A fixed 12% annual coupon is exactly the kind of number that makes new investors pause. Set against the bank deposit board that CafeF updated on July 3, the instinctive reaction is to focus on the spread and assume the deal must be attractive.CafeF

That is the wrong starting point for corporate bonds. In this market, coupon is not a gift. It is the price an issuer has to pay to convince someone else to carry its risk. The higher the coupon, the less useful the first question becomes, “How much do I earn,” and the more useful the next one becomes, “Why does the issuer need to pay this much.”

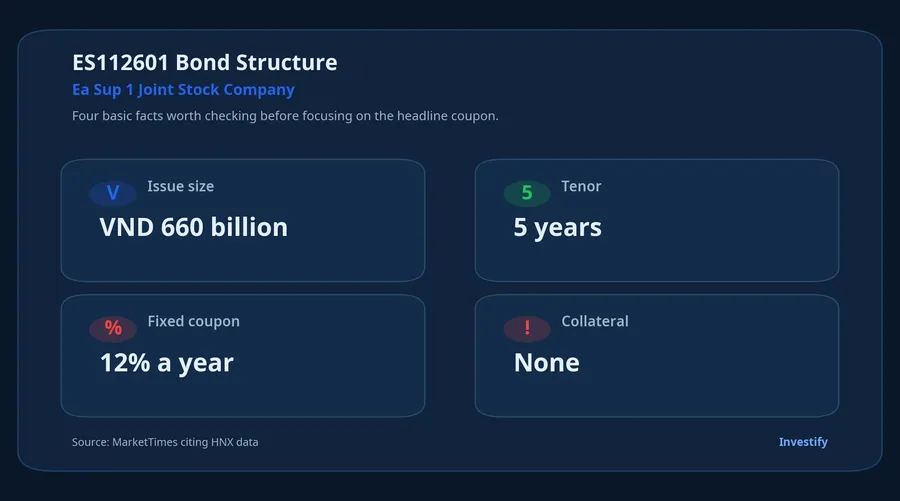

Ea Sup 1’s ES112601 issue is a clean example of that logic. MarketTimes, citing HNX data, reported that the company completed a VND 660 billion issue with a five-year tenor, an issuance date of June 22, 2026, completion on June 25, 2026, and a scheduled maturity on June 22, 2031. The coupon is fixed at 12% a year for the life of the bond.MarketTimes

Read the structure before the headline yield

The key detail is not the number itself but the terms wrapped around it. The same MarketTimes report says ES112601 is non-convertible, carries no warrants, and has no collateral. For a first-time reader, “no collateral” matters more than “12%,” because it speaks directly to what stands behind the promise if the plan stops working.MarketTimes

In plain English, bondholders are relying primarily on the issuer’s future cash flow and execution capacity rather than on a pledged asset that can be enforced first. If the company performs as planned, coupons and principal can still be paid on schedule. If cash flow slows, holders do not have a ring-fenced piece of collateral already sitting there for recovery.

That does not automatically make the bond bad. Unsecured bonds can still be rational purchases for investors who understand the issuer, the project, and the trade-off they are accepting. The problem for newcomers is that a 12% label can dominate attention while the more important clues sit in the fine print.

Why would a solar issuer still pay 12%

This is where discipline matters. The source article does not prove a single cause for the 12% coupon, so it would be a stretch to say the company is paying up because it is in distress. A more defensible reading is that several explanations can coexist.

The first is project finance itself. Solar assets are tangible and revenue-generating, but they are also capital-intensive and slow to pay back. A five-year funding package should price above bank deposits because investors are locking up money for longer and taking project risk rather than bank balance-sheet risk.

The second is the bond’s legal structure. Two issuers with the same project profile can still pay different coupons depending on whether the debt is secured. Remove collateral and investors usually ask for a higher risk premium because one layer of protection disappears.

The third is disclosure quality. MarketTimes said the State Securities Commission’s inspectorate fined Ea Sup 1 VND 92.5 million on March 27, 2026 for breaching bond-related disclosure obligations. That fine is not proof of repayment trouble, but it is a fact that can reasonably push investors to demand more compensation for uncertainty.MarketTimes

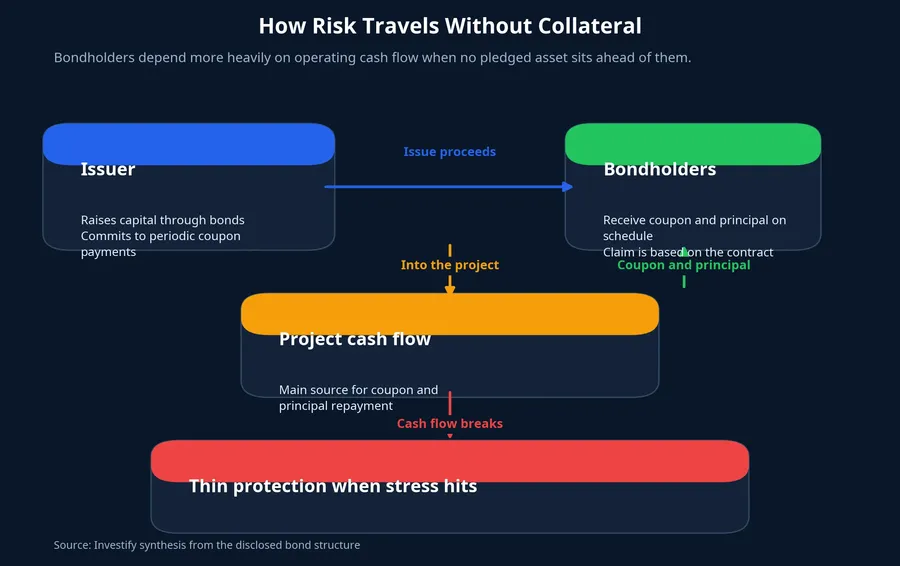

How the risk actually travels

This is the part retail readers often miss. Corporate bond risk does not show up like an equity screen flashing red. It usually travels more quietly, moving from issuance terms to project cash flow and only then to coupon service and principal repayment.

The mechanism is straightforward. Bondholders provide capital to the issuer, the issuer deploys that capital into the project or its funding needs, and repayment ultimately depends on future cash generation. Once that chain weakens, the problem is not just lower-than-expected return. It becomes a recovery problem.

That is why “no collateral” is not a technical footnote. It tells you that if stress appears, the recovery path can be slower, harder, and more dependent on negotiation or legal process. The fewer protection layers there are, the more coupon investors typically need to justify the exposure.

Why this is not the same as a bank deposit

Many first-time investors see 12% and compare it directly with a savings rate. The comparison is understandable, but it is incomplete because the two products do not sit on the same risk tier. A bank deposit is a liability of the bank inside a tightly supervised framework, with deposit insurance up to the statutory limit. A corporate bond is much closer to lending directly to a company and bearing the consequences of that choice.

That means the spread over deposits is not free carry. It is compensation for risks that depositors do not take in the same way: operating cash-flow risk, disclosure risk, collateral risk, and liquidity risk if an investor wants to exit early. In Vietnam’s private-placement market, the gap is even more important because these deals are mainly designed for professional investors with the capacity to read much deeper into an issuance file than a new retail buyer can.

That is also why “successfully issued” should not be confused with “safe.” A completed sale only proves that a group of investors accepted that trade-off. It does not mean every other investor should read the same structure through the same lens.

The lesson for new investors

The main takeaway from ES112601 is not about solar power specifically, and it is not really about Ea Sup 1 as a name. It is about how the capital market prices risk through several layers at once: coupon level, bond terms, disclosure quality, and confidence in repayment cash flow. If a newcomer looks only at the coupon, the entire deal can be misread.

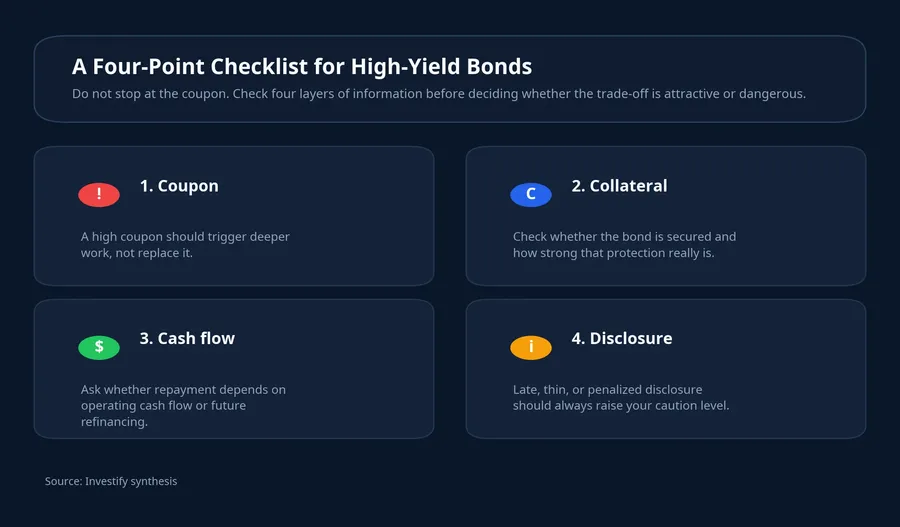

For new investors, a short checklist is usually more useful than a pile of jargon. First, treat the coupon as the opening signal for deeper work, not the conclusion. Second, check whether the bond is secured and, if so, what actually sits behind it. Third, ask which cash flow is expected to repay the debt. Finally, do not dismiss disclosure history, because the VND 92.5 million fine in this case shows that transparency is not a side note in the file.MarketTimes

The thesis here is simple and should stay simple: in Ea Sup 1’s case, a 12% annual coupon reads first as the market price of credit risk, not as proof of an unusually good investment. That conclusion only changes if later disclosures show meaningfully stronger repayment cash flow, asset quality, and transparency than the market can see today. For now, the right thing to watch is not how high the coupon looks, but what protection really stands behind it.