A 48% growth figure can make it look as if the entire steel cycle has turned at once. But Hoa Phat's latest operating update says something more specific: new capacity is ramping well, while end-demand is still uneven across product lines. For a cyclical business, that distinction matters far more than the headline growth rate.

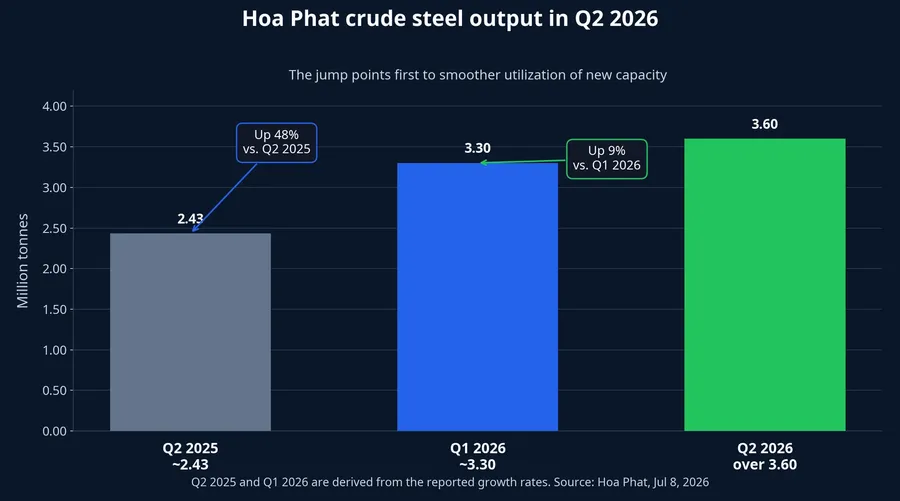

Start with the top-line number. Hoa Phat produced more than 3.6 million tonnes of crude steel in Q2 2026, up 48% year over year and 9% from Q1 2026.Hòa Phát That is large enough to pull investor attention quickly, especially because Hoa Phat still shapes how much of the market reads the Vietnamese steel sector. Yet crude steel output mainly tells you that furnaces are running harder and capacity is being used more efficiently. It does not, by itself, prove that construction steel demand has broadly rebounded.

The output jump is real, but it is not broad-based

The most important reading of this quarter is that the surge in crude steel output lines up with smoother utilization of new capacity. Hoa Phat now has annual capacity of 16 million tonnes and remains Southeast Asia's largest steel producer.Hòa Phát When a company adds meaningful capacity, the first thing investors should watch is not just sales volume but whether the new lines are being filled. Q2 points to a constructive answer on that front.

If you stop at the aggregate number, the easy conclusion is that steel demand has recovered across the board. That is too quick. In steel, a strong growth print can come from several sources at once: new capacity, exports, product mix, pricing, or genuine end-market demand. The analytical job is not to memorize the growth rate. It is to separate which of those forces actually created it.

HRC is doing most of the heavy lifting

The clearest source of acceleration in Hoa Phat's Q2 report is HRC, or hot-rolled coil. Total sales of HRC, construction steel, high-quality wire rod and billet reached 3.5 million tonnes in the quarter, up 35% from a year earlier.Hòa Phát HRC alone came in at 1.9 million tonnes, up 31% from Q1 2026 and 64% from Q2 2025.Hòa Phát

That matters because HRC gives Hoa Phat more routes to market than construction steel alone. It feeds pipes, coated sheet, fabricated metal products, industrial equipment and other downstream applications. The company said 80% of current HRC volume is absorbed domestically, with the rest exported, and that it has already shipped HRC to 20 countries and territories.Hòa Phát In practical terms, HRC reduces reliance on one narrow demand channel inside Vietnam's housing and construction cycle.

Once HRC is set beside the construction-linked segment, the picture becomes clearer. Construction steel and high-quality wire rod totaled only 1.3 million tonnes in Q2. That was up 2% from Q2 2025 but down 9% from Q1 2026.Hòa Phát The product group tied more closely to building sites and housing therefore failed to keep pace with total output. That single detail changes how the full report should be read.

Construction steel demand still lacks confirmation

If domestic construction demand were rising evenly, this segment would typically move much more clearly alongside crude steel output. Q2 did not show that. So the more accurate conclusion is not that "the steel industry has recovered strongly." It is that Hoa Phat is using new capacity more effectively, especially in HRC, while the construction side remains more tentative.

The first-half numbers point in the same direction. In the first six months of 2026, Hoa Phat produced nearly 7 million tonnes of crude steel, up 36% from a year earlier. Combined sales of HRC, construction steel, high-quality steel and billet reached 6.5 million tonnes, up 32%. HRC alone was close to 3.4 million tonnes, up 57% year over year.Hòa Phát Across that sequence, the growth engine is clearly more industrial than construction-led.

That is not inherently negative. For Hoa Phat, it shows the company is widening its demand base through a broader product mix. But for investors using Hoa Phat as a proxy for the sector, it is a reminder not to compress every signal into one industry-wide conclusion. A company can post sharp growth because internal execution has improved, even while part of its end-market remains only modestly better.

Pricing also favors HRC over construction steel

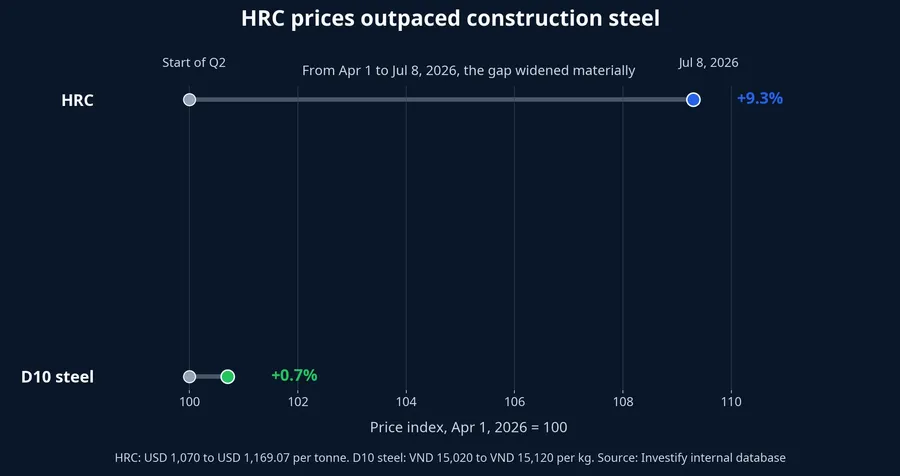

Internal price data supports the same interpretation. From April 1 to July 8, HRC prices rose from USD 1,070 per tonne to USD 1,169.07 per tonne, or about 9.3%. Over the same period, domestic D10 steel edged up from VND 15,020 per kg to VND 15,120 per kg, roughly a 0.7% increase.

That gap matters because it suggests the strong HRC volume story is not only about capacity coming onstream. It is also happening in a more supportive pricing environment than construction steel. Put differently, if investors expect better earnings in coming quarters, the cleaner argument sits with HRC and Dung Quat 2 utilization, not with a blanket assumption that the whole construction cycle has already turned.

On the stock side, HPG closed at VND 23,200 on July 8, below VND 24,239 on April 1, which means the shares were down about 4.3% over the period. By contrast, the VN-Index climbed from 1,702.93 to 1,853.70, or about 8.9%. That divergence suggests the market is not ready to rerate the stock on output alone. Investors still want clearer evidence on margins and the quality of realized selling prices.

Conclusion: brighter for Hoa Phat, not yet for the whole market

The thesis here is straightforward. Hoa Phat's Q2 2026 operating report is constructive for the company itself, but it is not enough to confirm a broad-based recovery in construction steel demand. The strongest evidence today sits with better utilization of new capacity and faster growth in HRC than in the rest of the portfolio. That is exactly the distinction newer investors tend to miss when they read only the first line of a corporate update.

Three signals will determine whether the story extends in the second half. First, whether HRC can sustain both volume and a supportive price environment. Second, whether construction steel can move out of its current low-growth pattern and begin to reflect clearer project demand. Third, whether earnings ultimately show that higher output is translating into better margins. When those three pieces line up together, the Hoa Phat story will move from "capacity is ramping well" to "demand and profits are confirming the ramp."