PC1 was forced to open an early repurchase mechanism for its VND 900 billion bond lot not because VND 90 billion was too large to ignore. The more important point is that the VND 90 billion moved away from the use of proceeds previously disclosed to investors. With equities, investors can live with daily price swings. With bonds, the investment case depends far more on the set of promises embedded in the contract.

Put simply, bondholders do not buy only a coupon. They also buy a package of commitments about where the money will go, what risks come with it, and which cash flows are expected to service the debt. Once part of that money drifts away from the disclosed purpose, the question is no longer whether VND 90 billion is big or small. The real question becomes whether the contract investors thought they owned is still the same contract.

What happened to bond lot PC1H2227002

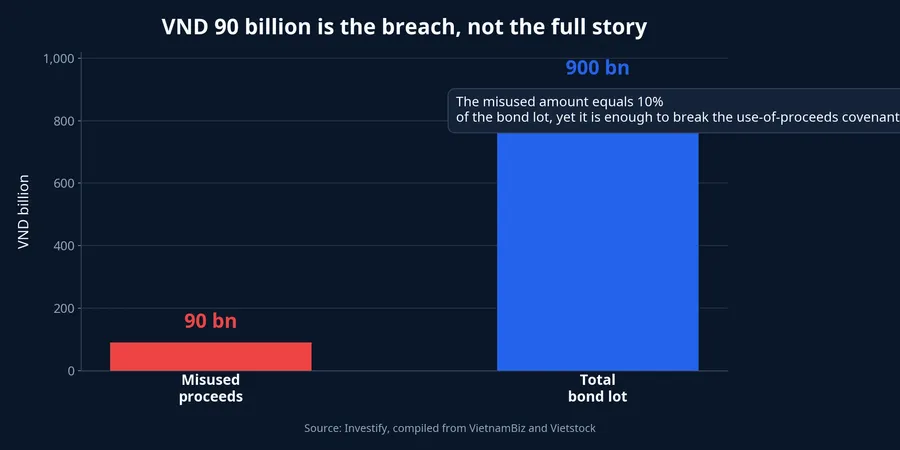

According to VietnamBiz, PC1 said it had received Decision No. 337/QD-KPHQ dated June 23, 2026 from the State Securities Commission of Vietnam. The order, as cited by the outlet, found that PC1 had used VND 90 billion from the private placement of bond lot PC1H2227002 to repay short-term loans at VietinBank instead of using the proceeds for working capital expansion as previously disclosed to investors.VietnamBiz

The VND 90 billion amounts to only 10% of the VND 900 billion bond lot, but that is not a reason to treat it lightly. In corporate bonds, a mismatch in the use of proceeds is not read as a routine spending adjustment. It is read as a sign that the core information investors used to price the risk is no longer intact.VietnamBiz

Newer investors often react by saying that PC1 still used the remaining VND 810 billion as planned, so why should the market make a big issue out of this. But a bond does not work like a savings deposit. In a deposit, the saver mostly looks at the bank's credibility and the posted rate. In a private bond, the buyer has to rely on the specific covenant package of that deal, and the use of proceeds is part of that package.

Why VND 90 billion is enough to change the whole case

The simplest way to think about it is this: if a company tells investors the money will be used for purpose A, investors are pricing the risk of purpose A. They are implicitly judging the expected cash generation, the payback period, the collateral support and the issuer's resilience under stress. When part of the money is redirected to purpose B, investors are suddenly exposed to a different risk profile they may never have agreed to in the first place.

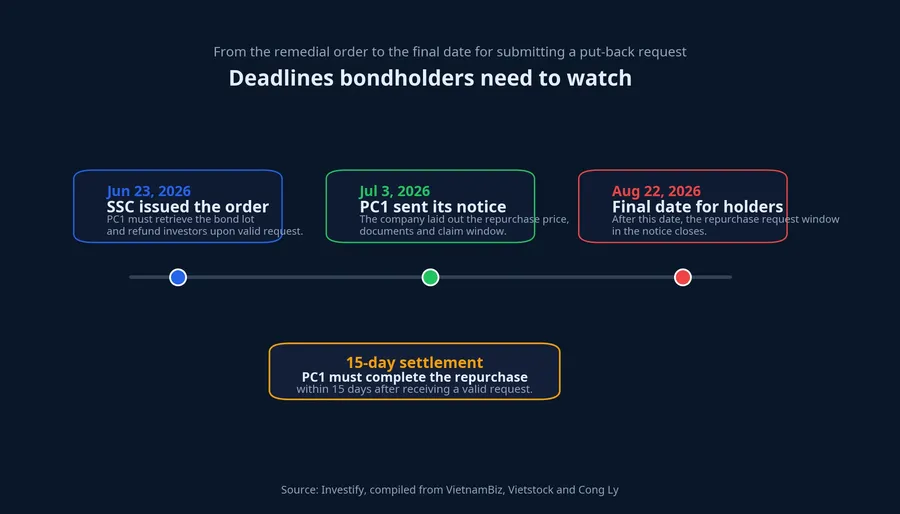

That is why the remedy in PC1's case goes beyond a simple administrative penalty. VietnamBiz reported that the company was required to retrieve the securities that had been offered and issued, and refund investors or depositors together with the relevant interest accrual within 15 days after receiving a valid request from investors.VietnamBiz

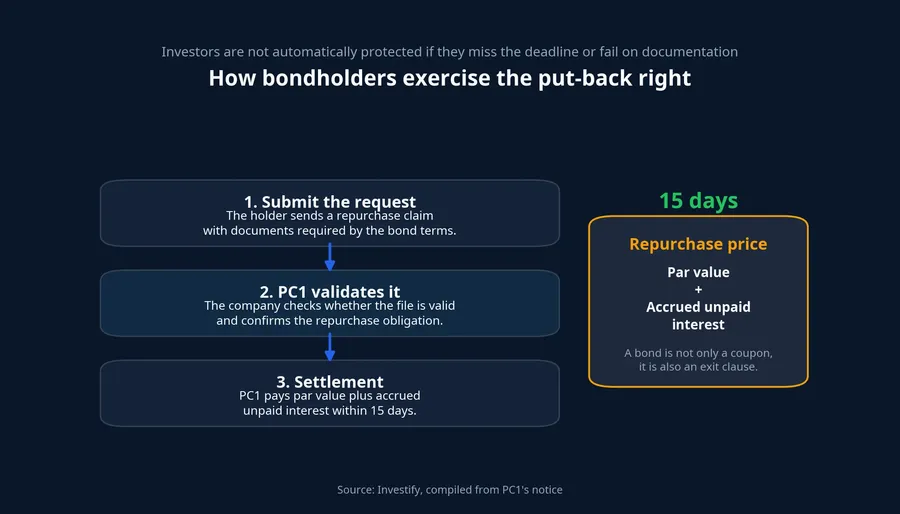

Vietstock said bondholders have up to 60 days to submit a request, and that August 22, 2026 is the final date for PC1 to receive repurchase claims.Vietstock A notice cited by Công lý also stated that the repurchase price for each bond consists of par value plus unpaid accrued interest from the latest coupon payment date to the day before repurchase, based on the bond's stated interest rate.Công lý

This is exactly where many first-time investors miss the real issue. Investor protection exists, but it does not operate automatically on behalf of the holder. If bondholders fail to read the notice, miss the submission deadline or cannot provide a valid file, a right that exists on paper may never turn into cash in the account. Bonds therefore demand much more active follow-through than many retail investors assume.

Which clauses retail investors usually overlook

Bond lot PC1H2227002 was issued in 2022 with a total value of VND 900 billion, a 5-year tenor and a maturity date of May 19, 2027. Each bond carries a par value of VND 100 million.Vietstock On the surface, these are the details most people look at first. But the more important parts are the early repurchase right, the collateral package and the trigger conditions attached to those rights.

According to Vietstock, the issuance plan allows bondholders to require PC1 to buy back the bonds early at specific milestones. The cumulative repurchase amount can reach VND 270 billion at the 24-month mark, VND 450 billion at 36 months and VND 630 billion at 48 months from the issuance date.Vietstock Those numbers show that the put-back right is not a footnote. It is part of the exit structure in a market where private bond liquidity is far thinner than listed equities.

There is also the collateral layer. Vietstock reported that at the end of 2025, PC1 disclosed changes related to collateral for several bond lots, and for the VND 900 billion lot it added more than 17.4 million shares of Trung Thu Hydropower JSC valued at more than VND 409 billion.Vietstock Collateral does not make a bond automatically safe, but it tells holders what extra layer of protection may still exist if debt-servicing cash flow weakens.

That affects an investor's money in a very direct way. If you only look at the stated yield, it is easy to miss whether the issuer can change the use of proceeds, what disclosure duties it has, who represents bondholders and when the holder is allowed to trigger the repurchase right. Once stress appears, the investor who has read the contract and the investor who remembers only the coupon are standing in very different places.

Why the lesson matters beyond PC1

Vietnam's corporate bond market has moved well past the stage when many retail buyers treated bonds as little more than higher-yield deposits. After the market's major disruptions, the lesson is not that investors should fear every corporate bond. The lesson is that a bond must be read as a credit contract with conditions attached. PC1's case makes that point clearly: a small deviation in percentage terms can still carry large consequences for legal rights and investor protection.

The notice cited by Công lý said that if investors do not submit repurchase requests within the stated period, the bonds will continue to be performed under the previously disclosed terms and conditions.Công lý That detail matters because it shows that investor rights are not triggered automatically just because a violation occurred. Bondholders still need to act through the right process if they want the legal right to become a practical result.

That is why the real lesson from the VND 90 billion figure is not about whether the amount looks small or large inside a VND 900 billion deal. The lesson is about the order of priorities when reading a fixed-income investment: the coupon is the easiest part to notice, while the use-of-proceeds covenant, bondholder rights and disclosure discipline are the parts that determine whether you own a clear contract or a risk you never fully read. The next signals to watch are also specific: whether bondholders file requests on time, whether PC1 completes each repurchase within the 15-day window after a valid claim, and how the market will treat investor-protection clauses in similar bond deals from here.