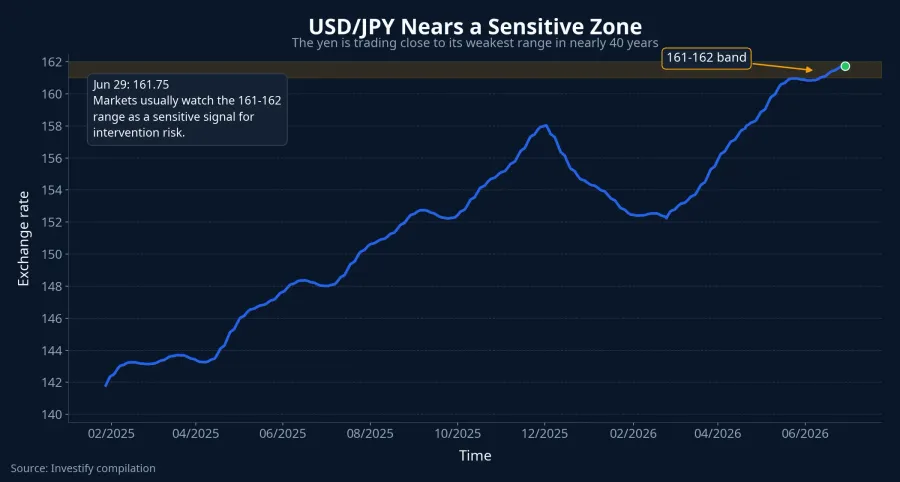

The Japanese yen is moving into a zone global markets watch very closely: near its weakest range in almost 40 years against the US dollar.CafeF For Vietnamese investors, the real issue is not simply that Japan has a weak currency. The bigger question is what that weakness says about the strength of the dollar, the resilience of Asian currencies, and the mood of short-term capital across the region.

On June 29, USD/JPY closed at 161.75, while DXY stood at 101.35 and USD/VND at VND 26,308 per dollar. Put together, those numbers point to a sensitive setup. The dollar is not in a disorderly global surge, but currency pressure in Asia is already visible enough for the yen to become the first screen markets look at. For Vietnam, this works better as a risk filter than as a one-way call on the VN-Index.

Why the 161-162 zone matters

The easiest mistake is to assume that a high exchange-rate level automatically leads to intervention. In practice, Tokyo tends to care about more than one static number. Officials watch the speed of the move, the extent of speculative positioning, and whether markets appear to be testing the state’s tolerance.

That is why the 161-162 range in USD/JPY carries outsized psychological weight. CafeF’s report on international market moves noted that the yen is hovering near its weakest area in almost four decades; if the pair climbs further, traders are more likely to believe some form of stronger Japanese response is becoming more probable.CafeF Still, there is always distance between a warning and actual action, and that gap is what drives rotation across risky assets in the region.

Internal market data illustrate how quickly sentiment can shift once FX moves enter a sensitive zone. On May 1, 2026, USD/JPY fell from 160.24 to 157.15, a decline of 1.93%. On July 2, 2025, the pullback was even sharper, from 150.76 to 143.69, or 4.69%. In a market as deep as foreign exchange, swings of that size over a short span are meaningful.

Scenario one: Japan turns more forceful

Vietstock reported on June 23 that Japanese officials had signaled readiness to intervene in order to stabilize the foreign-exchange market if necessary.Vietstock If that message is upgraded in the next few sessions, the first response would likely be a sharp drop in USD/JPY. That would also pressure carry trades funded in yen, creating a broader regional de-risking move rather than a simple story of money “leaving one market for another.”

For Vietnam, the first screen should be USD/VND, not individual tickers. Over the last 90 sessions, USD/VND has traded in a relatively narrow band between VND 26,045 and VND 26,371 per dollar. If the yen rebounds hard while USD/VND stays stable, the impact on Vietnamese equities may remain mostly psychological. If USD/VND starts climbing with it, the conversation shifts toward broader FX pressure, and portfolio risk has to be read more carefully.

The VN-Index is now around 1,854.97 points. At that level, the key risk is not that the index “must fall” because of the yen. The bigger risk is that sectors with strong year-to-date gains get sold first.

Scenario two: Japan does not act yet

If Tokyo stops at signaling and does not move beyond that, the pressure comes through a different channel. A persistently weak yen can reinforce price advantages for Japanese exporters, while the rest of Asia has to reassess its own currency resilience and export competitiveness.

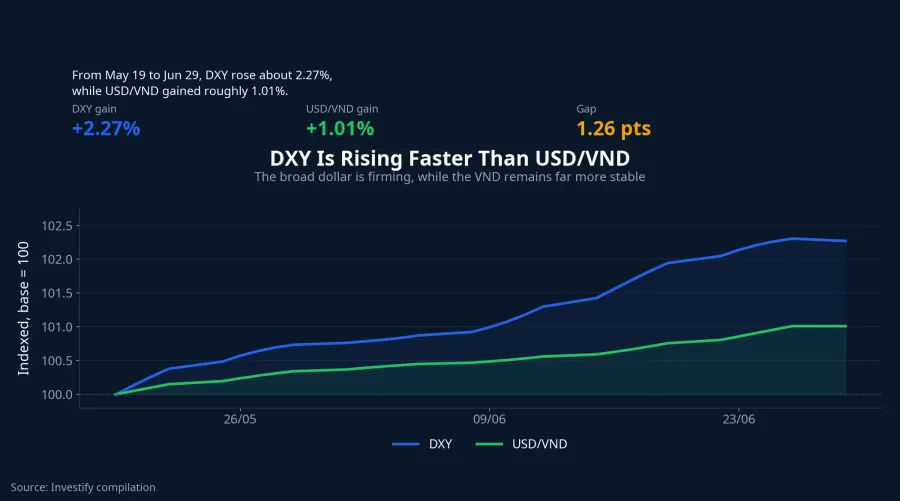

This is exactly where reasoning can become sloppy. A weaker yen does not automatically create direct pressure on the Vietnamese dong because Vietnam does not peg to the yen. The more important transmission channel runs through the broader dollar and through sentiment toward Asian risk assets. From May 19 to June 29, USD/JPY rose from 158.99 to 161.75, or about 1.74%. Over the same period, DXY climbed from 99.10 to 101.35, roughly 2.27%. When the dollar strengthens more broadly again, emerging markets usually face tighter scrutiny, especially after equities have already posted gains.

What stands out is that USD/VND has not reacted the way the yen has. That suggests the dong is not in the same stress regime as Japan’s currency. But that stability does not make FX irrelevant. It only means Vietnam is still in the second layer of reaction, so it is too early to jump straight to the idea that a weaker yen automatically helps Vietnamese exporters.

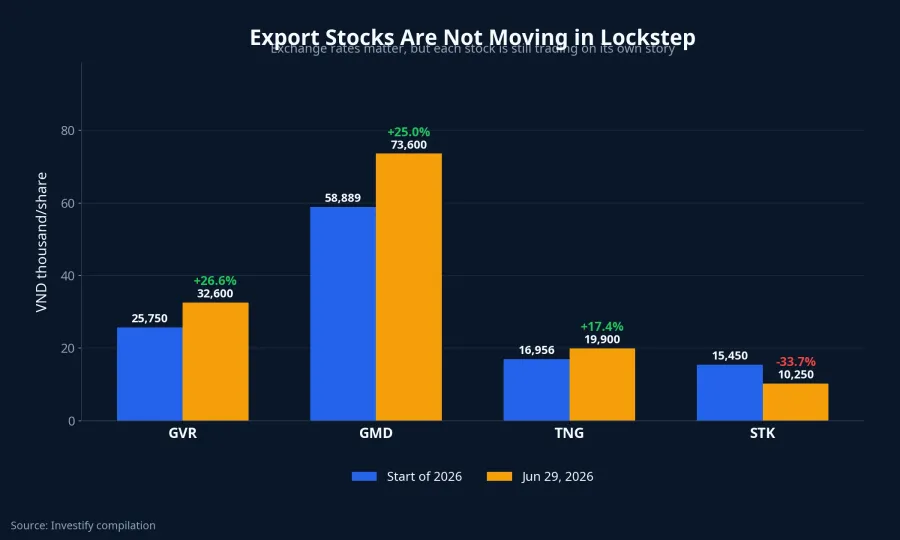

Export stocks need to be read one by one

The dispersion is already visible in the numbers. GVR closed on June 29 at VND 32,600 per share, above its start-of-year level of VND 25,750. GMD finished at VND 73,600, higher than VND 58,889 at the start of the year. TNG ended at VND 19,900, up from VND 16,956. STK, by contrast, closed at only VND 10,250, down from VND 15,450 at the start of 2026.

All four names can be grouped loosely under an “exports” label, but the market is paying for four different stories: rubber, ports, garments, and yarn. That is the key lesson for new investors. Markets do not price labels. They price how effectively each company can turn a macro backdrop into actual earnings. So if export names turn volatile in the next few sessions, that alone does not prove the core story has broken, and a stock that has already fallen is not automatically “cheap because of FX.”

What Vietnamese investors should monitor first

The cleanest order of signals, in my view, starts with FX and only then moves to equities. First comes USD/JPY around the 161-162 band and any new language from Japanese officials. If the messaging remains generic, markets may keep testing Tokyo’s tolerance. If officials shift toward tougher wording on speculative moves or possible action, the odds of a sharp reversal in the pair rise quickly.

Second comes USD/VND. The current level of VND 26,308 per dollar suggests the dong remains much steadier than several Asian peers. If that holds, Vietnamese equities are more likely to face sentiment pressure than a full-blown FX shock. If USD/VND breaks out of its narrow multiweek range, then the currency story becomes a genuine portfolio risk.

Third comes the reaction in stocks that have already rallied this year. GVR, GMD, and TNG all trade above their start-of-year levels, so if regional investors move into a more defensive stance, those are the kinds of names that can wobble first. For STK, a deep decline in the share price does not automatically make it safer.

The practical conclusion is straightforward: the yen nearing a 40-year low is not a one-way signal for the VN-Index. It is a signal to sort market reactions more carefully. The most defensible thesis right now is that the risk lies in short-term repricing and capital rotation, not in a certain call that Vietnam’s market is about to change trend. The key markers for the next few sessions remain USD/JPY, the tone of Japanese officials, and the stability of USD/VND. Unless those three pieces shift together, there is no reason to over-read the story.