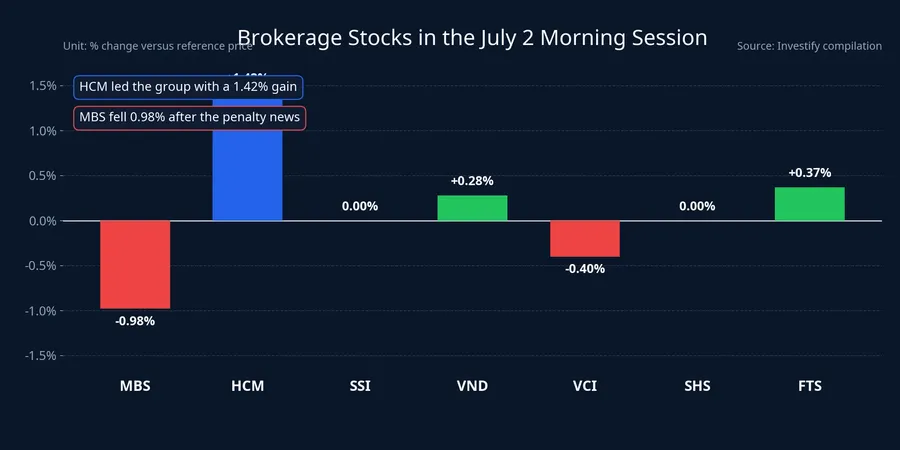

At first glance, the July 2 morning session looked contradictory. MBS fell 0.98% to VND 20,200 per share, while HCM rose 1.42% to VND 28,500, FTS gained 0.37% and VND edged up 0.28%. SSI and SHS were flat, while the VN-Index paused for lunch at 1,869.42 points, up 0.12%. Those numbers do not tell one story for the entire brokerage sector. They show money is reading each company through its own risk and its own room to grow.

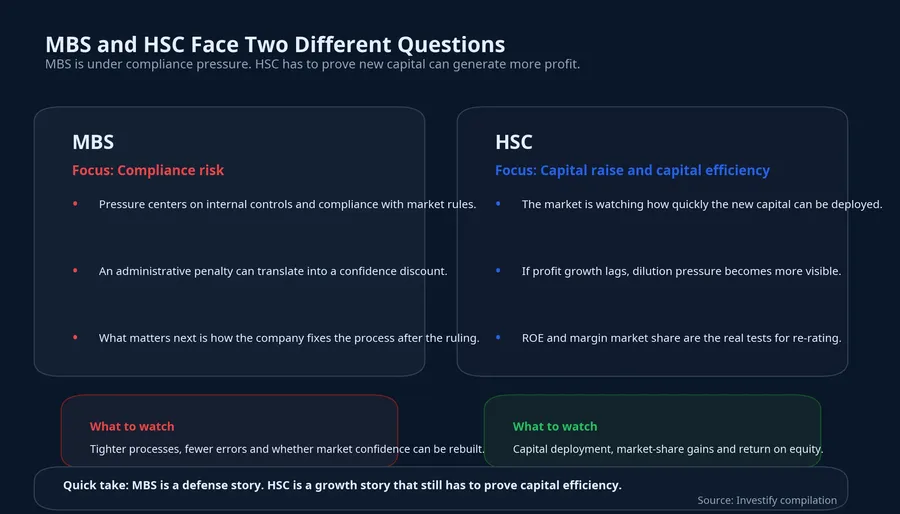

The simplest way to frame it is this: both MBS and HSC touch margin lending, but they sit on opposite sides of the equation. In MBS's case, the market is asking whether the company now deserves a discount because of a compliance failure. In HSC's case, the market is asking whether new capital can be turned into profitable loan growth and market share. That is why the two stocks can trade differently even inside the same industry group.

MBS: The negative signal is operational compliance

Per Nhà Đầu Tư, MB Securities was fined a total of VND 340 million under Decision No. 355/QD-XPHC dated June 29, 2026.Nhà Đầu Tư The largest item was a VND 275 million fine for working with a credit institution to provide loans for securities purchases without prior written approval. The conduct was identified as having taken place from January 1, 2024 to May 5, 2026.Nhà Đầu Tư

MBS was also fined another VND 65 million because at certain points it allowed margin trading in stocks that were not on the permitted list.Nhà Đầu Tư The part investors need to focus on is not only the cash penalty. More important is the additional sanction: a 2.5-month suspension of the service that coordinates with credit institutions to lend money for stock purchases.Nhà Đầu Tư

In plain English, this is an operating-risk issue rather than a signal that the whole brokerage industry is being squeezed at once. MBS was not suspended from all brokerage operations, and the source article does not show that every margin-lending channel at the firm has been shut. That makes a company-specific discount the most reasonable initial market response, rather than an industry-wide verdict.

Why HSC is being viewed through a different lens

At the same time, HSC is trading on a very different narrative. Per Tuổi Trẻ, the company was granted a certificate to offer nearly 270 million shares to existing shareholders at VND 10,000 per share, implying expected proceeds of nearly VND 2,700 billion.Tuổi Trẻ The proceeds are intended to support margin-lending operations.

For newer investors, the phrase "share issuance" often immediately translates into dilution risk. That concern is valid, but incomplete. A brokerage business is one where equity capital heavily shapes how far margin lending can expand. When the equity base gets thicker, the company gains more room to grow its loan book and more balance-sheet flexibility to support trading operations.

That is why HSC is being judged differently from MBS. One side of the market is asking about discipline and compliance. The other is asking about how efficiently new capital can be put to work. Investors can tolerate short-term dilution if they believe the proceeds will create more profit over the following quarters.

The Tuổi Trẻ report also shows why the capital-raising story is meaningful in HSC's case. At the end of the first quarter of 2026, the company had about VND 40,467 billion in total assets, more than VND 28,140 billion in margin loans and VND 14,402 billion in equity. Operating revenue reached VND 1,466 billion, up 46.7% year on year, while pre-tax profit came in at nearly VND 364 billion, up 28.4%.Tuổi Trẻ Those numbers do not guarantee further upside, but they do explain why the market reads this as an expansion story rather than a defensive capital patch.

The same margin theme can mean very different things

This is where the confusion is easiest to make. Both MBS and HSC are tied to margin lending, so a quick reading may suggest they are being pulled by the same force. In reality, the underlying issues are different.

At MBS, margin lending is where investors are testing compliance quality. According to Nhà Đầu Tư, first-quarter 2026 lending revenue reached VND 439 billion, up 59% from a year earlier and accounting for about 43% of total operating revenue. Margin loans and advance-selling receivables stood at nearly VND 14,867 billion as of March 31, 2026, while short-term borrowings from credit institutions were nearly VND 16,974 billion.Nhà Đầu Tư When a business line that important is tied to a penalty and a suspension of a related service, investors have a reason to lower the multiple they are willing to pay.

At HSC, margin lending is where the market is looking for expansion capacity. If the new capital is deployed into a market with healthy trading activity, it can turn into interest income and market-share gains. But one counterpoint still matters. The source article shows HSC has secured a financing tool. It does not prove that future profits will automatically rise in step.

That is why the right reading is not that the market has "ignored" bad news at MBS, or that HSC's capital raise is automatically bullish. A better reading is that the market is currently paying more for an open-ended growth story while immediately marking down a risk that has already become visible. This is classification, not blind enthusiasm for the whole sector.

What first-time investors should watch next

The first signal is whether the price response lasts beyond one session. A mixed morning is a starting data point, not a final verdict. If MBS continues to lag the rest of the broker group in the following sessions, the market is confirming a company-specific discount for compliance risk.

The second signal is the quality of margin-lending growth. For HSC, raising capital only matters if the loan book expands without a sharp erosion in lending spreads. For MBS, the question is different: after the penalty, does the company need to change its service structure enough to create a visible hit to lending revenue.

The third signal is confidence in governance. When a company is questioned at the level of systems and risk control, the confidence discount can appear before the financial impact is fully visible in the income statement.

Conclusion: This is a selective test, not a sector-wide vote

The most important takeaway from the July 2 morning session is that money is not buying brokerage stocks as a single block. It is separating companies with visible compliance risk from companies that still have a capital-expansion and lending-capacity story. That thesis only changes if later sessions show that the MBS issue extends to the broader business model of other brokers, or if HSC fails to turn new capital into real operating growth.

For newer investors, the point is not to pick a side immediately. The point is to remember that the right way to read an industry group starts with each company, each profit engine and each type of risk. Second-quarter results and the next read on margin balances will be the most useful signals to watch.