After a choppy stretch in equities, many first-time investors tend to reduce the decision to two familiar options: stay in stocks and wait for the next rebound, or retreat to bank deposits for peace of mind. That framing is understandable, but it leaves out a middle layer of capital. Fresh data from Vietnam's government bond market suggests fixed income is being actively priced and traded again, rather than simply parked on institutional balance sheets.

Put simply, when yields rise and trading activity still climbs, that usually means buyers have not disappeared. They are accepting a new price level because the future income stream looks clearer. For retail investors, the key signal is not to rush into bonds. It is to recognize that a portfolio does not have to live only at two extremes.

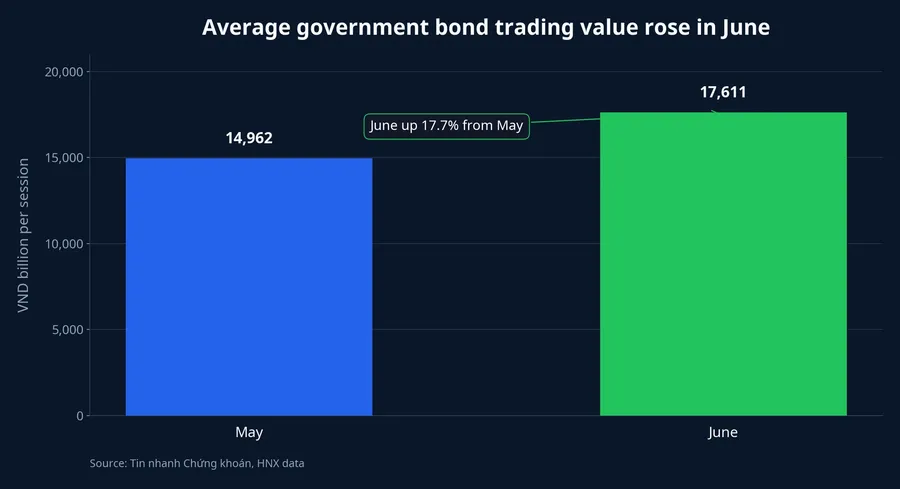

What June says about demand for government bonds

In June 2026, the Hanoi Stock Exchange held 20 government bond auctions for the State Treasury, raising VND 23,375 billion. On the secondary market, average trading value reached VND 17,611 billion per session, up 17.7% from the previous month.Tin nhanh CK The most useful takeaway is not the primary issuance number on its own. It is the fact that secondary-market activity became noticeably more active.

Why does that matter for a new investor? The primary market mostly tells you how much new capital the government raised. The secondary market tells you whether the asset is still being bought and sold, which is another way of asking whether investors still want to own it at current prices. When average session turnover rises by nearly 18%, the cleaner interpretation is that demand for stable-income assets is returning to the conversation.

Another detail supports that reading. Auction yields at the end of June moved higher across multiple maturities. The 3-year tenor cleared at 3.52% a year, the 5-year at 4.18%, the 10-year at 4.35%, the 15-year at 4.40%, and the 30-year at 4.58%, all above the final auction levels seen at the end of May.Tin nhanh CK In plain English, new buyers are now looking at a more visible yield curve, which makes fixed income easier to evaluate.

Higher yields are not automatically a negative signal

Many new investors hear "higher bond yields" and jump straight to "bond prices must be falling, so this must be bad news." That is only half true. For investors who already hold bonds, a higher yield backdrop can pressure secondary-market prices. For investors looking for a new entry point for capital that needs steadier income, however, higher yields mean better compensation for locking up money and accepting product risk.

The more important point is that June does not look like a disorderly move. If yields were rising because the market was under stress, turnover might spike briefly but would usually come with obvious risk aversion. That is not the picture here: yields moved up, average trading value increased, and total listed government bond value at the end of June reached VND 2,715,370 billion, up 0.8% from the previous month.Tin nhanh CK That looks more like an orderly repricing than a panic event.

From a personal-finance perspective, the practical lesson is straightforward. Not every episode of stock-market volatility sends money straight back into bank accounts. Some capital may be searching for an asset layer in between, where yields are visible enough to model but price swings are still milder than in equities. The June data does not prove that all idle cash is shifting this way, but it does show the option is being used at larger scale again.

The Asian backdrop is context, not proof of causation

Vietnam is not operating in isolation. According to Bloomberg data cited by VietnamPlus on July 7, issuers across Asia-Pacific sold USD- and euro-denominated bonds worth USD 154 billion in the second quarter of 2026. Japanese companies accounted for 40% of that volume, while Australia and China contributed about USD 26 billion and USD 20 billion, respectively.VietnamPlus

That does not mean Vietnamese investors should chase offshore bonds, and it certainly does not mean June liquidity in domestic government bonds rose solely because of a regional issuance wave. The discipline here is to avoid turning correlation into causation. What the regional data does offer is background: when stable yields become more attractive, institutions across markets also tend to revisit income-producing assets.

So the careful reading is this. June government bond liquidity in Vietnam reflects domestic demand and local yield levels. The broader Asian bond story does not establish a direct cause, but it helps show that the reappraisal of visible-income assets is not a one-off local quirk.

The comparison makes sense only beside deposits and stocks

If you leave government bonds out of the framework, new investors quickly fall back on a familiar but incomplete question: should I keep stocks or move back to deposits? The better question is what job each slice of capital is supposed to do. Emergency money, medium-term capital that needs a steadier income rhythm, and long-term growth capital should not all be forced into the same role.

On the deposit side, Techcombank's July 7 update shows 12-month online deposit rates across many banks clustered around 5.2% to 7.2% a year, depending on the institution and product conditions. VietnamNet also reported the same day that certain promotional programs could lift rates to 7.35% a year at Techcombank for a 6-month term, 8% at VIB, and 8.9% at Cake, but those are conditional offers rather than the baseline across the banking system.TechcombankVietnamNet

Stocks, meanwhile, remain the growth engine. The VN-Index closed on July 7 at 1,848.25, up 0.26% on the day and about 31.8% above its level a year earlier. Because equities have already delivered a strong 12-month move, it becomes even more important to separate the capital that can tolerate volatility from the capital that needs more consistency. When both goals are pushed into the same equity bucket, new investors usually notice the mismatch only after the market turns unstable.

This is where fixed income earns a clearer role. It should not be treated as a copy of bank deposits. It usually requires more attention to product structure, liquidity is not as simple as breaking a deposit early, and risk is not zero. But it is not a stock substitute either, because the primary objective is not to capture a sharp rerating in market prices. Its natural job is to absorb medium-term capital that wants a more visible income stream while accepting more lock-up and more risk than a deposit account.

What new investors should take away now

The core thesis of this piece is consistent from start to finish: June's data is not a call to dump equities and run into bonds, but it is strong enough to put fixed income back on the radar. Secondary-market government bond liquidity improved, end-June yields moved higher, and the regional backdrop also suggests income-producing assets are being reconsidered more seriously. For first-time investors, that is a reminder that a sturdier portfolio has more than two operating modes.

If this needs to be reduced to one practical sentence, it is this: deposits help you sleep, stocks help your capital grow, and fixed income can add a middle cushion between those two functions. Over the next few weeks, the signals worth watching are whether deposit rates stay elevated, whether government bond yields keep edging higher or cool off, and whether stock volatility remains strong enough to increase demand for steadier income. Put those three variables side by side, and it becomes much easier to see why fixed income is back in the market's conversation.