Four ships turning back at the Strait of Hormuz on July 8 were more than another war headline. They signaled that the oil market was repricing route risk before any clear physical supply shock had fully materialized.CafeF

That distinction matters, especially for newer investors. Oil does not only rise when wells stop pumping or export terminals shut down. It can also rise when buyers, sellers, shipowners and insurers all demand a higher risk premium because cargoes may be delayed, rerouted or unable to pass on schedule.

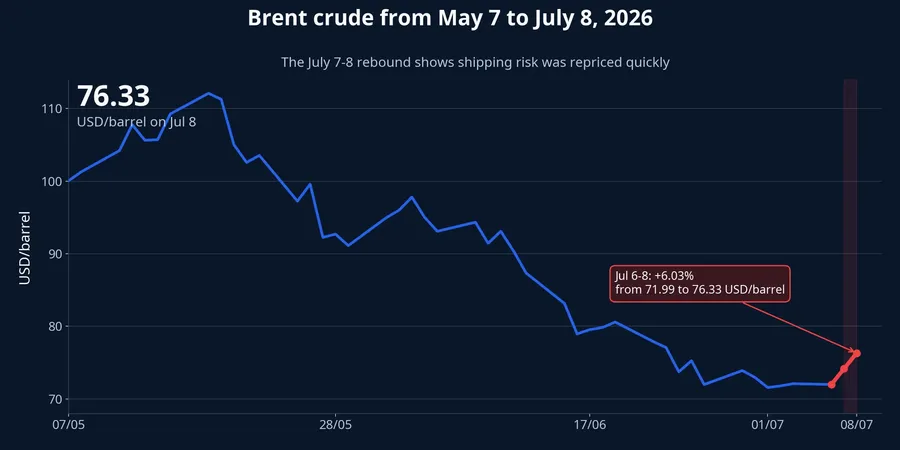

Brent is reflecting exactly that logic. Brent settled at USD 71.99 per barrel on July 6, rose to USD 74.16 on July 7 and reached USD 76.33 on July 8. From July 6 to July 8, that was a 6.03% increase, large enough to show a rapid repricing of logistics risk, even if it still falls short of a full panic move.

Why Hormuz matters so much

Hormuz is not just another shipping lane on the global energy map. According to the EIA, about 20.9 million barrels per day moved through the strait in the first half of 2025, equal to roughly 20% of global liquids consumption.EIA When a chokepoint that large starts to look unsafe, oil can react before inventories or production data show a measurable shortage.

For investors, it helps to separate two layers of risk. The first is supply risk: are oil fields, refineries or export terminals being disrupted? The second is route risk: the oil still exists, but it may not move on time, on schedule or at the same cost. Brent's jump on July 7-8 looks much more like the second category.

That is why the rerouted ships matter. CafeF, citing Kpler and LSEG data, reported that the LNG vessels Al Ghariya, Duhail and Al Ruwais changed course late on July 7, while an Indian-flagged tanker carrying 2 million barrels of Kuwaiti crude also turned back on July 8.CafeF Markets do not wait for confirmed shortages. If the probability of delivery along the intended route drops, prices adjust almost immediately.

What matters more than the headline

In a story like Hormuz, the war headline is not always the most useful signal. The better indicators are whether more ships keep turning back, whether vessels return to the route, how marine insurance changes and whether freight costs move higher. Once risk has shifted into logistics, shipping data often becomes more informative than traditional supply-demand commentary.

It is also important not to overstate causality. Brent's two-day rise alongside these course changes is a strong correlation, but that does not mean every percentage point came from a single source. Military escalation, defensive positioning in commodities and broader concern over Gulf supply may all be contributing. Still, among the signals visible on July 8, the rerouted ships were the clearest direct evidence that the cost of the route itself was being repriced.

That is different from a conventional supply shock. When production is disrupted, markets focus on lost barrels. When the problem is transportation, oil can rise even if production continues normally, simply because delivery has become less reliable and more expensive. That is why Hormuz should not be read as a simple supply story.

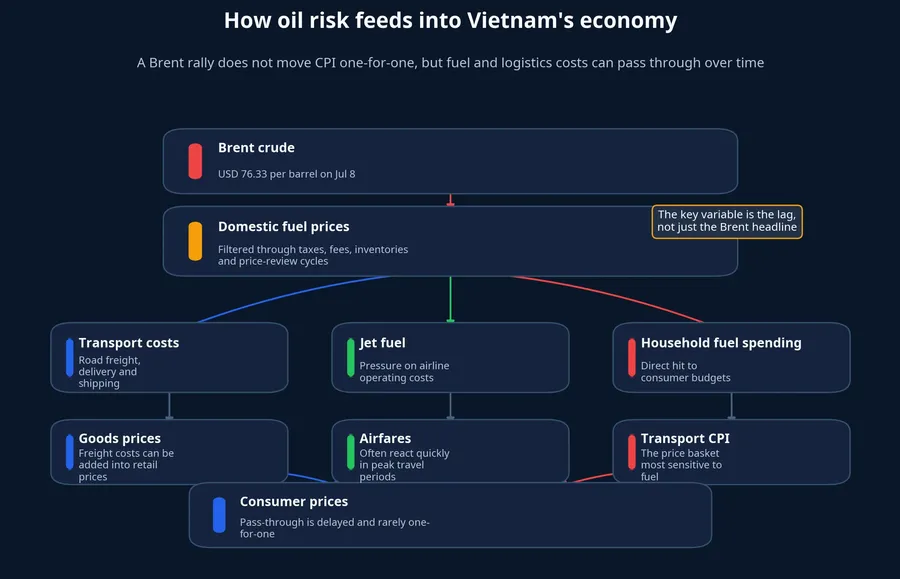

How the shock reaches Vietnam

The nearest transmission channel for Vietnam is domestic fuel pricing. In the latest database update, RON 95-V gasoline stood at VND 21,610 per liter on July 2, diesel 0.05S-II at VND 21,170 per liter and kerosene at VND 20,960 per liter. If Brent stays elevated through several more pricing cycles, the effect will not stop at gas stations. It can move into transport costs, delivery fees, airfares and eventually broader consumer prices.

In plain terms, Brent does not pass through into CPI one-for-one. Domestic prices are filtered through taxes, fees, inventories, exchange rates and administrative review cycles. But for retail investors, the key lesson is that a lag does not eliminate the effect. It only spreads the effect over time, from visible fuel prices into less visible pressure on logistics and corporate margins.

Another useful indicator is container freight. The database shows the containerized freight index at 3,326.87 points on July 8, up sharply from 2,218.15 on May 28. That does not prove Hormuz is the only driver. It does show that global shipping was already on a sensitive footing, which means a prolonged disruption at Hormuz could widen the freight premium and spread the oil shock more broadly through logistics.

Which stocks react first

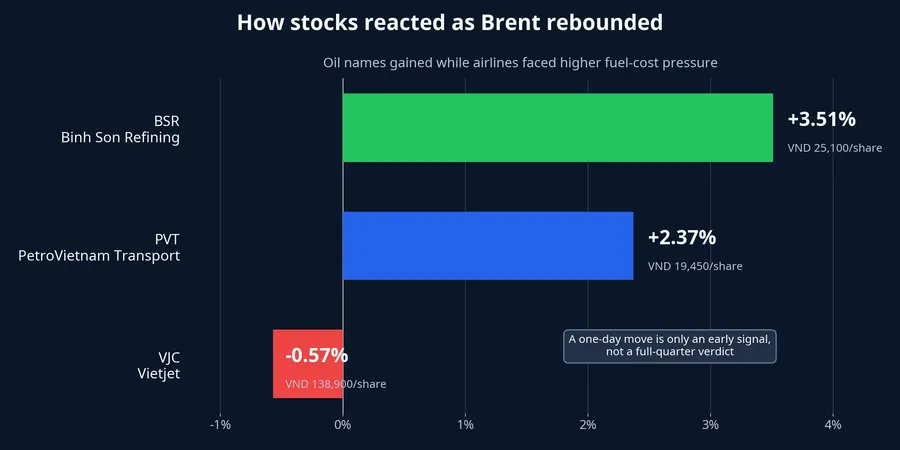

On equities, the first response usually follows cost structure and earnings expectations. BSR closed at VND 25,100 a share on July 8, up 3.51%. PVT, PetroVietnam Transport, rose 2.37% to VND 19,450. VJC moved the other way, slipping 0.57% to VND 138,900.

The pattern is intuitive. When oil rises because shipping risk has returned, investors often look first at companies tied directly to the upstream, refining or transport side of the energy chain. Airlines, by contrast, are immediately examined through the lens of fuel costs because that line item is one of the most sensitive parts of the operating model.

Still, a single session should not be treated as a verdict on the quarter. A gain in an oil name on July 8 does not automatically mean stronger third-quarter earnings. A mild decline in an airline stock does not capture fare increases, fuel hedging or peak-season demand. The right way to use this move is as an early sorting signal for what to monitor next, not as a substitute for fundamentals.

The core thesis

The bigger picture is that oil is no longer being priced only through the question of whether supply will disappear. It is also being priced through the market's growing doubt about the safety of the world's most important energy route, and when that doubt appears, prices react before delivery data confirms a shortage. That is why a tanker turning back is a more valuable signal than a generic conflict headline.

The cleanest conclusion, then, is this: if Hormuz keeps flashing signs of shipping disruption, Brent can stay on a higher floor even without an immediate production outage. If vessels return quickly and insurance pressure fades, that route premium can also unwind quickly. The practical watch list for the next few sessions is the number of ships changing course, the direction of freight costs and how energy, shipping and airline stocks behave after the first shock.