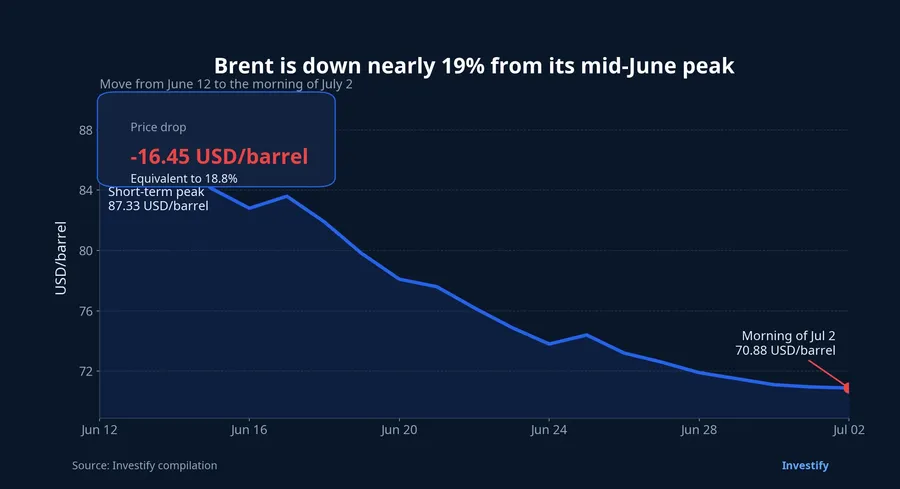

Brent is down almost 19% from its short-term peak on June 12 to the morning of July 2, yet most Vietnamese oil and gas stocks still closed in positive territory on July 1. In plain English, that is a warning against the simplest reading of the sector: lower oil does not automatically mean the whole oil complex has to fall together. The market is asking a more useful question stock by stock: is this name being priced for crude, for orders, or for a company-specific trigger?

That split was already visible in the last session. Brent settled at USD 71.57 a barrel on July 1, down 1.89% from the prior session, and market data showed it easing further to USD 70.88 on the morning of July 2. The Guardian reported that Brent traded around USD 72.17 as investors grew less concerned about supply disruption around the latest US-Iran talks, while VietnamPlus said the market had trimmed part of its supply-risk premium as the outlook for flows looked less strained.The Guardian VietnamPlus

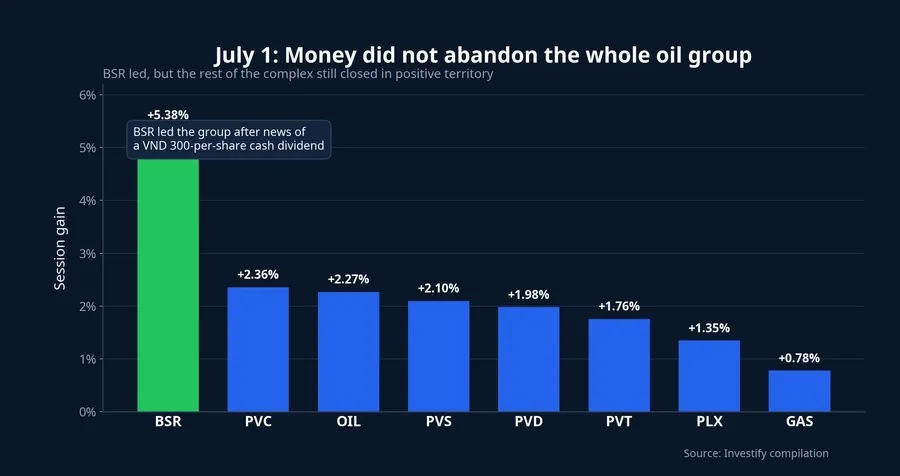

Vietnamese equities did not follow that move in a straight line. BSR rose 5.38% to VND 25,450. PVD gained 1.98% to VND 33,450. PVS climbed 2.10% to VND 38,900. PVT added 1.76% to VND 20,200. PLX rose 1.35% to VND 37,450. OIL gained 2.27% to VND 13,500. GAS edged up 0.78% to VND 78,000, while PVC advanced 2.36% to VND 13,000. Anyone using a single Brent number as a shortcut for the whole sector would have missed what the tape was actually saying.

Why oil stocks do not move as one

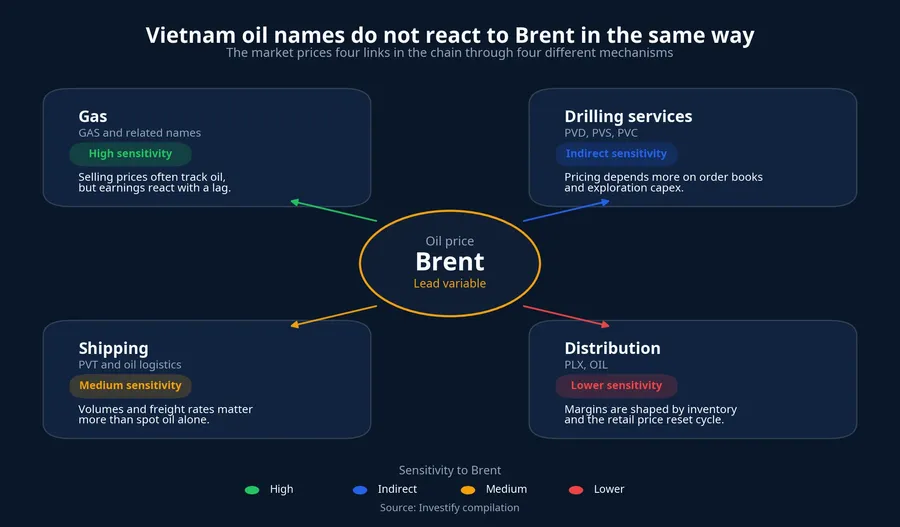

The first thing a newer investor needs to do is break the oil and gas chain into separate links. Each link absorbs oil-price moves differently, so one weaker Brent session does not automatically translate into the same reaction across every stock.

For gas names such as GAS, selling prices and earnings usually track oil with a contractual lag. That means a lower oil price today does not instantly turn into weaker earnings in the current reporting period. What the market discounts first is the next set of expectations: if Brent stays lower for longer, future revenue and margin assumptions may need to come down.

For drilling and technical service names such as PVD, PVS, and PVC, the transmission channel is even more indirect. These companies are not selling crude the way an upstream producer does. The market is asking a different question: will lower oil slow drilling programs, rig leasing, vessel demand, or broader exploration spending? Put simply, this group is more sensitive to the order pipeline than to spot crude itself.

PVT sits in a softer part of the chain. Oil and gas shipping depends on cargo volumes, routes, and freight rates, so the reaction does not need to mirror Brent tick for tick. PLX and OIL also deserve separate treatment. A lower crude price is not automatically negative for distributors, because inventory accounting and the lag in domestic retail-price resets also matter. Decree 80/2023 shortened the retail adjustment cycle from 10 days to 7 days, but local prices still do not move minute by minute with Brent.Chính phủ

July 1 showed money sticking to stock-specific stories

BSR is the clearest example of the market choosing an individual story over a broad sector call. The stock jumped 5.38% in the July 1 session, well ahead of the rest of the group. On the same day, Vietstock reported that BSR had set the record date for a 2025 cash dividend of 3%, equal to VND 300 per share.Vietstock For a stock with a clear near-term cash event, that corporate trigger can matter more than one overnight drop in oil.

PVD offers another useful case. On June 30, Vietstock reported that PV Drilling planned to issue nearly 371.9 million new shares, equal to a 66.9% ratio, lifting charter capital to nearly VND 9,300 billion.Vietstock The stock still gained 1.98% in the following session. That does not prove PVD is immune to oil, but it does show that part of the market is currently pricing the capital story and future order visibility rather than reacting mechanically to Brent.

The gap in reaction size matters as much as the direction. GAS rose only 0.78%, clearly trailing BSR, PVC, and OIL. That makes sense. Gas businesses tend to face a lagged earnings response, so when Brent drops quickly, investors become more conservative on medium-term expectations. By contrast, names with a clearer short-term trigger have been better able to keep money in the trade.

That is why the right question for July 2 is not whether “oil stocks are up or down.” The better question is which names still have a reason for capital to stay. In a differentiated market, a concrete thesis will always beat a broad slogan.

What a near-19% Brent pullback is really testing

From USD 87.33 a barrel on June 12 to USD 70.88 on the morning of July 2, Brent has fallen about 18.8%. For a retail investor, that is a large enough move to assume the entire Vietnamese oil complex must be repriced. What matters, though, is that the market did not behave that way in the latest session. The drop in oil is acting more as a stress test for each individual investment case than as a final verdict on the entire sector.

If Brent stays in the lower range for several more sessions, pressure will build first on the names that depend on order expectations, especially PVD, PVS, and PVC. That is where investors should watch whether liquidity still holds, because oilfield service names usually react early when the market starts worrying about upstream capex. If those stocks keep trading well even without an oil rebound, the message is that money still believes the order story and company fundamentals can absorb the commodity weakness for now.

BSR needs a two-layer reading. One layer is feedstock cost. The other is refining spread, inventory position, and the dividend event. That is why BSR should not be placed in the same emotional bucket as GAS or PVD. They all sit inside the oil sector, but their earnings engines and the market's focus are not the same.

PLX and OIL also need to be treated separately. Many investors assume that lower oil must hurt fuel distributors. In reality, the impact depends on inventory cost, the speed of retail-price resets, and trading margins. In some short windows, softer oil can even ease input pressure before the domestic pricing mechanism fully catches up. That helps explain why these stocks do not need to move in lockstep with Brent every session.

A more useful framework for July 2

The cleanest conclusion is that this is a differentiation test, not an on-off switch for the whole Vietnamese oil sector. Brent matters, but it is not enough on its own to decide every stock in one session. Gas should be read through earnings lag. Oilfield services should be read through orders and flow. Shipping should be read through volume and freight. Distribution should be read through inventory and the pricing cycle.

The key signals for the rest of July 2 are specific. Does liquidity still hold in PVD, PVS, and BSR? Does a thinner move such as GAS weaken further? Do PLX and OIL keep showing their own pattern, or do they start moving back in line with crude? If those signals all deteriorate together, the market will drift back toward the old one-factor reading, with Brent taking over as the dominant driver. If they hold, the lesson from this move becomes clearer: in Vietnamese oil stocks, reading the right link in the chain matters more than reacting to a single crude number.