The headline number was strong enough to move markets immediately. The US economy added only 57,000 nonfarm jobs in June, a figure weak enough to invite quick calls that the Federal Reserve will soon turn softer. But that reading becomes much less clean once you place it next to a 4.2% unemployment rate, which still does not look like a labor market in outright breakdown.BLS

For a retail investor, the cleanest way to read this report is to stop treating it as a one-line verdict. The payroll print weakened. The unemployment rate did not crack higher. The gap between those two signals is exactly why the June report lowered short-term rate pressure without fully validating a Fed pivot.

What the headline misses

According to the Bureau of Labor Statistics, labor force participation fell 0.3 percentage points to 61.5% in June, while the employment-population ratio slipped 0.2 percentage points to 59.0%.BLS That matters because a lower unemployment rate can look better than the underlying reality when fewer people are still counted as part of the labor force.

That does not prove the US economy is already in recession. It does mean the 4.2% unemployment rate cannot be read on its own as a sign that labor conditions remained fully healthy.

The revisions made the report more important, not less. BLS cut April payroll growth to 148,000 from 179,000 and May to 129,000 from 172,000, leaving the prior two months revised down by a combined 74,000 jobs.BLS For the Fed, that is not just one weak month. It suggests the second-quarter labor picture had already been softer than markets thought.

Softer is not the same as broken

A softer labor market is not automatically a recession signal. In June, professional and business services still added 36,000 jobs, social assistance added 25,000, and health care added 22,000. The clearest drop came from leisure and hospitality, where payrolls fell by 61,000 because seasonal hiring was weaker than usual.BLS

That distinction matters. Investors often collapse "cooling" and "breaking" into the same story, especially after a weak payroll headline. The June report supports the first story more than the second: hiring momentum slowed, confidence in labor demand weakened, but the damage still does not look broad-based across the economy.

If you only look at the 57,000 jobs figure, you end up leaning too quickly toward a dovish Fed conclusion. If you only look at 4.2% unemployment, you risk calling the labor market healthy when participation is telling a less reassuring story. Put together, the evidence supports a more measured view: the US economy is cooling, but the Fed still needs more confirmation before it can soften decisively.

What markets actually repriced

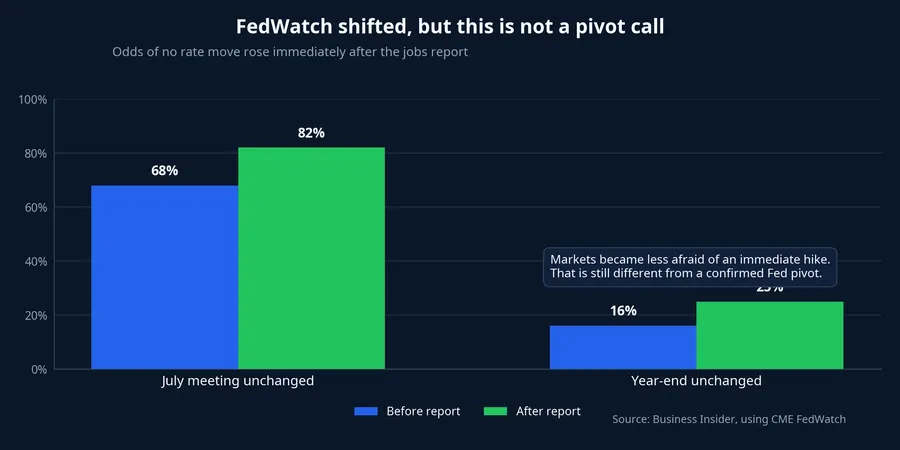

The clearest repricing after the report did not come from the Fed itself. It came from how quickly markets backed away from the idea of an immediate July hike. Business Insider reported that the probability of the Fed leaving rates unchanged at the July meeting rose to 82% from 68% before the jobs data. The probability of no move for the rest of the year also rose to 25% from 16%.Business Insider

In plain English, markets became less afraid of another near-term hike. That is a meaningful shift, but it is still not the same claim as saying the Fed has turned. A higher probability of no move tells you the market sees less immediate pressure. It does not yet prove a full policy pivot.

This is where many fast takes go too far. The dollar softened and gold rallied, so it becomes tempting to label the whole move as a pivot trade. That is still only the first layer of market reaction to weaker-than-expected data. For the story to become more durable, inflation data and short-dated Treasury yields still need to confirm it.

How that signal reaches Vietnam

Internal database figures show the DXY index fell 0.53% on July 3 to 100.80. Spot gold rose 2.27% on July 2 to USD 4,122.76 per ounce, then climbed another 1.16% on July 3 to USD 4,170.51 per ounce. That is a familiar pattern when markets think US real-rate pressure is easing at the margin.

But global signals do not flow into Vietnamese portfolios in a straight line. Internal database figures also show USD/VND at 26,297.50 on July 3, broadly steady versus the prior session. The VN-Index closed the same day at 1,862.08, down 0.23%, suggesting local positioning still has to be read together with domestic liquidity, local FX conditions and how much optimism was already priced in.

This is the point where many newer investors over-simplify. A stronger gold price does not automatically mean Vietnamese equities must fall. A softer dollar does not automatically mean local risk assets get a free boost. The US jobs report mainly shifts the global expectation set. Whether Vietnam can absorb that shift depends on domestic FX stability, local money flow and how stretched valuations already were.

Three signals worth watching this week

The first is the US 2-year Treasury yield. If short-dated yields keep falling over the next few sessions, markets will gain confidence that the June report really did reduce near-term rate pressure. That would usually leave the dollar under more pressure and give gold a better chance of holding its gains.

The second is the next US CPI release on July 14. Business Insider flagged that release as the next key test for the Fed story.Business Insider If labor cools but inflation stays sticky, the Fed still has room to remain cautious rather than pivot quickly.

The third is how USD/VND and the VN-Index behave through the first few sessions of the week. If DXY weakens but USD/VND does not ease with it, the support signal for Vietnamese risk assets becomes less convincing. If gold rises while equities do not sell off much further, that would suggest the domestic market is reading the report more as lower rate pressure than as a fast deterioration in the US economy.

Bottom line: Less pressure, not yet a turn

The most coherent conclusion for now is that the June jobs report reduced short-term pressure for another Fed hike, but did not confirm a policy turn. Softer hiring is real. The downward revisions are real. But unemployment still has not broken higher in a decisive way, and inflation remains the next test that matters.

For a new investor, the useful question is not whether this report was good or bad. It is which branch of the story the market is actually validating. The three signals to watch next are the US 2-year yield, the July 14 CPI release and the behavior of USD/VND alongside the VN-Index. If all three move in the same direction, the Fed story becomes clearer. If they do not, this is still a short-term sigh of relief rather than a final verdict on the US rate cycle.