July 7 was not a “buy the whole brokerage sector” session. It was a reminder that the market is starting to price something more specific: which brokers can expand margin capacity soonest.

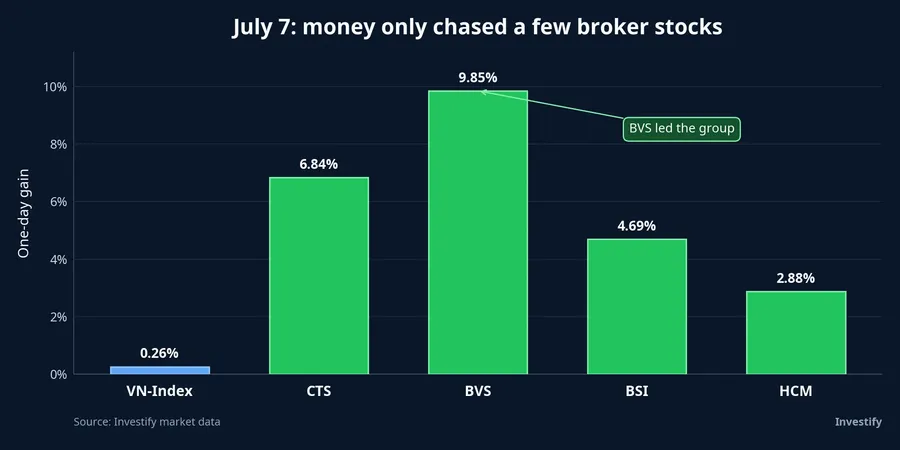

At a quick glance, the tape looked bullish enough. VN-Index closed at 1,848.25, up 0.26%, while CTS gained 6.84%, BVS rose 9.85%, BSI added 4.69%, and HCM climbed 2.88%. But money still did not return evenly across financial services. That matters, because selective strength usually says more than a broad bounce.

For brokerage firms, the balance sheet is not just an accounting backdrop. It determines how much margin lending a company can still extend, how aggressively it can defend client share, and how much operating leverage it can unlock when market turnover improves. In plain English, once margin capacity is nearly full, fresh capital stops being a corporate footnote and becomes a growth input the market can price.

The market is not buying “brokerage stocks” as a block

The standout move in CTS, BVS, BSI, and HCM was not only about one-day performance. The more important point is that all four names sit inside a live narrative around capital plans or ownership restructuring, a theme that was refreshed again in current reporting on July 7.Doanh nhân

That is a different setup from a plain technical rebound. In a purely technical trade, money usually lifts high-beta names more broadly. When it only picks a few stocks, investors need to ask what mechanism is being priced rather than assuming the whole sector is back in favor.

The cleaner interpretation is that the market is screening for balance-sheet capacity. Firms that are approaching the legal ceiling on margin loans, but also have visible plans to raise capital, are easier to pitch as early beneficiaries if trading activity keeps recovering. The money is not just chasing volatility. It is chasing the ability to expand business lines that matter.

Why capital raising hits the sector’s real bottleneck

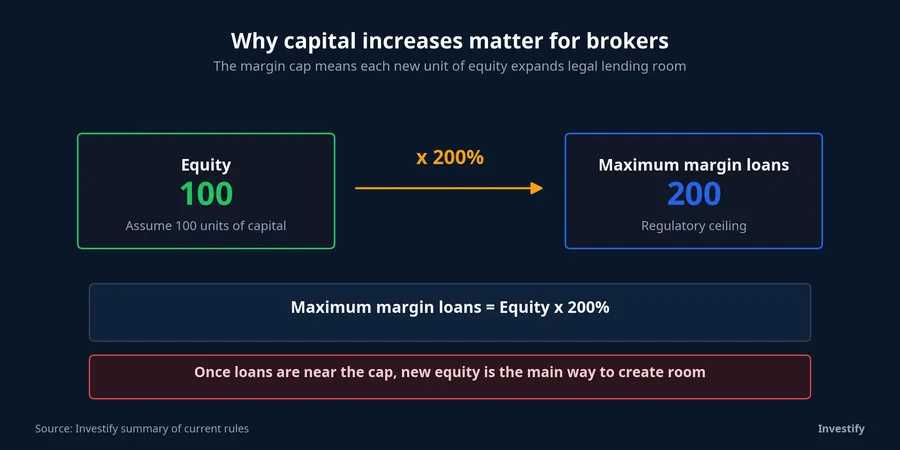

Under current rules, a broker’s margin-loan book is constrained by its equity base. Once that ratio moves close to the ceiling, the company cannot simply decide to lend more. At that point, each new unit of capital becomes the legal foundation for additional margin capacity.Doanh nhân

This matters because it explains why brokerage shares can rally before the next quarter’s earnings are visible. The market does not wait for revenue to be booked. It often reacts earlier, when it sees the pipes for future revenue widening.

That does not mean a capital raise automatically turns into profit. New equity is only the first condition. The company still needs real borrowing demand, healthy market turnover, and disciplined risk management so that a larger loan book does not create a different problem when the tape turns. But if a broker is already near the cap, limited capital can become a competitive handicap before any benefit from a stronger market fully arrives.

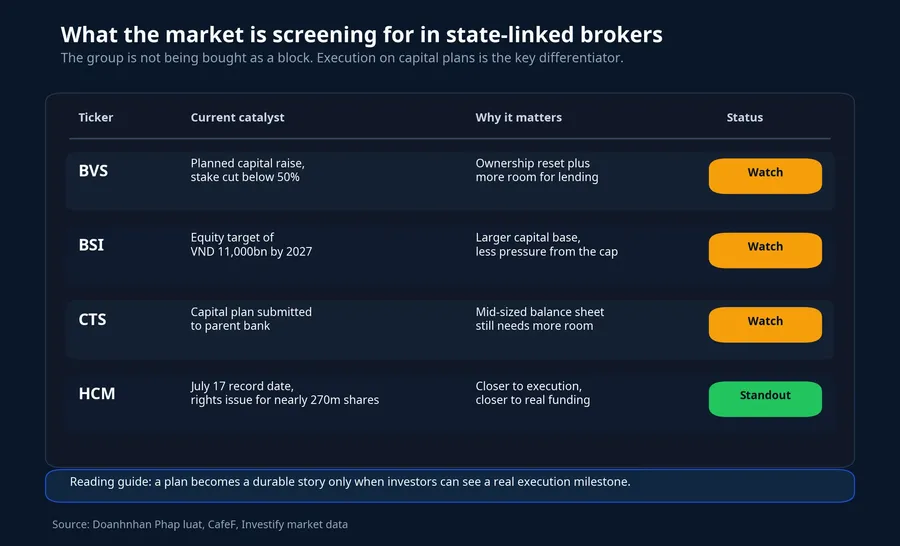

Four names, four different distances from real funding

The market is not treating every capital story the same way. The key distinction is how close each company is to actual execution.

HCM is the clearest case. HSC will finalize its shareholder list on July 17 for a 4% cash dividend and a rights issue for nearly 270 million shares at VND 10,000 each. If completed, the company expects to raise almost VND 2,700 billion, lifting charter capital from nearly VND 10,808 billion to nearly VND 13,508 billion.CafeF

Why does HCM stand out more easily? Not because its plan is guaranteed to work better than everyone else’s, but because the market can already see a timetable. A record date, an offering price, and an expected funding amount make the story less abstract. For investors, that is a major difference between a promise and a process already moving toward cash.

BSI is a different kind of setup. The current roadmap being discussed is to lift equity to VND 11,000 billion by 2027, with management framing the need for a larger capital base as a competitive requirement rather than an optional expansion project.Doanh nhân What the market is testing here is not an immediate issuance date, but whether BSI can scale out of its current capital constraints fast enough.

CTS and BVS sit on the same axis, but in a “watch” state rather than a “confirmed” one. For CTS, the story is that a capital plan has been submitted to its parent bank for consideration. For BVS, investors are watching two layers at once: a possible capital increase and a potential reduction in Bao Viet’s ownership to below 50%.Doanh nhân

That distinction is worth keeping straight. HCM is closer to execution. BSI has a clearer scale-up narrative. CTS and BVS still need more confirmation. When several stocks rally on the same day while their underlying catalysts sit at different stages, the right approach is to separate the stories instead of labeling it a simple brokerage-sector move.

Is the rally only about capital plans

Not necessarily, and this is where investors should stay disciplined. The July 7 move may also reflect a technical rebound after a pullback, short-term position covering, or renewed confidence that VN-Index can hold support well enough to pull money back into turnover-sensitive names.

In other words, a price jump that happens alongside capital-raising headlines does not prove that capital plans were the only cause. What the current evidence supports more confidently is that the theme is acting as a stock-selection filter. The exact mix between technical trading and fundamental repricing still needs more sessions to become clear.

That is why new investors should not read one strong day as proof that profit growth is about to surge immediately. Markets move ahead of the numbers, but they also move ahead of reality when expectations outrun execution. If a capital plan stalls, if participation is weak, or if broader market turnover fails to justify a larger margin book, the gap between narrative and results can show up quickly.

The practical read for the next few sessions

The strongest thesis here is straightforward: the market is starting to re-rate state-linked brokers based on balance-sheet capacity, and the names with capital plans closest to execution have the best chance of holding investor attention.

That edge only lasts if two signal layers keep confirming each other. The first layer is price and liquidity. After a strong session, do CTS, BVS, BSI, and HCM keep attracting money. The second layer is execution. Do capital plans move one step closer to completion, or do they remain at the level of intention. If prices run ahead while capital timelines stand still, the trade can slip from selective re-rating into short-term speculation.

For newer investors, that is the most useful lesson from July 7. The key question is not which brokerage stock posted the strongest gain in one session. It is which company can convert a capital plan into real lending capacity and real revenue over the next few quarters. That distinction makes it easier to avoid the lazy conclusion that “the whole sector is in play.”

The watch list for the next one to two weeks is therefore fairly clear: concrete execution milestones on capital plans, follow-through in liquidity after the initial move, and whether VN-Index remains stable enough for real margin demand to come back. Those three signals will decide whether this is the start of a durable re-rating or just a brief burst of enthusiasm around a story that is directionally right but still future-dated.