The most important part of the Fed's latest message is not whether Kevin Warsh sounded more hawkish or more dovish. It is the broader shift in how he wants markets to behave. Instead of waiting for the central bank to hint at every next move, investors are being pushed back toward the harder work of reading the economy itself. For Vietnamese investors, that is not an abstract Wall Street debate. It shapes how to read the dollar, gold, US Treasury yields, and pre-open market sentiment at home.MarketWatch

Kevin Warsh, Chairman of the Board of Governors of the Federal Reserve System, and also Chair of the Federal Open Market Committee, was not making an offhand comment. He said investors should not look for clues about the next rate move in each Fed remark, while AP noted that he also stressed the Fed's political independence and its commitment to returning inflation to the 2% target.FedAP

That is a meaningful change in market regime. For years, investors got used to a system in which Fed language itself could do much of the work. A softer sentence could lower yield expectations. A firmer phrase could reprice growth stocks within minutes. That mechanism has not disappeared, but Warsh's message suggests the Fed wants less reliance on forward hints and more reliance on incoming data.

For retail investors in Vietnam, that matters because US macro news usually lands after local trading hours or shortly before the next domestic session. If the habit is to react to headlines alone, the result is often emotional trading. If the new reality is that the Fed is offering less verbal guidance, then the real advantage lies in knowing which data releases can actually reset global pricing.

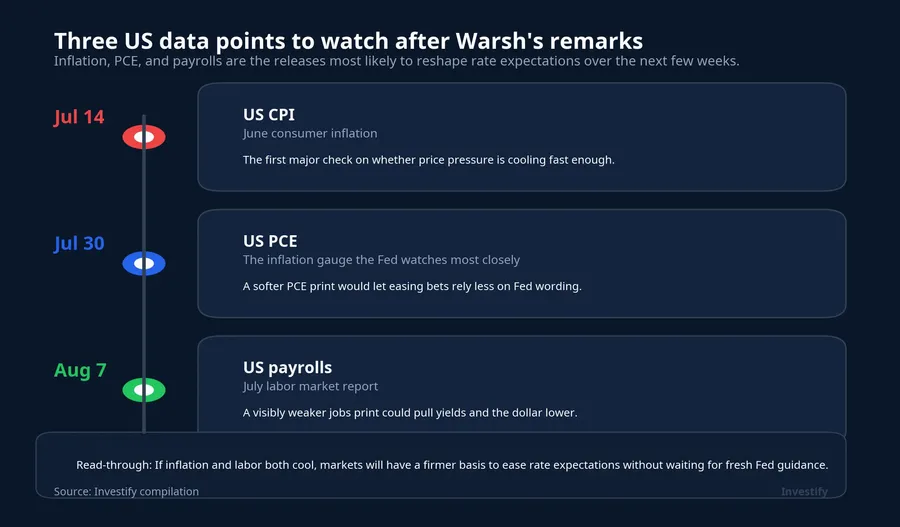

First signal cluster: inflation

The Fed may stay flexible on timing, but it has little room to go soft on inflation. That is why CPI and PCE remain the first indicators to watch after these remarks. If June CPI shows a clearer cooling trend and late-July PCE confirms it, markets will have firmer grounds to lower rate expectations on their own rather than waiting for the Fed to prepare them verbally.BEA

Markets are not watching just one number. They are watching whether the direction is convincing. A mild slowdown in inflation may calm nerves, but it may not be enough to drag Treasury yields lower in a durable way. If CPI or PCE still points to sticky price pressure, then the Fed's message of "do not expect hints" will be read in a tougher light: policymakers want to preserve flexibility because they still do not trust the inflation trend.

That has a direct Vietnam angle. A higher-for-longer US rate backdrop often supports the dollar, keeps pressure on exchange rates, and makes investors less willing to chase risk assets aggressively. That does not mean the VN-Index must fall every time US inflation disappoints. It means local bullish stories will have a harder time broadening out if the global macro backdrop remains dominated by a firm dollar and elevated yields.

Second signal cluster: jobs

If inflation tells investors how much room the Fed has to soften, the labor market tells them how quickly the US economy is actually cooling. That is the other half of the equation. A friendlier inflation print will not be enough if employment remains too strong. In that case, wage growth and household demand may continue to keep core inflation pressure alive, which in turn keeps yields elevated.

On the other hand, a clearer slowdown in jobs data can change pricing fast. When payroll growth cools and unemployment edges higher, the question stops being "what did the Fed say?" and becomes "what is the market forcing the Fed to acknowledge?" The larger point is that the Fed may be trying to speak less, but if labor data shifts decisively enough, markets will guide rate expectations without needing any verbal nudge.

That said, investors should not overstate the implication. Weaker jobs data does not automatically mean stocks rally. If labor softens while inflation stays hot, markets can move into a more uncomfortable setup: weaker growth without a clean path to easier policy. In that scenario, gold may hold up better than growth stocks, while the dollar may stay stronger for longer than many hope.

Third signal cluster: asset confirmation

Once the data lands, the next step is to see which assets confirm the story. The DXY stood at 101.30 on July 1, while USD/VND was 26,314.50 on the same day. Those levels suggest exchange-rate pressure is still present, but not yet in outright shock territory. If upcoming data softens while DXY remains firm, markets may be pricing a separate risk, such as lingering safe-haven demand for the dollar.MarketWatch

The 10-year US Treasury yield was around 4.48% on July 1, making it the clearest bridge between Fed expectations and global equity valuations.MarketWatch If yields fall alongside a weaker dollar and softer inflation data, that is fairly clean confirmation that financial conditions are easing. If yields stay elevated even as Fed rhetoric sounds gentler, the market is effectively saying the data still does not justify a cheaper-money story.

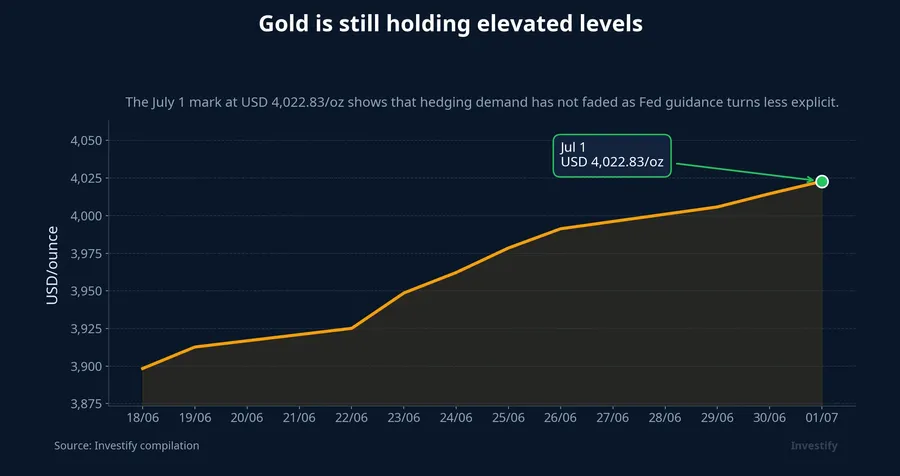

Spot gold was at USD 4,022.83 per ounce on July 1. That is not a detail to skip over. Gold is highly sensitive to real yields and hedging demand. If yields rise but gold holds firm or even edges higher, markets may still be uneasy about policy credibility or growth risks. If yields fall and gold rises at the same time, that is a stronger sign that easing expectations are spreading beyond just headline interpretation.AP

The Nasdaq closed at 26,040.03 on July 2, down 0.7% in one session, while the VN-Index ended July 1 at 1,867.21, up 0.39%. The two markets do not move in lockstep, but Vietnamese opening sentiment still reacts quickly to US tech moves when the underlying story is interest rates. The Nasdaq slide therefore is not a direct buy-or-sell signal for local investors. It is a prompt to ask the more useful question: are US growth stocks being repriced because the data is deteriorating, or because the market still lacks the confirmation it wants?

A practical pre-open framework for Vietnam

When the Fed steps back from guiding markets with words, the most effective reading framework has three stages. First, check whether inflation is cooling clearly enough to take pressure off yields. Second, see whether jobs data confirms that the US economy is moderating rather than overheating. Third, look at the cross-asset reaction in DXY, yields, gold, and the Nasdaq to see whether markets are telling one consistent story.

That is a far more useful framework than waiting for one dovish sentence from the Fed. It also fits the reality for Vietnamese investors, because most local decisions are made before New York begins another session. If an overnight headline is not yet backed by data, the next morning's reaction is often emotional rather than analytical. When both the macro releases and the asset response line up, the signal becomes much more reliable.

The conclusion here is not that the Fed is definitely about to cut rates or definitely about to stay restrictive for longer. The cleaner conclusion is that the Fed is deliberately reducing the role of verbal guidance, and markets are being pushed back toward hard data. For Vietnamese investors, the edge over the next few weeks will not come from guessing Warsh's next sentence. It will come from following the right signal stack: inflation, PCE, jobs, yields, the dollar, gold, and the Nasdaq. If those pieces shift together, markets will reprice before the Fed needs to say much more.