One of the most common beliefs among new investors sounds perfectly reasonable: if the market is rallying, picking winners should become easier. Screens are greener, positive headlines multiply, and growth stories sound more convincing. But that is often the exact moment when investors confuse a rising market with a higher probability of picking the right stock.

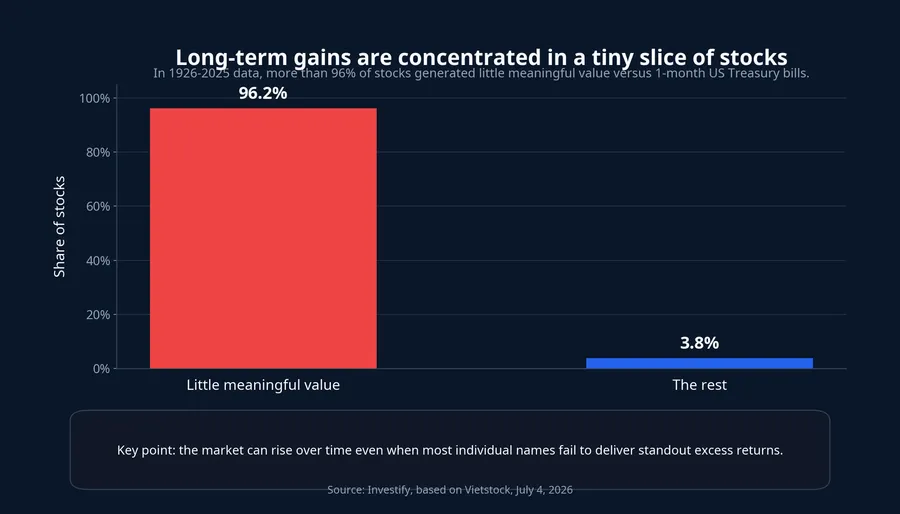

Long-run data from the US market suggests those are not the same thing. A Vietstock article published on July 4, 2026 says more than 96% of US stocks generated little meaningful value relative to 1-month US Treasury bills, even though the US equity market as a whole has remained a powerful wealth-creation engine over time.Vietstock

What the 100-year data is really saying

At first glance, that figure feels counterintuitive. If equities are such a strong long-term asset class, why would most individual stocks fail to deliver meaningful excess value over a safe instrument like Treasury bills? The answer is that market returns are not distributed evenly. The broad market does not rise because every company wins. It rises because a very small group wins by a lot.

The study highlighted by Vietstock was written by Professor of Finance Hendrik Bessembinder of the W. P. Carey School of Business at Arizona State University. According to the article, the dataset spans 1926-2025 and covers nearly 29,000 US stocks.Vietstock The key test is not whether a stock went up at some point. The test is whether it created enough shareholder wealth to outperform the closest risk-free alternative by a meaningful margin.

Put simply, a stock can rise and still be an unimpressive investment if the gain does not compensate for the risk and barely beats a safe benchmark. That distinction matters because new investors often treat “the price increased” and “this was a strong investment” as if they were the same statement.

Once you frame the issue that way, the 96%-plus figure stops looking paradoxical. It simply means most stocks have ordinary life cycles. They attract attention, trade for a period, rise and fall, and eventually contribute very little to the total wealth the market creates for shareholders over time.Vietstock

Why the index can win even when most stocks do not

This is where many first-time investors misread the lesson. When they hear that most stocks do not create meaningful value, they jump to the conclusion that stocks as an asset class must be unattractive. The opposite is closer to the truth. Broad equity markets can still be compelling, but their gains are extremely concentrated in a small set of companies that scale for years, widen margins, and defend their positions over long stretches.

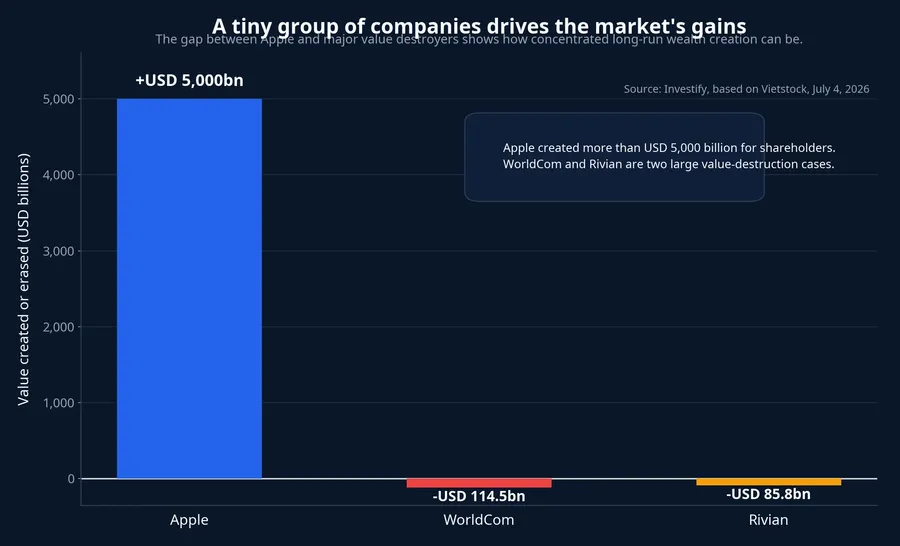

The examples cited by Vietstock make that concentration easy to see. Apple is said to have created more than USD 5,000 billion in shareholder value, equal to roughly 5.5% of all value created by the US market over the same period. By contrast, WorldCom erased about USD 114.5 billion of shareholder wealth, while Rivian destroyed about USD 85.8 billion from its November 2021 IPO through the end of 2025.Vietstock

Those examples show how an index can keep climbing even when many of its components remain mediocre. A tiny number of exceptional companies can create enough wealth to offset a long tail of names that go nowhere, underperform, or disappear. In other words, the market is not a place where everyone wins a little. It is a place where a few companies win big enough to pull the whole aggregate higher.

For investors who own a broad basket, that concentration is actually helpful. You do not need to identify the next Apple at the start. You need enough breadth that when the rare long-term winner appears, your portfolio still owns some of it. If your portfolio holds only a handful of names, the risk is not just buying bad companies. The bigger risk is missing the very small group that ends up driving most of the market's wealth creation.

Bull markets often distort how new investors read probability

When markets rise, every story becomes easier to believe. A company without profits can be framed as a future growth champion. A hot sector can make it seem as if every firm inside that theme deserves to rerate. And a stock that has already rallied can look like proof that the market must be seeing something special.

But the 100-year dataset points investors back to probability. The odds of selecting the small set of true long-run winners do not automatically improve just because the backdrop is favorable. A market rally can lift many stocks in the short run, but it does not turn the average company into a durable wealth compounder. In fact, the moment narratives feel easiest to trust is often the moment entry price becomes the most dangerous variable.

That also helps explain why many people feel as if they are making easy money in a bull phase, only to discover a few quarters later that their personal returns lagged the index badly. They may have joined the right cycle but still missed the names that generated most of the cycle's value. Market excitement and actual portfolio outcomes are related, but they are not the same thing.

A good company is not automatically a good investment

Another common mistake is treating business quality and investment quality as interchangeable. A company can have an appealing product, a strong narrative, or intense media attention and still be a poor investment if the entry price already discounts too much future success. In that case, even a modest reset in expectations can compress the part of market value that was built on optimism.

Rivian is a useful example because this is not simply a story of a bad business leading to a weak stock. Based on the figures cited by Vietstock, the deeper problem was that the market initially placed an extremely rich valuation on the company's future, then had to revise those expectations downward.Vietstock For newer investors, that is a concrete lesson: paying too much for a compelling story can still produce a disappointing result.

That is why rising markets do not really make stock picking easier. They simply make valuation mistakes harder to recognize. When almost everyone around you is telling a bullish story, it becomes easy to mistake pre-priced optimism for genuine upside.

A more realistic portfolio frame for first-time investors

The practical takeaway is not to give up on individual stocks altogether. The more useful takeaway is to be honest about probabilities and build a portfolio that can survive them. If you pick single names, position sizing matters. So does knowing why you bought, and what would prove the original thesis wrong. A portfolio concentrated in a few hot names is not always intentional conviction. Sometimes it is just weak diversification.

For new investors, a more realistic structure is a core-and-satellite approach. The core can sit in broader vehicles such as equity ETFs or mutual funds, where the goal is to capture the market's long-term wealth creation without having to guess every future superstar. The satellite sleeve, if used at all, is where individual stock ideas belong, with tighter rules around entry price, thesis quality, and exit discipline.

The most important lesson from this research is not that stock picking is pointless. It is that the hard part in a rising market is not deciding whether to participate. The hard part is whether your portfolio is actually built to own the rare winners that matter. For first-time investors, the better way to improve the odds is not to believe hot stories more strongly. It is to build a portfolio that is broader, more disciplined, and durable enough to stay in the game.