TV2 has come back with a fresh business plan, and at first glance the story does not look disastrous. The company is still talking about revenue growth, still presenting a profit target, and the stock has not shown the kind of collapse that usually signals panic. That is exactly why the case is useful for new investors: after a governance shock, the market is not pricing earnings alone. It is pricing how much trust those earnings still deserve.

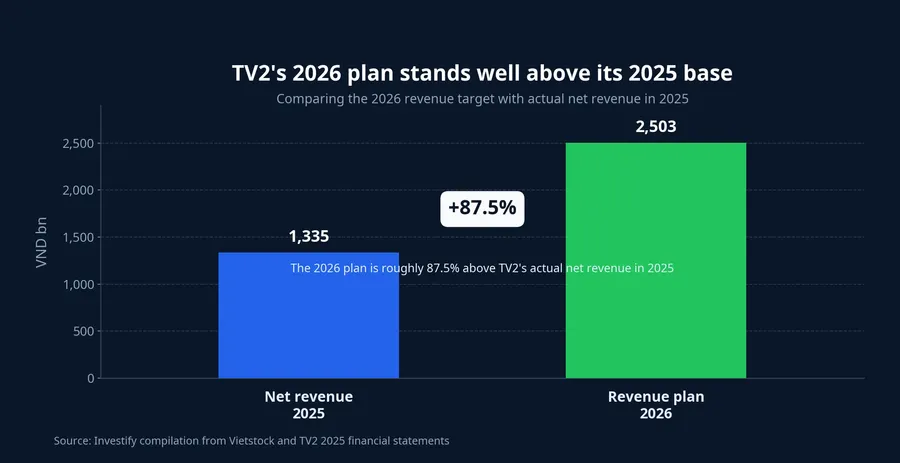

At the June 30 annual general meeting, Power Engineering Consulting Joint Stock Company 2 set a target of roughly VND 2,503 billion in revenue and more than VND 100 billion in net profit. At the same meeting, shareholders removed Mr. Nguyễn Chơn Hùng, former Chairman of the Board of Directors of Power Engineering Consulting Joint Stock Company 2 (TV2), from his board member status after the prosecution case was brought back into focus.Vietstock Those two developments belong in the same frame. One is about this year's ambition. The other is a reminder that TV2's real challenge is not only hitting a target, but rebuilding confidence in the machinery behind that target.

A new plan does not settle the old question

The simplest way to think about it is this: a business plan tells you where management wants to go, while governance tells you whether the vehicle is still reliable enough to get there. If the control structure has already shown cracks, investors cannot listen only to the destination. They also need to inspect the engine. That is why two companies with similar profit numbers can still trade on very different valuation multiples.

At the AGM, Mr. Đinh Quang Tri, Independent Member of the Board of Directors of Power Engineering Consulting Joint Stock Company 2 (TV2), described the incident involving the former chairman as a painful lesson and suggested that EVN could send a direct representative to the board and tighten oversight at the company. The meeting also confirmed Mr. Phạm Liên Hải, Chairman of the Board of Directors of Power Engineering Consulting Joint Stock Company 2 (TV2), for the 2025-2030 term, while Mr. Võ Văn Bình, Chief Executive Officer of Power Engineering Consulting Joint Stock Company 2 (TV2), was identified as taking the top executive role from April 28, 2026.Vietstock

The key issue is not how quickly the company replaced people. The key issue is how much of the underlying process changes with them. Retail investors often see a new chairman or a new CEO and assume the situation has normalized. In practice, personnel is only the visible layer. The more important layer sits underneath it: contract approval, document verification, cash monitoring and the tone of disclosure to shareholders.

TV2 also has EVN as a controlling shareholder with a 51.33% stake. In a company with that kind of ownership concentration, minority investors should pay even more attention to how they are protected instead of assuming that a major backer automatically makes the situation safe. A strong shareholder can help stabilize a company, but that only matters if the oversight framework is clear.

Read the profit line more slowly after a governance event

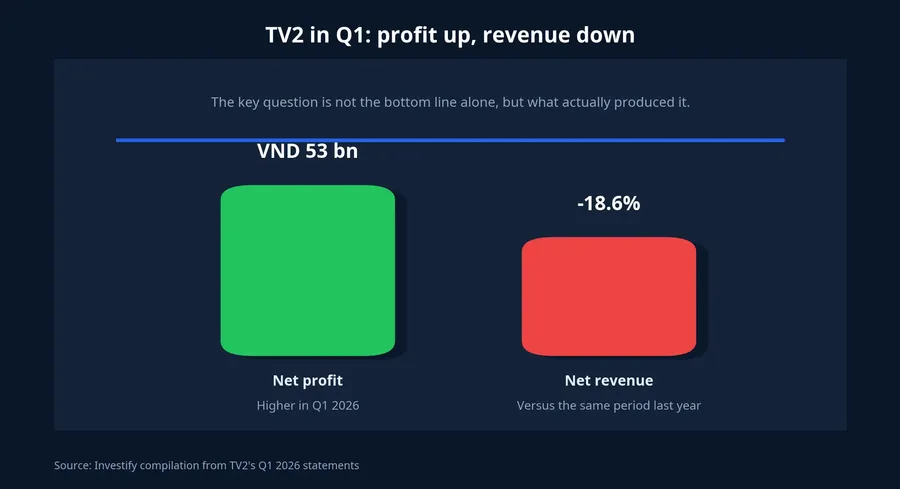

In the first quarter of 2026, TV2 reported VND 244 billion in net revenue and VND 53 billion in net profit. Revenue fell 18.6% year on year, while profit jumped sharply from the VND 14.5 billion base posted in the first quarter of 2025. This is exactly the type of picture that tempts new investors into a quick conclusion that the business is fine. But when revenue declines while profit rises, the right response is not comfort. The right response is to examine what is happening one layer deeper.Vietstock

That does not mean TV2 is necessarily deteriorating. It means the bottom line alone is not enough to tell you how healthy the recovery really is. If profit is rising because the core business is expanding in a durable way, that is one story. If profit is rising because of financial income or other less repeatable factors, that is a very different story. New investors often miss this distinction.

At TV2, financial income in the first quarter rose to about VND 20.9 billion from roughly VND 2.8 billion a year earlier. Total liabilities climbed to about VND 2,944.4 billion at the end of the first quarter of 2026, up from around VND 1,704 billion at the end of 2025. At the same time, net cash flow from operating activities reached about VND 1,046.6 billion after a negative VND 84.4 billion in the first quarter of last year. None of those shifts automatically signals trouble, but they do force investors to examine receivables, payables and working-capital dynamics rather than stopping at the reported profit figure.Vietstock

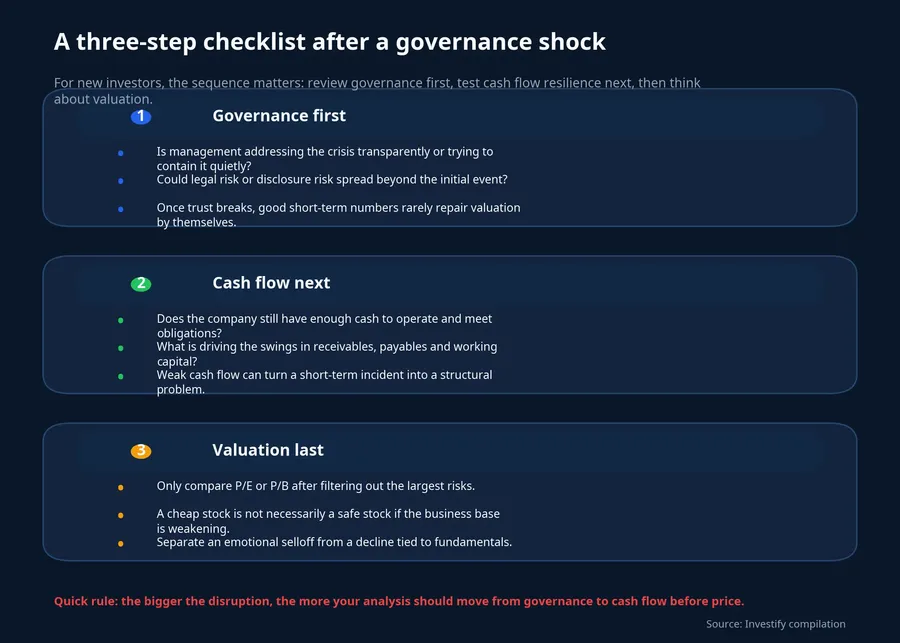

This is where beginners should change the order in which they read a set of accounts. Do not begin with whether the P/E looks cheap or expensive. Start with three simpler questions: does profit convert into cash consistently, is debt rising because the company is expanding or because working capital is stretched, and is the new leadership explaining those swings clearly enough. If those answers remain blurry, an attractive valuation is still only surface-level comfort.

A firm share price is not proof that the risk has passed

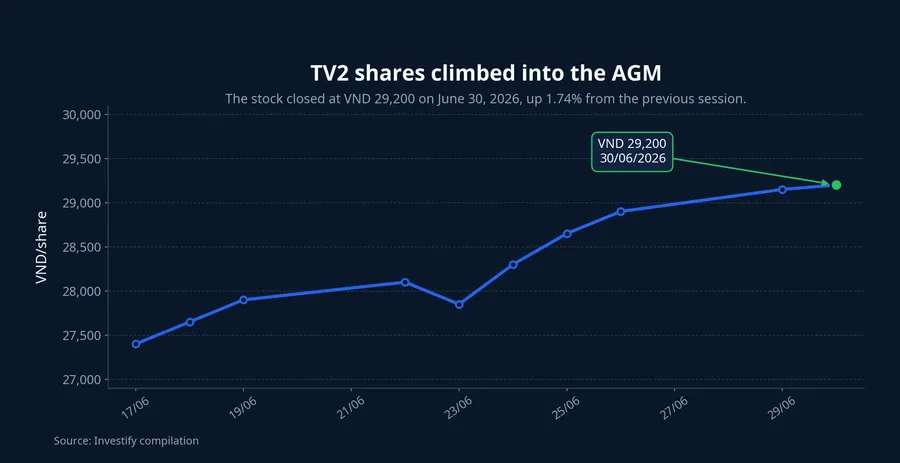

TV2 closed the June 30 session at VND 29,200 per share, up 1.74% from the previous day, giving the company a market value of about VND 2,000 billion. A steady stock price, or even a rising one ahead of the AGM, can easily create the impression that the market has already accepted the new narrative. But price action over a handful of sessions only captures short-term expectation. It does not prove that the governance discount has disappeared.

Think of the stock price as a thermometer, not a full diagnosis. For a company emerging from a governance shock, a few positive sessions only tell you that the market is still watching. They do not mean the market has stopped asking questions about internal control.

Even the target of more than VND 100 billion in net profit should be treated as a test ahead, not as a certificate of recovery. If coming quarters show that profit is supported by stable core revenue, cleaner cash flow and more disciplined communication from the new leadership team, the governance discount can narrow. If the targets still look good while the answers on process, accountability and internal control remain vague, the market has every reason to keep its distance.

Three signals worth tracking after the AGM

After a disruption like TV2's, the useful exercise is not to guess immediately whether the stock will rise or fall next. The more useful exercise is to watch what the new leadership can prove through data and behavior.

The first signal is disclosure quality after the AGM. Does the company clearly explain accountability, corrective measures and process changes, or does it stop at reassurance. The second signal is the consistency between profit, revenue and cash flow over the next few quarters. The third signal is the rhythm of communication from the new board and executive team. Consistent transparency may not lift the stock in a single session, but it is often what determines whether the market will eventually pay a higher multiple over the medium term.

The core conclusion is straightforward. TV2's new business plan is necessary if the market is going to keep paying attention, but it is not enough to push governance risk into the background. For new investors, the filter should run in the opposite order from the usual habit: governance first, cash flow second, valuation last. When a company has just gone through a top-level disruption, moving more slowly on governance is often what keeps you from moving too quickly on valuation.