Nearly VND 830 trillion is estimated to have flowed back into Vietnam's banking system in the first half of 2026. For many first-time investors, that sounds like a simple signal: cash is returning to banks, so deposit rates should soon come down. But that is not how the system is actually being tested. The real question is whether incoming deposits are rising fast enough to catch up with credit growth.CafeF

Put simply, a bank also has to balance its input and output. Its input is deposits and other funding sources. Its output is lending. If lending still expands faster than funding, the system cannot relax yet, even if the headline number on returning deposits looks large.

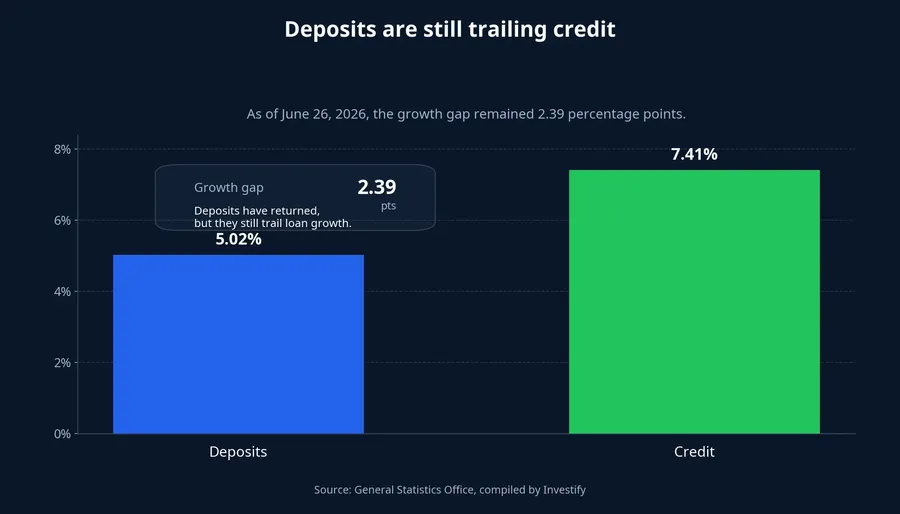

Deposits are back, but not enough to ease the pressure

CafeF, citing Vietnam's General Statistics Office, said that as of June 26, 2026, deposit mobilization at credit institutions was up 5.02% from the end of last year, while credit growth reached 7.41%. That 2.39 percentage point gap is the core detail in this story, because it shows that deposits are rising but still not keeping pace with lending into the economy.CafeF

Seen that way, the nearly VND 830 trillion figure is not proof that funding stress has disappeared. It only shows that banks are pulling in more money. Whether system liquidity is actually easing depends on the relative speed of deposits and credit, not on one large headline number in isolation.

CafeF also reported that by June 29, 2026, total outstanding credit in the banking system had reached VND 20,030 trillion, up 7.73% from the end of 2025. In plain language, credit kept running even after the June 26 checkpoint. That is exactly why deposit rates are unlikely to fall quickly just because deposits improved in the first half.CafeF

Why savers are moving back to banks

Part of the answer is visible in the rates now being offered. VietnamNet reported on July 3 that SeABank was offering up to 8.55% a year and Cake by VPBank up to 8.9% a year at selected tenors. The same report said an unnamed bank was paying as much as 9.2% a year for 12-month online deposits from VND 100 million, while some 6-month tenors were also reaching 9% a year.VietnamNet

For new investors, yields like that are enough to change behavior. When a low-volatility asset can deliver a visible return right away, many people will delay putting money into stocks, mutual funds, or corporate bonds. That is not an emotional reaction. It is a practical comparison between potential reward and the amount of risk required.

This matters for portfolios because higher deposit rates do more than attract idle cash. They also create a meaningful alternative yield for the wider asset market. When banks pay enough, riskier assets need a stronger earnings story, a more compelling valuation case, or a clearer catalyst to win that money back.

The easy mistake in reading the VND 830 trillion number

The common mistake is to look at the scale of returning money and conclude that system liquidity must already be comfortable. In reality, a large number says little if credit is still expanding faster. A bank is not truly free of funding pressure until new money arrives both fast enough and steadily enough to finance fresh lending without paying up for capital.

If that condition is not met, banks keep looking for ways to retain funding. The most visible route is higher posted deposit rates or targeted promotions. The less visible route is adding extra yield for balance size, tenor, or online placement. That is why a slightly lower posted board rate does not automatically mean the real cost of funding has fallen.

CafeF said that on April 9, 2026, the State Bank of Vietnam met with commercial banks and asked them to lower rates on new deposits with tenors from six months onward. Then on May 14, 2026, the central bank issued Official Letter 3972/NHNN-CSTT to inspect how credit institutions were implementing the policy of lowering deposit-rate levels.CafeF

But market mechanics are still market mechanics. If credit keeps outpacing deposits, the pressure to retain funding will simply reappear in another form. So the right question is not whether banks want to lower rates. The right question is whether they have enough room to do so quickly.

Two practical scenarios for the second half

The first scenario is that the gap between deposits and credit remains wide. If upcoming monthly reports still show deposits growing more slowly than lending, deposit rates will be hard to bring down quickly across the board. In that case, quiet promotions, conditional top-ups, and a wider spread between smaller banks and large banks will likely remain in place.

That scenario does not mean money will abandon the stock market altogether. It does mean capital becomes more selective. Equities will need clearer proof on earnings, valuation, or company-specific catalysts. New investors often miss this and focus only on the broad market index. In reality, when savings products become more attractive, the market often responds with sharper internal divergence rather than a single wave of outflows.

The second scenario is that deposits gradually catch up with credit in the third and fourth quarters. If that happens, the rate environment could flatten first and then start easing at the most competitive tenors. That would be the point at which the risk appetite of idle cash holders has a real reason to shift, because the reward for staying in bank deposits would no longer stand so far above expectations in other assets.

The key discipline is not to turn one big first-half number into a certain second-half conclusion. Deposits returning is a real signal. But for now it only shows that banks are doing a better job attracting funding, not that the funding squeeze has already been resolved.

What first-time investors should watch next

The first signal is the gap between deposit growth and credit growth. Those two numbers must be read together. If deposits rise strongly but credit rises even faster, the pressure is still there. Only when that gap narrows more consistently over several reporting periods does the case for faster rate cuts become more credible.

The second signal is the real rate savers can actually receive, not just the posted board rate. If the board comes down but online offers, new-customer deals, or large-ticket placements still pay up, competition for funding has not disappeared. For first-time investors, that distinction matters because it determines whether the alternative yield outside the market has genuinely fallen.

The third signal is how money behaves when it returns to risk assets. As long as savings still pay high yields, flows into equities usually become more selective and more demanding. If rates start easing and money still does not come back forcefully, that suggests the market's problem is no longer just rates. It is also about earnings expectations and valuation.

The clearest thesis right now is this: deposits are back, but as long as credit keeps growing faster than funding, deposit rates will remain difficult to lower quickly. That thesis only changes if the next reports show a meaningful narrowing of the deposit-credit gap and actual offered rates fall at the same time. Until those two signals arrive together, it is still too early to read this banking story as "cash has returned, so rates are about to drop sharply."