When regulators signal more room for credit, the first instinct is easy to understand: banks can lend more, so bank stocks should move up together. That sounds logical at headline level. In practice, though, banking is one of the few sectors where the same policy tailwind can help one balance sheet and expose another at the very same time.

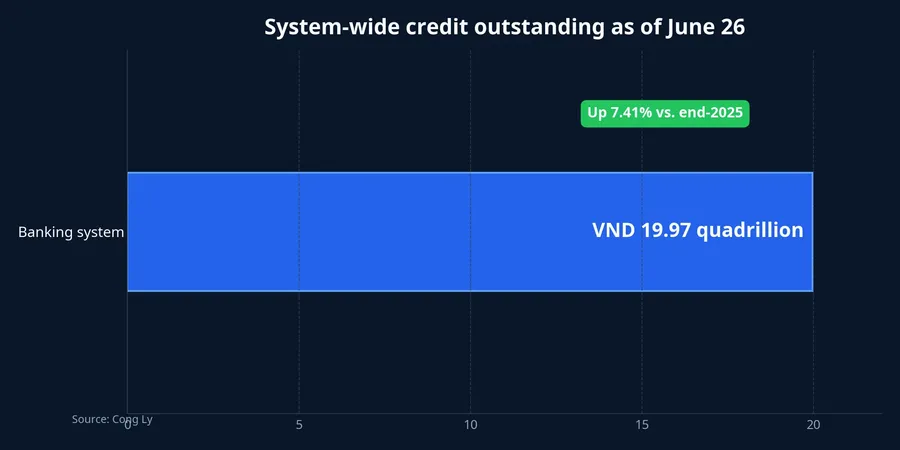

That was the real message behind Vietnam's July 2 market reaction. Total system credit outstanding had risen above VND 19.97 quadrillion by June 26, up 7.41% from the end of 2025 and 18.1% from a year earlier. The State Bank of Vietnam also maintained a system-wide credit growth orientation of around 15% for 2026, subject to real-world conditions.Công lý

Taken on its own, that is an encouraging macro signal. It says credit demand is real. But equity markets do not price banks on the sentence “credit is growing.” They price a bank's ability to turn that growth into net interest income while still controlling funding costs, asset quality and balance-sheet stress.

Selective easing is not broad-based easing

The most misleading phrase in this story is “excluding certain loans from the credit cap.” VietnamNet reported that the SBV had sent documents to commercial banks allowing loans tied to 18 key projects of Vingroup, Sun Group and Masterise to be excluded from credit-limit calculations.VietnamNet

Read too quickly, that can sound like a sector-wide green light. But at the July 2 briefing, Phạm Chí Quang, Director General of the Monetary Policy Department at the State Bank of Vietnam, stressed that credit growth does not mean growth at any cost.VietnamNet In plain English, this is a targeted policy lane, not a blanket loosening for every loan book in the system.

That distinction matters. A bank only benefits directly if it is already financing, or is well positioned to finance, projects inside that priority bucket. A lender focused on retail credit, consumer finance or SMEs may still gain indirectly from better system conditions, but that is very different from receiving an immediate earnings boost from the exclusion itself.

So the cleaner framing is not “all banks got more room.” It is “specific loans tied to specific projects are being treated differently under the credit ceiling.” Once the benefit set is that narrow, price dispersion across bank stocks is not a contradiction. It is the expected outcome.

The market is asking where funding will come from

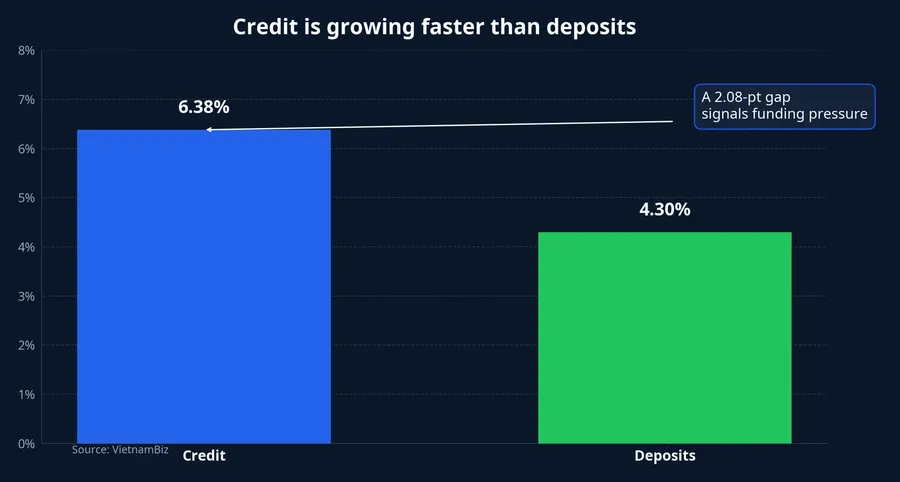

The first data layer investors need to watch is funding. According to VietnamBiz, credit growth reached 6.38% by June 15, while deposit growth was only approximately 4.3%. That approximately 2.08-percentage-point gap means loans were expanding faster than deposits were coming into the system.VietnamBiz

The simplest way to think about it is this: banks are wholesalers of capital. If outgoing inventory grows faster than incoming inventory, margins either get squeezed or the business must restock at a higher price. For banks, that “restocking price” is funding cost, mainly what they have to pay to retain and attract deposits.

That is why a credit-supportive policy does not automatically become a sector-wide equity trade. Banks with stronger CASA franchises, stickier customer bases and lower funding costs are better positioned to turn fresh lending capacity into income. Banks that need to raise deposit rates to sustain loan growth may see a large part of the benefit eaten away before it reaches earnings.

This is where professional investors differ from headline-driven retail flows. They do not stop at the question “can this bank lend more?” They keep going: where does the money come from, how expensive is it and how much profitability remains after the new loans are written? Without credible answers to those three questions, supportive policy is still just supportive policy, not an earnings story.

High LDR means balance-sheet pressure, not a shared upside

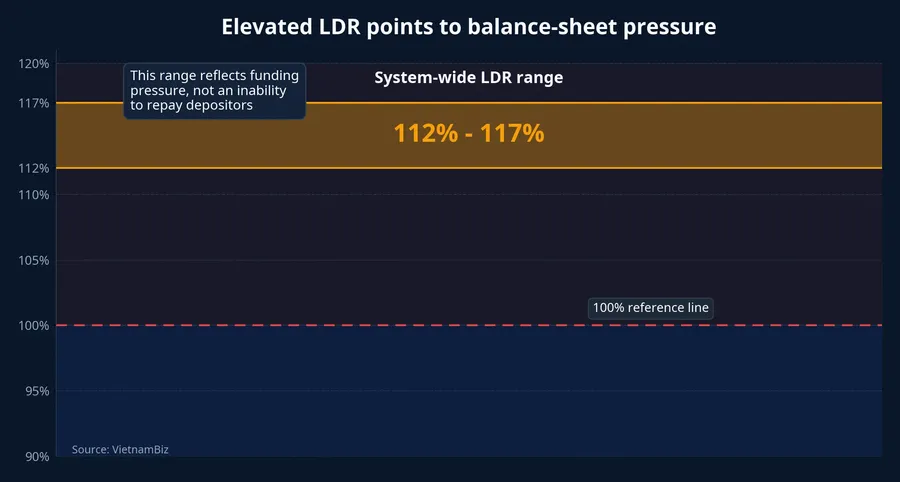

The second layer is LDR, the loan-to-deposit ratio. VietnamBiz quoted Quang as saying that Vietnam's LDR currently stands at approximately 112% to 117%, while state-owned commercial banks are at approximately 111% to 112%. He also drew an important distinction: this is pressure on funding balance, not a sign that banks are unable to repay depositors.VietnamBiz

That may sound technical, but it is central to the equity case. “Balance-sheet pressure” means the system is functioning, yet not every bank has the same degree of comfort in expanding assets further. When LDR is already elevated, every additional unit of credit growth forces management to think harder about liquidity structure, funding resilience and return on incremental lending.

This is exactly why selective easing is different from a broad easing cycle. If every bank received the same relief at the same time, the market could price the sector more uniformly. But when each balance sheet starts from a different place, investors go back to stock picking. Banks with cheaper funding, steadier deposits and less balance-sheet stress will naturally trade differently from banks that still have to fight for funding.

The SBV has also deployed technical measures to relieve some of that pressure. VietnamBiz reported that Resolution 168 allows the Ministry of Finance to raise the ratio of State Treasury deposits placed with commercial banks above 50%, while Circular 25 allows 20% of those Treasury balances to be counted in the LDR denominator.VietnamBiz Those steps help the system. They do not erase the differences in balance-sheet quality across listed banks.

Stock prices already showed that the market does not expect equal gains

If this policy really were a uniform catalyst for the entire sector, the July 2 price action in large-cap banks should have looked much cleaner. It did not. VCB closed at VND 62,300, down 1.11%; BID at VND 42,650, down 0.93%; CTG at VND 34,100, down 0.87%; TCB at VND 33,950, down 1.02%; and MBB at VND 25,650, down 0.39%.

That does not prove bank stocks have turned bearish. It only shows that the market is not willing to buy the entire group on the back of a policy headline alone. At a time when investors are increasingly sensitive to earnings quality and funding structure, a selective reaction is more informative than a broad one.

One caution is still necessary here. Uneven price action does not mean the market fully priced the policy impact in a single session. Other forces may have mattered too, including short-term profit taking and the way capital rotated across large caps that day. Even after allowing for those alternatives, however, the current evidence still supports one clear reading: investors are focusing on balance-sheet durability, not just on easier credit language.

What retail investors should read beyond the headline

That leads to a more disciplined conclusion. A 7.41% rise in credit is positive for economic activity. Excluding loans tied to 18 priority projects from credit-limit calculations is also a meaningful targeted support step. But jumping from there to “every bank benefits” is a leap too far.

The single thesis here is straightforward: policy is creating more room for the system, while the market is still rewarding banks based on their own internal strength. Banks with cheaper funding, more breathing room on the balance sheet and clearer capacity to absorb new lending should stand out more. Banks still constrained by deposits, LDR or loan books with little relevance to the priority-project bucket should see thinner benefits.

In a market that is increasingly hard to trade through broad stories alone, that difference matters. Over the next one to two weeks, the signals worth tracking are not simply whether bank stocks are green or red. The better questions are whether price moves come with stronger liquidity, which banks start getting paid for real data rather than for policy headlines, and whether the gap between credit growth and deposit growth begins to narrow. Those are the signals that separate a headline-driven bounce from a more durable investment case.