On July 3, the VN-Index fell 4.27 points to 1,862.08, while HVN rose 6.53% to VND 25,300 a share and VJC added 2.01% to VND 141,800.VietnamPlus A quick read of the tape would suggest that airline stocks simply looked stronger than the market. A better read is that investors are paying ahead for a narrower fuel bill at the peak of the travel season.

For first-time investors, the easy mistake is to look only at passenger traffic. Airline earnings do not move in a straight line with the number of seats sold. They are shaped just as much by fuel, exchange rates, aircraft leases, maintenance costs and fare competition. When airline shares rise on a day when the broader market closes lower, the market is usually repricing a future margin scenario rather than reacting to the passenger count of that session.

Why the market is focused on the fuel bill

Tuổi Trẻ reported that HVN was the biggest positive contributor to the VN-Index on July 3, with trading volume of roughly 3.2 million shares, almost three times its one-month average.Tuổi Trẻ Internal data points the same way: HVN traded 3,216,800 shares, far above 886,500 on July 2 and 1,114,500 on July 1. That is not a thin squeeze. It is real money entering the name.

The mechanism matters. A full aircraft does not automatically translate into a better margin if fuel, leasing costs and currency pressure all move the wrong way. The reverse is also true. If fuel prices soften while load factors remain healthy, the same volume of passengers can leave behind a much better profit pool.

Vietnam Airlines had earlier estimated its average Jet A1 price for 2026 at USD 128.54 per barrel, up nearly 48% from 2025. On that assumption alone, the airline expected about VND 11,900 billion in additional fuel costs versus the previous year.VietnamPlus That figure makes the logic easy to grasp. If the input cost rises, stronger revenue can still be absorbed. If the input cost eases, the market has a reason to re-rate margins before the next quarterly report lands.

Brent is cooling, but that is only the first condition

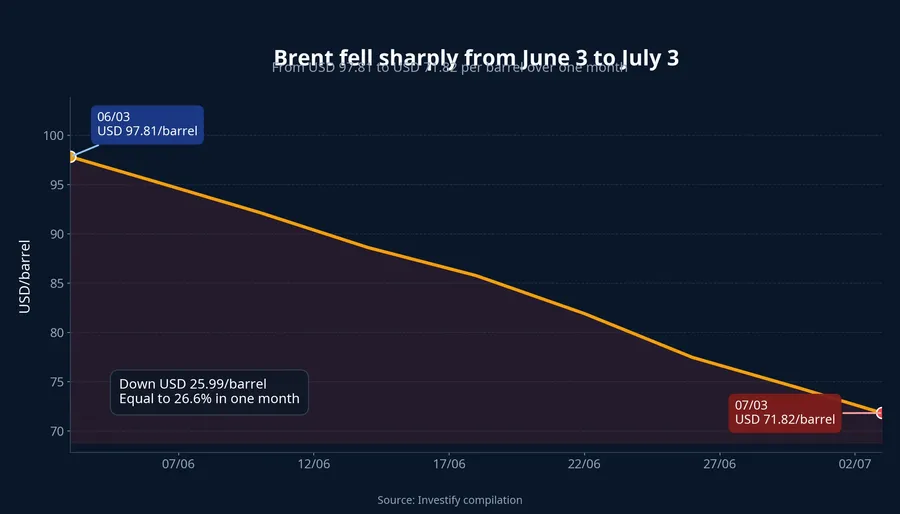

Internal data shows Brent fell from USD 97.81 per barrel on June 3 to USD 71.82 on July 3, a decline of about 26.6%. VietnamPlus also reported that after the Strait of Hormuz reopened and the US and Iran reached a ceasefire agreement in June, jet fuel prices moved down to around USD 112-115 per barrel.VietnamPlus That shift alone is enough to make investors think about a less compressed second half for airline operators.

Still, there is an important difference between “fuel is falling now” and “the quarter’s cost base has already improved.” Earnings are built on average costs over weeks and months, not on a handful of softer sessions. If Brent only pauses and then turns back up, the expectations already built into airline share prices will be tested quickly.

That is where new investors often get ahead of themselves. They see a friendlier input backdrop, they see the stock move, and they jump to the conclusion that better profits are now locked in. The cleaner way to frame it is this: the share price is reacting to the probability of margin improvement, not to a result that has already been delivered.

Travel demand is the second condition

The other side of the equation is revenue quality. If fuel eases but fare competition intensifies, part of the cost relief can be given back through discounts. For the current thesis to hold, the market needs another confirming variable: demand, especially international demand, has to stay strong enough for airlines to preserve revenue per seat.

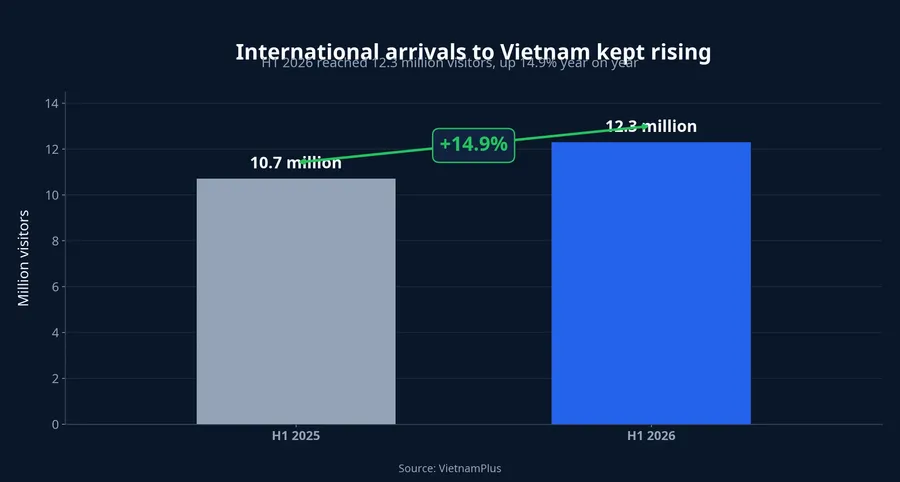

The recent numbers are supportive. Vietnam welcomed about 12.3 million international visitors in the first six months of 2026, up 14.9% year on year, while domestic trips reached about 81 million. Tourism revenue was estimated at roughly VND 569,000 billion.VietnamPlus For airlines, international routes matter disproportionately because they tend to carry stronger margins and richer ancillary revenue.

First-quarter results also explain why the market is not ignoring this setup. Citing an Agriseco research note, Tuổi Trẻ said Vietnam Airlines posted nearly VND 36,900 billion in first-quarter 2026 revenue, up 21% year on year. Profit attributable to the parent company came in at nearly VND 4,400 billion, up 29%. Passenger volume reached 6.7 million, up 14.6%, while international passengers totaled about 2.5 million, up 22%.Tuổi Trẻ

For retail readers, the picture has two layers. The first is that traffic recovery is already visible. The second is that if fuel costs decline at the same time, margins can expand rather than merely survive. That is why airline shares can be more sensitive to oil than many investors assume when they reduce the story to summer travel alone.

Not every travel stock belongs in the same basket

One useful discipline is not to treat every “travel” name as if it benefits through the same channel. HVN and VJC are more direct beneficiaries because fuel feeds straight into operating costs. Hotels, resorts and tour operators gain more indirectly, through visitor flow, spending power and length of stay.

That distinction matters when price action looks similar on the screen. VNG, a tourism stock linked to Thành Thành Công, rose 4.68% to VND 6,490 on July 3, but internal data shows only 200 shares changed hands. A move on extremely thin volume does not carry the same information value as HVN’s rally, where millions of shares traded. New investors often see two green candles and assume they signal the same thing. In reality, liquidity usually tells the more important part of the story.

The other discipline is not to force a single explanation onto HVN or VJC. Cheaper fuel is the strongest driver supported by the current evidence, but it is not necessarily the only one. Short-term trading flows, positioning around the summer season or expectations for second-quarter earnings could also be part of the move. The evidence is not strong enough to assign exact weights to each factor, so the honest reading is that lower fuel prices are strengthening the thesis, while the size of the market’s advance pricing still needs more data.

What to watch over the next few weeks

The monitoring list is fairly simple. First, Brent and Jet A1 need to hold at a lower range. If oil only pauses and then turns higher again, the margin story weakens at its source.

Second, investors need to watch international passenger data, load factors and airlines’ ability to hold ticket prices through the peak season. The real question is not whether more people are flying in the abstract. The real question is whether carriers can protect revenue per flight while their key input cost becomes less punitive.

Third, the quality of the flow on each stock matters. A rally backed by large turnover, as in HVN’s case, says the market is willing to position early for a better earnings setup. A rally on a few hundred shares says price moved, but it does not yet prove that serious money is choosing the theme.

The clean conclusion is that the current airline outperformance has a more defensible foundation than a simple summer-travel headline. The most credible thesis is that investors are discounting an improvement in profit margins if fuel stays lower for long enough while travel demand remains firm. The main risks to monitor are a rebound in oil or fare competition eating into the cost relief, but at this stage those are tests of the thesis, not reasons to dismiss it.