Starting on July 1, 2026, personal bank transfers in Vietnam move into a more transparent regime. More account and transaction data can be shared with tax authorities, which means investors need more discipline in how they document cash flows.LuatVietnam The wrong reaction is to assume that every payment entering a bank account is now treated as taxable income. That is not what Decree 252 says.

The easier way to read the change is this: the tax system is getting a clearer view of money movement, but tax liability still depends on the economic substance of each payment, the type of transaction, the supporting documents and whether withholding or declaration has already happened elsewhere. The real shift is a higher transparency standard for cash flows, not an automatic tax claim on every incoming transfer.

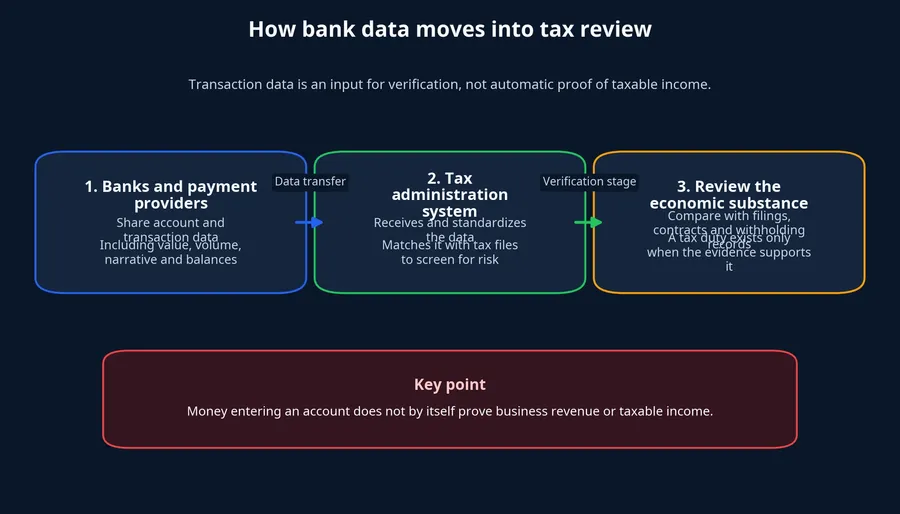

What the new rule actually changes

Under Decree 252/2026/ND-CP, banks and payment service providers must supply additional account and transaction data on taxpayers to tax authorities in electronic form from July 1, 2026.LuatVietnam Account information itself must be reported on a monthly basis no later than the 10th day of the following month.LuatVietnam

The scope goes well beyond a name and an account number. CafeF summarizes the rule as covering transaction volume, transaction value, payment narratives, payer and beneficiary details, domestic and cross-border transfers, account balances, end-period balances and income generated from the account.CafeF

That matters because it changes how retail investors should think about a bank statement. Many people still treat a personal account as a place where everything passes through without much structure: a dividend today, a family transfer tomorrow, stock-sale proceeds a few days later. From here, a bank statement becomes more than a private memory aid. It increasingly functions as part of a financial file that can be reviewed if questions arise.

Transaction data is not the same thing as tax liability

This is the point most likely to be misunderstood. A transfer entering your account tells the authorities that money moved through the account. It does not answer the harder questions: what transaction created the payment, what the economic substance was and where any tax obligation was already handled.

The tax authority may use account data to screen and request explanations. A final conclusion still has to rest on supporting records, documents and context rather than on a number appearing on a statement.

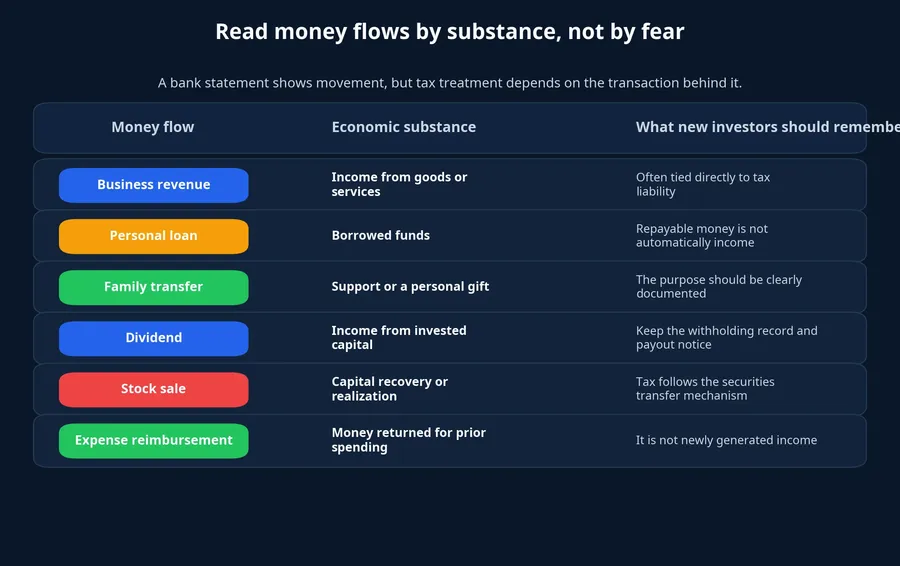

CafeF also highlights the core practical point for retail readers: tax treatment depends on the origin, substance and purpose of the payment.CafeF So the right habit is not to fear every transfer. It is to ask whether each material payment has a clear story behind it.

Think of two transfers worth VND 50 million. One may be repayment of a personal loan. The other may be undeclared business revenue. On the surface they look identical, but their tax treatment is completely different. Without documents, the taxpayer is exposed. With records that fit the timeline and the purpose, the same transfer becomes much easier to explain.

The six money-flow types new investors misread most often

Retail investors often make the same mistake when reading a statement: if money comes in, they mentally classify it as income. That shortcut does not hold up.

First is business revenue. This is the category most naturally tied to tax liability because it is usually linked to the sale of goods or services. If you run a small business, sell online or receive recurring commercial payments, this is the category most likely to draw attention.

Second is borrowed money. A personal loan raises your account balance, but it does not make you richer in the sense of taxable income. It is capital that must be repaid. If an explanation is ever needed, the key evidence is the loan agreement, the timing and a transfer narrative that matches the record.

Third is money from family members. This is common in Vietnam, whether it is living support, a temporary transfer or reimbursement inside a family network. Its substance is very different from business revenue, but the weak point is that many people still use vague descriptions such as “transfer” or shorthand abbreviations. Once the amount is large enough, that vagueness creates unnecessary friction.

Fourth is dividends and other returns on invested capital. Xây Dựng Chính Sách notes that personal income from invested capital is taxed at 5% of taxable income.Chinhphu For investors, the useful records are not just the money arriving in the bank account, but also the payout notice and any withholding certificate.

Fifth is stock-sale proceeds. This is a clean example of why money hitting the bank account is not where the tax story begins. Under the current guidance for personal income tax on securities transfers, the rate is 0.1% of transfer value for each transaction.Chinhphu That means the cash received from a stock sale should be read together with broker statements, execution records and trade confirmations rather than as anonymous income.

The last category is reimbursement of an advance or repayment of money previously spent on behalf of someone else. This appears often for freelancers, informal business groups and people who routinely front expenses for others. It boosts the account balance, but economically it is money coming back, not newly generated income.

What new investors should do now

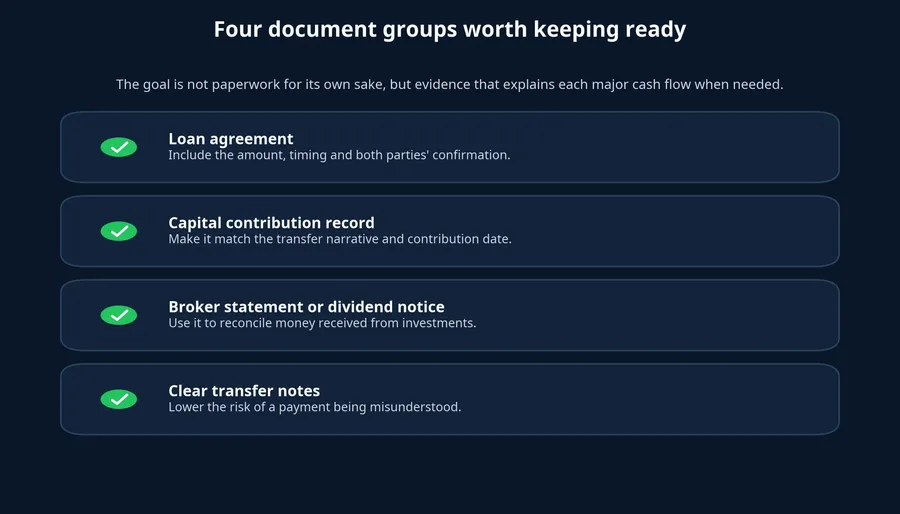

The first step is to treat transfer descriptions as if you were writing accounting notes for your future self. The clearer the description, the lower the risk of confusion. “Loan repayment for July,” “first capital contribution,” “advance reimbursement” and “cash dividend” are all far more useful than a generic “transfer.”

The second step is to organize records by cash-flow type instead of leaving them scattered across email, broker apps and a phone gallery. The practical goal is simple: each large payment should come with a trail that reconstructs what happened. For loans, keep the agreement and repayment schedule. For stock investing, keep broker statements, trade confirmations and transfer records. For dividends, keep the payout notice and withholding documents. For capital contributions, keep the contribution agreement and matching bank evidence.

The third step is to separate accounts once your money flows become more complex. The law does not require every individual to split daily spending, investing and business activity into different accounts in every situation. But if one account receives sales proceeds, family support, dividends and routine living expenses at the same time, you will be the first person to struggle when you need to reconstruct the history.

The fourth step is to stop reading every viral post as if the rule were a machine that taxes all transfers automatically. The new framework raises the transparency bar. It does not remove the need to look at substance. In fact, the more data authorities can compare, the more valuable good records become for taxpayers who want to prove what a payment really was.

Conclusion: do not fear incoming money, fear undocumented money

The central argument here is straightforward: from July 1, 2026, the bigger risk is not that money enters your bank account, but that a meaningful payment arrives with no context, no clear transfer description and no supporting records.LuatVietnam As transparency standards rise, people with disciplined recordkeeping will find the new rule much less threatening than people who still manage money from memory.

The useful thing to monitor over the next few weeks is not the rumor that every transfer is taxable. It is whether your own financial habits are strong enough for a more data-rich tax environment. A clean bank statement is not one with no incoming money. It is one where every major transfer can answer three questions clearly: where it came from, why it came in and how any tax obligation was handled if the law required one.