A rising bank sector used to be simple shorthand for a market that still had leadership. By the end of June, that shortcut was starting to break down. Fresh forecasts for the second quarter of 2026 point to a more selective picture: some banks are being rewarded for fast credit growth, some for operating stability, and some are being held back by weaker NIM or heavier provisioning.Nhịp sống KD

That distinction matters because retail investors often treat banks as the market's default anchor. In plain terms, when the VN-Index rises, many assume bank stocks are the safest way to ride the move. The market is becoming less forgiving than that. Banks may still help support the index, but money is no longer paying the same multiple for every earnings story.

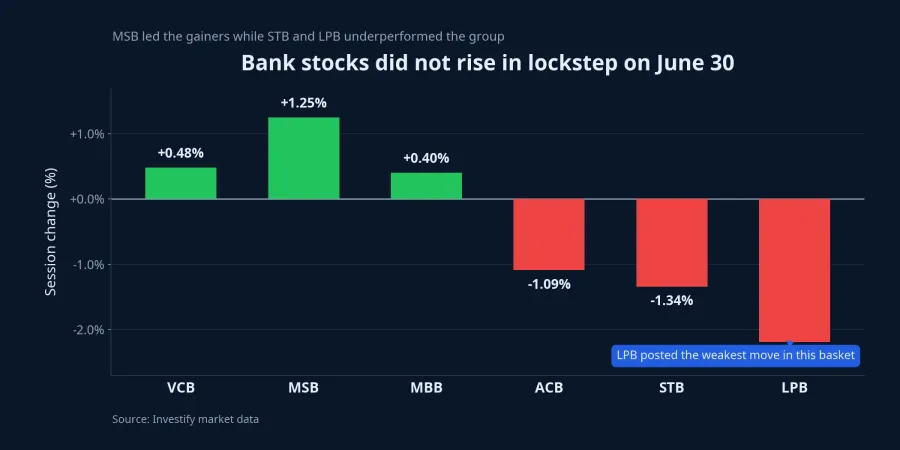

One green session does not tell the whole story

On June 30, the VN-Index closed at 1,860.01 points, up 0.27%. In the same session, VCB rose 0.48%, MBB gained 0.40% and MSB climbed 1.25%, while ACB fell 1.09%, STB lost 1.34% and LPB dropped 2.19%. If you only read the sector label, you miss the fact that banks were already trading in clearly different lanes on the same day.

Price action alone is not enough to prove that all of that divergence came from earnings expectations. End-quarter portfolio rebalancing, short-term trading flows and index support can all matter as well. But when stock moves start separating just as the market receives new earnings data, investors have a good reason to look deeper instead of treating the sector as a single block.

According to Nhịp sống Kinh doanh's June 29 summary of an MBS report, second-quarter 2026 net profit for the banks under coverage is expected to rise by about 15% year over year. That sounds constructive, but it is only an average. Beneath that average sits a wide gap between banks expected to grow by more than 40%, banks delivering steady double-digit growth, and banks that may be flat or down.Nhịp sống KD

The high-growth group: equally fast, not equally clean

VPBank is the clearest example of the high-growth branch. MBS forecasts second-quarter net profit of about VND 7,499 billion, up 51.9% year over year, with the main engine coming from credit growth that could reach roughly 25% from the start of the year. Net interest income is projected to rise around 34%, even as provisioning expense still increases by roughly 20%.Nhịp sống KD

The simple way to read that is that VPBank is growing quickly because lending is growing quickly. If the loan book expands fast enough, profit can still move higher even when funding costs are not especially comfortable. The key lesson for newer investors is that this kind of growth comes with real earnings torque, but it also has to be read together with the provision buffer. Fast credit growth without matching asset quality can force the market to reprice the story very quickly in later quarters.

HDBank belongs in the same high-growth bucket, but its structure looks smoother. MBS forecasts second-quarter net profit of about VND 5,381 billion, up 46.4% from a year earlier. Credit growth in the quarter could be roughly 10% versus the end of the first quarter, taking first-half growth to approximately 20%, while provisioning expense is expected to fall around 20% because last year's comparison base was high.Nhịp sống KD

That difference between VPBank and HDBank is exactly the kind of nuance retail investors need to practice. Both are above 40% growth, yet one leans more heavily on rapid credit expansion while the other also benefits from an easier provisioning base. On a stock screen, they can look like the same idea. In portfolio analysis, they are not.

The steady growers: where the market looks for balance

If the fastest growers attract the most attention, the steady growers often attract the most confidence. MBS forecasts Techcombank at about VND 7,468 billion in second-quarter net profit, up 17.7% year over year. Vietcombank is seen at VND 10,262 billion, up 16.1%; BIDV at about VND 7,937 billion, up 15.1%; and VietinBank at about VND 11,022 billion, up 13.0%.Nhịp sống KD

This group does not deliver the same headline pop as VPBank or HDBank, but it offers something else: a steadier operating base. For Techcombank, MBS expects support from non-interest income such as investment banking, insurance and bad-debt recovery. For Vietcombank and VietinBank, the advantage is lower funding costs, while VietinBank is also projected to keep non-performing loans around 1.0% and its bad-loan coverage ratio above 150%.Nhịp sống KD

In practical terms, this is the part of the sector the market often pays for resilience rather than speed. When investors still want exposure to large-cap banks but do not want to own the most cyclical earnings profiles, lenders with stable NIM, manageable asset quality and more predictable operating momentum can become the preferred parking place. That is why a good earnings season does not automatically lift every bank stock at the same pace.

The flat-to-down group: where NIM and provisioning matter most

The hardest part of the banking sector to read is always the group that no longer benefits from a uniform growth story. ACB is a useful example. MBS forecasts second-quarter net profit at about VND 4,899 billion, essentially flat with growth of just 0.4% year over year. The drag is not disappearing credit demand, but weaker non-interest income, which is expected to fall by more than 10% because debt-resolution income is no longer as strong as it was a year earlier.Nhịp sống KD

Sacombank is under more obvious pressure. MBS forecasts second-quarter net profit of only about VND 1,666 billion, down 42.4% year over year. NIM could fall to roughly 2.5%, provisioning expense is expected to double and second-quarter non-performing loans are projected at about 6.0%.Nhịp sống KD

LPBank is also expected to move backward, with second-quarter net profit around VND 2,244 billion, down 6.3% from a year earlier, while provisioning expense could rise by about 39%. If you connect those projections with the price reaction on June 30, it is reasonable to say the market is becoming more cautious toward banks whose earnings outlook is no longer moving in the same direction as before. That said, discipline still matters: a single day's price move does not prove the market has fully and correctly priced second-quarter results. It only suggests that money is becoming more selective across the sector.Nhịp sống KD

How retail investors should read this earnings season

The main point here is not which bank is "the buy." The more useful takeaway is how to read the numbers. For the high-growth banks, look at the quality of credit growth and the size of the provision cushion. For the steady growers, watch whether NIM, funding costs and bad-loan ratios are actually holding where expectations say they should. For the flat or declining group, the key question is whether the pressure comes from a temporary line item or a more persistent deterioration in earnings quality.

The clearest thesis right now is that second-quarter results are likely to expose more dispersion inside the banking sector, not less. Money may still come back to banks because they remain liquid large-cap names with heavy index weight. But the gap between stocks supported by genuine earnings strength and stocks simply floating on a sector trade is likely to widen further.

Over the next one to two weeks, the three signals worth tracking are actual credit growth, NIM direction and provisioning levels as second-quarter reports arrive. If those variables line up with current expectations, the case for a more segmented banking trade gets stronger. If profit rises at some banks while asset quality deteriorates faster than expected, the market will have to reprice those stories quickly. For retail investors, that is the real lesson of this earnings season: do not buy a sector label when what the market is really paying for is the earnings quality of each individual bank.