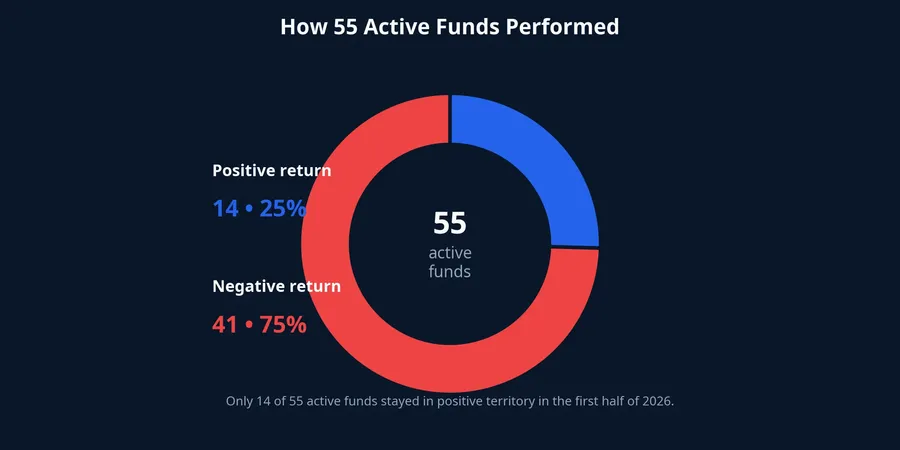

There is an easy trap for new investors in the first half of 2026: the headline index went up, but most active equity funds did not keep pace. The VN-Index rose 4.2%, yet only 1 of the 55 active funds tracked in the report managed to beat it.Người Quan Sát On the surface, that sounds like a straightforward indictment of active management. The closer read is different. This was less a story of managers staying on the sidelines and more a story of a market that rose in a very hard-to-beat way.

Put simply, an index can be green even when much of the market is not. If gains are carried by a narrow group of heavyweights, an active fund can own plenty of solid stocks and still lag the benchmark if it does not own enough of the names doing the index-level lifting. That is why the right takeaway is not “active funds are worse than ETFs.” The real question for investors is what benchmark they are using and what, exactly, they are paying a fee for.

A Rising Index Does Not Tell the Whole Story

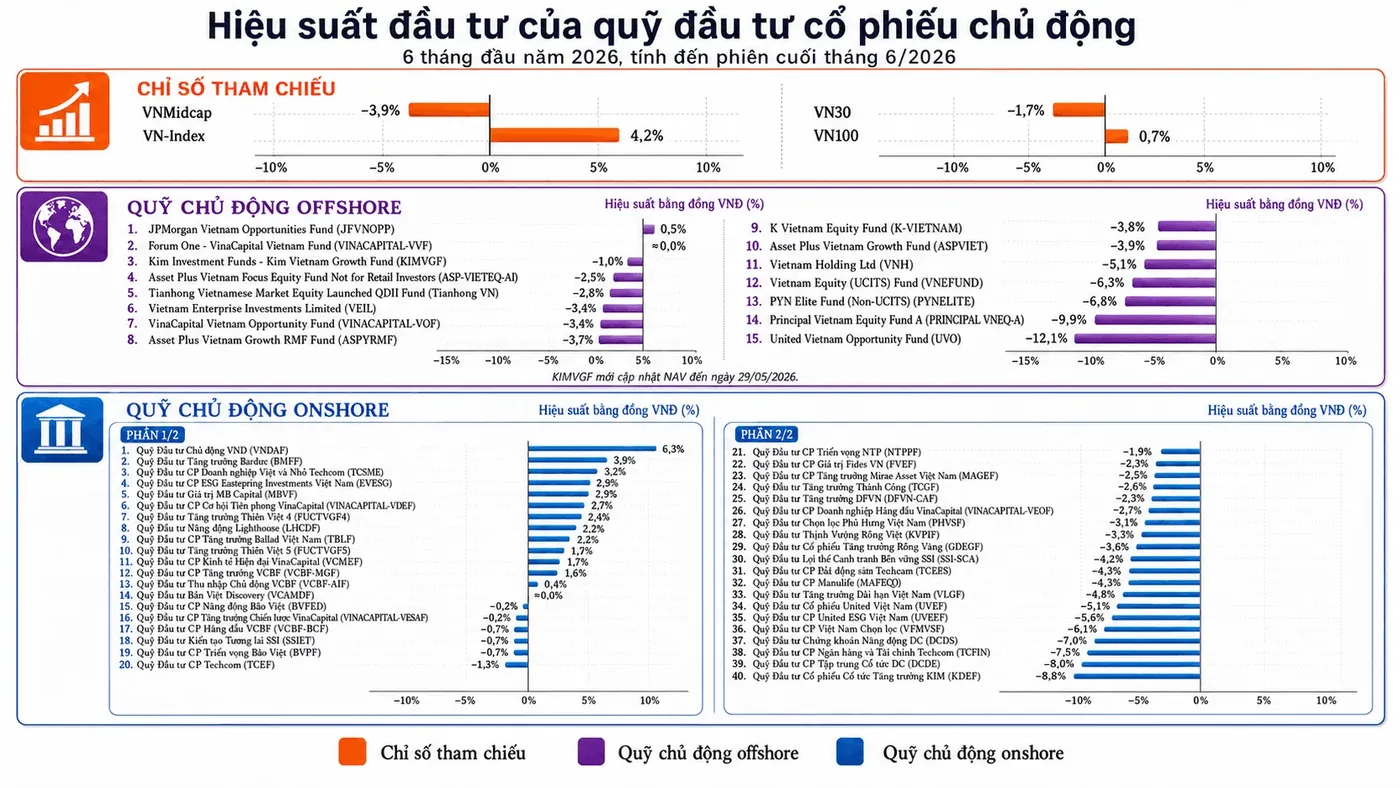

The VN-Index ended 2025 at 1,784.49 points and stood at 1,860.01 points on June 30, 2026, a gain of 4.2%.Người Quan Sát For a new investor, the instinctive conclusion is simple: if the market is up, stock funds should be up as well, and ideally by more. Markets are rarely that clean.

Market breadth tells the deeper story. Over the same period, VN30 fell 1.7%, VN100 rose only 0.7%, and VNMidcap declined 3.9%.Người Quan Sát That tells us the VN-Index gain was not broadly shared. The headline number was supported by a concentrated set of large-cap stocks, while wider parts of the market moved sideways or lower.

That distinction matters. “The market went up” is not the same thing as “most stocks went up.” In a broad rally, active managers have more ways to keep up or outperform. In a narrow rally, funds that miss the index-driving pocket are likely to lag, even if they are fully invested and even if their stock selection is defensible on its own terms.

For newer investors, this is where benchmark confusion usually begins. The index is the market’s front window. Breadth is the foundation behind it. A green headline can hide a far less forgiving market underneath. Judging all active funds against the VN-Index alone in a period like this is possible, but it is not automatically the most informative way to judge them.

One Fund Beating the Index Does Not Mean 54 Were “Bad”

According to the report, only 14 of the 55 active equity funds posted positive returns, while 41 were negative. VNDAF, managed by IPA Partner, was the only fund to beat the VN-Index, gaining 6.3%, or roughly 2.1 percentage points more than the benchmark.Người Quan Sát

If investors stop there and conclude that active management is not worth paying for, they miss a more basic question: what was each fund built to do? A fund tilted toward mid-caps, or toward a more defensive style, will struggle to match the VN-Index in a period when the benchmark is being pulled up by a narrow large-cap cluster. Comparison is necessary, but it only helps if the benchmark fits the mandate.

That means not every fund that trailed the index should be read as poorly managed. Some lagged because their style did not resemble the benchmark’s structure. Some may have avoided overheated names on valuation or liquidity grounds. Others may indeed deserve closer scrutiny if they keep underperforming across multiple cycles and multiple market shapes. Those are three different cases, even if they produce the same six-month disappointment on paper.

This is also the cleanest way to understand the ETF versus active-fund trade-off. ETFs largely accept index tracking at a lower fee. Active funds charge more in exchange for the right to deviate from the index, manage risk differently, and tolerate periods of underperformance when their positioning does not match the benchmark’s leadership. If investors are paying for that flexibility, they need to judge it across a full cycle, not only across a distorted half-year.

The Funds Were Not Sitting in Cash

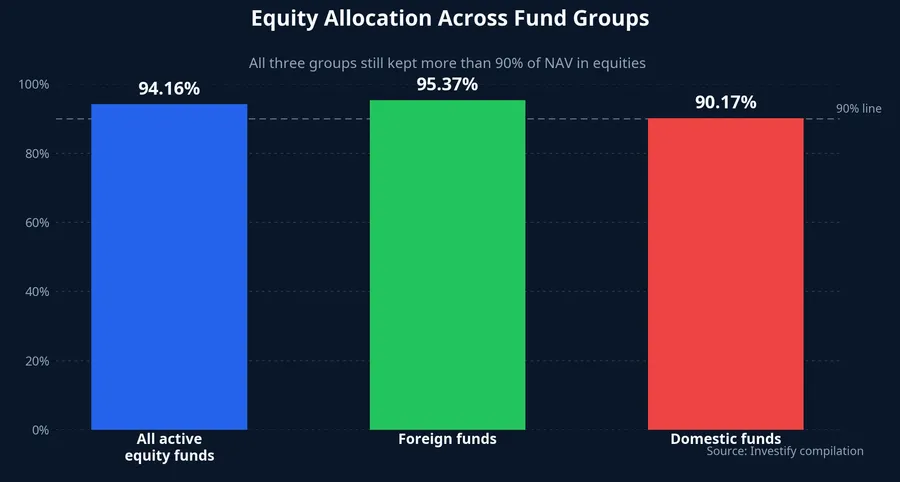

A common reaction when funds trail the index is to assume they were too defensive or held too much cash. The data here does not support that. As of June 30, 2026, the group of active equity funds had total NAV of VND 182,430 billion, with average equity exposure of 94.16%. Foreign-managed funds held 95.37% of assets in equities, while domestic funds stood at 90.17%.Người Quan Sát

In plain English, these funds were in the market. The issue was not that they stayed in cash. The issue was where they were invested inside the market. When an index rise is narrow, being invested is not the same thing as being invested in the part of the market that carries the benchmark higher.

That is why portfolio structure matters more than a single return line. A fund can trail the index in the short run while still holding a more balanced portfolio, taking less concentration risk, or avoiding names whose valuations have become stretched. The opposite is also possible: a fund can miss both the downside protection when markets fall and the upside capture when markets rebound. Those two situations can look similar in a short performance table, but they reflect very different levels of portfolio discipline.

Foreign Fund Redemptions Made the Setup Harder

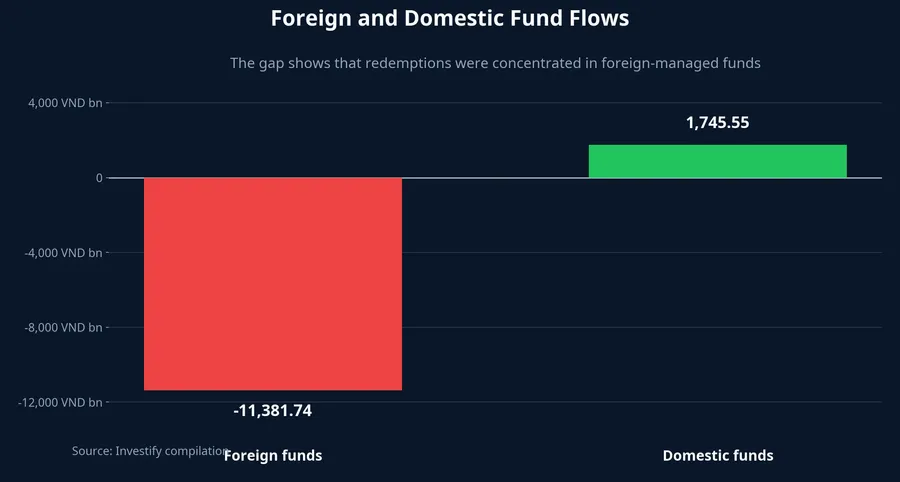

To understand why some large foreign funds lagged more visibly, fund flows matter. From the start of the year through the end of June 2026, foreign funds saw net outflows of VND 11,381.74 billion, while domestic funds recorded net inflows of VND 1,745.55 billion.Người Quan Sát Over the same stretch, several large foreign funds were down: VEIL lost 3.4%, VOF fell 3.6%, VEF declined 6.3%, and PYN Elite Fund dropped 6.8%. Principal Vietnam Equity Fund A fell 9.9%, while United Vietnam Opportunity Fund was down 12.1%.Người Quan Sát

It would be too strong to claim that redemptions alone explain the entire underperformance. But they clearly made the job harder. A fund dealing with withdrawals still has to maintain portfolio discipline, manage liquidity, and decide whether chasing a narrow leadership pocket is worth the trade-off. When those pressures arrive at the same time, keeping up with a concentrated benchmark becomes harder, not easier.

That does not automatically mean foreign funds are worse than domestic funds. A more careful reading is that the operating conditions were different. Domestic managers had inflows to work with. Foreign managers faced outflows on top of a narrow rally. The result reflects both market structure and flow pressure, not pure stock-picking skill in isolation.

How New Investors Should Read This

The first layer is benchmark choice. If a fund leans toward mid-caps or carries a style tilt that differs from the VN-Index, judging it only against the VN-Index can produce the wrong disappointment. A benchmark that better matches the portfolio structure often gives a fairer picture of actual execution.

The second layer is portfolio design. How much is the fund allocating to equities? How concentrated is it? How far does it deviate from the leadership group? What type of risk is it deliberately taking or avoiding? Those questions tell investors what kind of management process they are buying, not just what six months of NAV movement happened to look like.

The third layer is fees. Active funds charge more because they promise value through selection, discipline, and risk control. If a fund cannot demonstrate that value across multiple market environments, investors are right to question the fee. But if they use one narrow-rally period to dismiss active management altogether, they are likely drawing the wrong conclusion from the right data.

The core thesis here is straightforward: the first half of 2026 was an unusually difficult test for most active funds because the most visible benchmark, the VN-Index, was lifted by a narrow rally. The data does not support the claim that active funds simply sat out the market or hid in cash. The next signals worth watching are whether market breadth improves, whether foreign-fund redemptions ease, and which managers can prove post-fee value across more than one market shape. For new investors, this episode is really a lesson in choosing the right measuring stick before choosing the product itself.