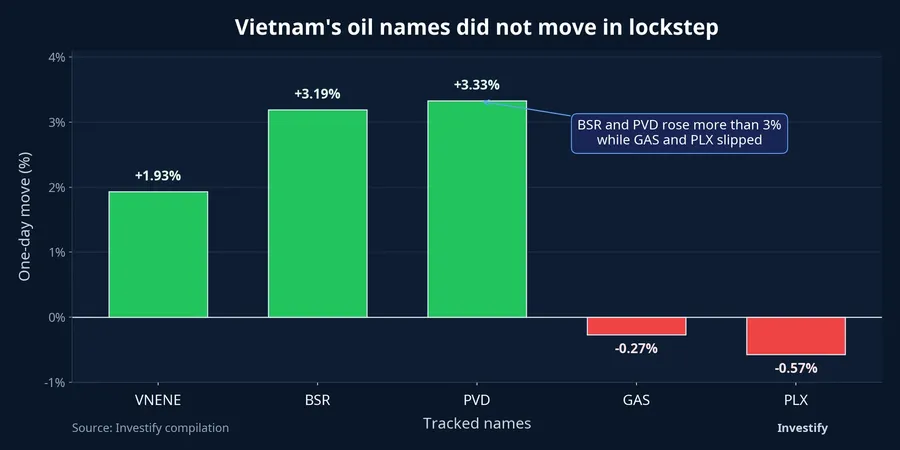

The most useful domestic signal so far is that energy stocks are not moving as one block. The VNENE index gained 1.93% on July 7. In the same session, BSR rose 3.19% and PVD gained 3.33%, while GAS fell 0.27% and PLX slipped 0.57%. The numbers do not support a crude shortcut like “oil up means all oil stocks up.” They support a more realistic reading: flows are separating companies by business model, earnings sensitivity, and what investors want to own in the first leg of the shock.

That is the real lesson for less experienced investors. When a large headline hits, the correct reaction is not to throw every stock with an oil label into the same basket. Different businesses face different exposures to crude prices, feedstock costs, regulated pricing, and margin structure. A rise in Brent can improve expectations for one name while raising cost pressure or margin risk for another. The July 7 divergence is a reminder that understanding the mechanism is more valuable than reacting to the headline.

A cleaner checklist for the July 8 open

If the entire situation has to be reduced to one practical framework, it should be a four-step sequence. First, check Brent. If crude is only holding a moderate gain, the market is still in an alert state rather than a panic state. Second, check gold. If gold is not confirming, a broad flight to safety has not fully formed.

Third, check DXY and USD/VND. That is the layer that decides whether an oil shock is starting to become a currency-pressure story for Vietnam. If the dollar jumps together with oil and gold, the burden on equities becomes more serious. Only then does step four come into focus: VN-Index itself, and not just the headline point move but the underlying structure of flows into energy, defensives, or a broader selloff.

The most coherent conclusion at this point is not a confident call that the market will open green or red. It is this: Hormuz is large enough to push oil higher first, but the other asset classes have not yet confirmed a full, system-wide risk-off phase. For Vietnamese retail investors, the difference between an oil bounce and a broader shock is the difference between emotional reaction and disciplined reading. The signals that matter most on the morning of July 8 are still Brent, gold, DXY, USD/VND, and the breadth of VN-Index flows, in that order.